Juewei Food’s 2025 financial report is being “rewritten by tax payments.”

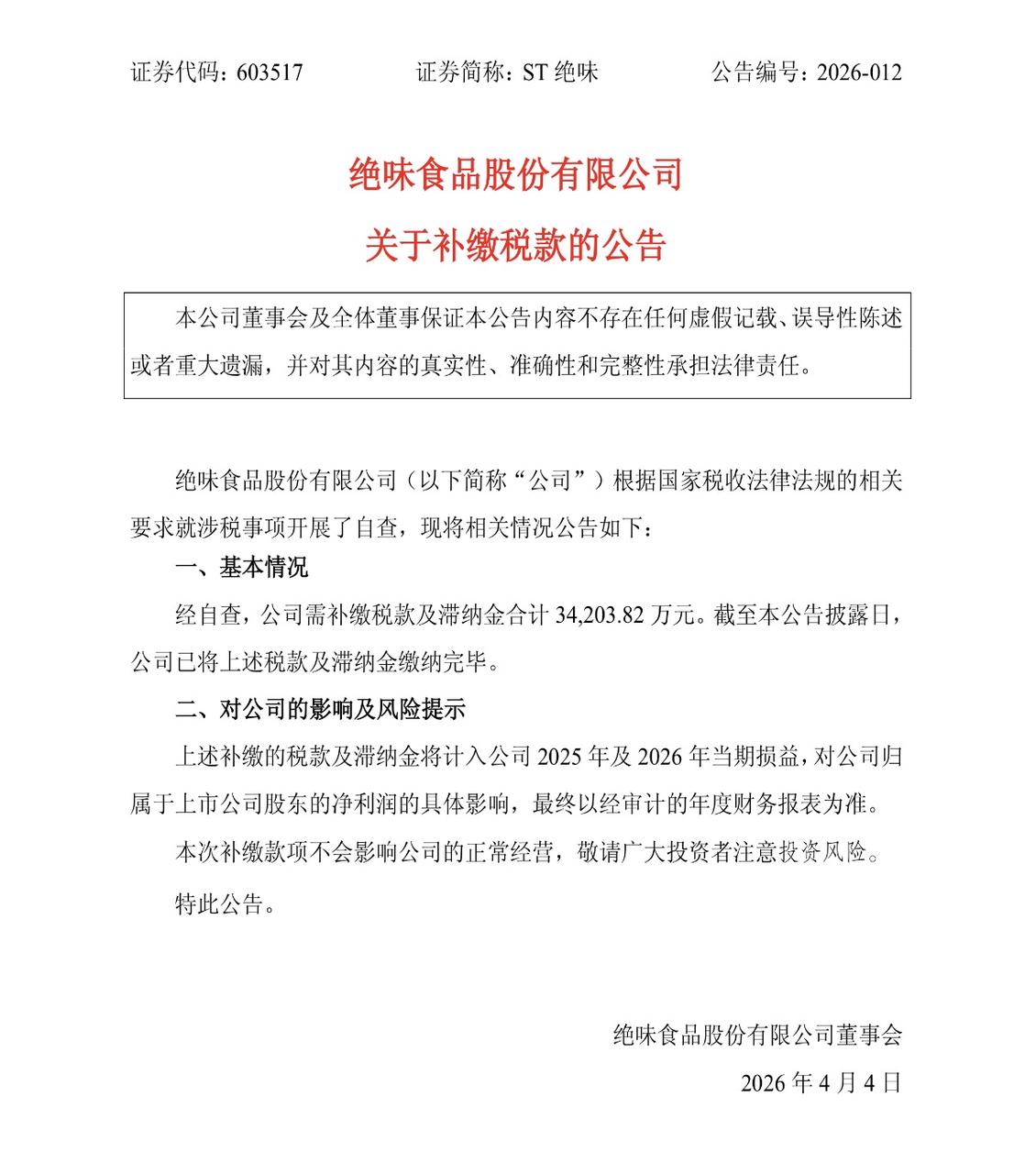

On the evening of April 3, 2026, ST Juewei disclosed that after self-examination, the company needed to pay back taxes and late fees totaling 342 million yuan. It has been paid in full. The back taxes and late fees will be included in the profits and losses in 2025 and 2026.

According to Juewei’s previous financial report, net profit in the first three quarters of 2025 will be approximately 270-280 million yuan. This means that a supplementary tax directly covers the entire year's profits or even losses.

Juewei Food expects full-year revenue in 2025 to be 5.3 billion to 5.5 billion yuan, a year-on-year decrease of 12% to 15%; net profit attributable to the parent company will be a loss of 160 million to 220 million yuan.

This is the company's first annual loss since it went public in 2017. Although the non-net profit is still positive, between 70 million and 100 million yuan, it is completely different from the net profit attributable to the parent company of nearly 1 billion at the peak of 2021.

This money seems to be a proactive "historical liquidation", but behind it is a complete chain of collapse from financial fraud to operational stalling and then to the first loss.

This 340 million is not an accident, but a "concentrated traceability" of a complete set of business operations in the past.

From 2017 to 2021, Juewei Food did not include the renovation costs of franchise stores into its revenue. The relevant funds were transferred through a joint account called the "Franchise Committee" and never entered the company's financial system. The accumulated hidden income in five years was approximately 723 million yuan.

According to the regulations of the Shanghai Stock Exchange, false records in financial indicators in the annual report will trigger the ST clause. Starting from September 23, 2025, the company's stock will be officially changed to "ST Juewei" and moved to the risk warning board, with the daily price limit narrowed from 10% to 5%.

This kind of operation is called "reverse counterfeiting" in the industry. It is not an inflated profit, but a concealment of income. The "extracorporeal circulation" of decoration expenses that should be included in the revenue point is collected through employee accounts to avoid financial confirmation.

By reducing the surface revenue scale, beautifying profit margins, and improving the attractiveness to franchisees.

In other words, Juewei's past expansion was not entirely based on real operating efficiency, but partly relied on "financial structure optimization."

The essence of tax repayment is that this growth logic is liquidated at once.

How did a chain with thousands of stores get to this point?

The decline in revenue didn't happen overnight.

In 2024, Juewei's annual revenue will be 6.257 billion yuan, a year-on-year decrease of 13.84%; the net profit attributable to the parent company will be 227 million yuan, a year-on-year decrease of 34%.

Entering 2025, revenue in the first half of the year was 2.82 billion yuan, a year-on-year decrease of 15.6%, and net profit attributable to the parent company was 175 million yuan, a year-on-year decrease of 40.7%. The second quarter was particularly brutal, with single-quarter revenue falling nearly 20% year-on-year, and net profit attributable to the parent company falling nearly 58% year-on-year.

In the first three quarters combined, revenue was 4.26 billion yuan and net profit was 267 million yuan. Although there were slight signs of narrowing in the third quarter, it was fully covered by the huge tax repayment.

The core variable dragging down performance is the accelerating shrinking of the store network.

Juewei Food has disclosed the number of stores in its annual reports for five consecutive years since 2019, expanding from 10,954 to 15,950 by the end of 2023; however, in the 2024 annual report, the company made no mention of the number of stores.

The silence itself said everything.

According to Zhaimen data, as of March 14, Juewei has approximately 10,476 stores across the country. Compared with the 14,969 stores disclosed in the 2024 interim report, there has been a net reduction of more than 4,000 stores in one and a half years.

The substantial shrinkage of stores has directly led to sluggish sales of fresh food products.

In the first half of 2025, fresh food revenue decreased by approximately 500 million yuan compared with the same period last year, a drop of more than 19%, and this category is precisely the company’s basic revenue base.

The rapid expansion logic of the franchise system is particularly fragile in an environment of declining consumption.

Juewei's business model is highly dependent on franchisees: the central factory is responsible for supply, franchisees bear terminal operating risks, and the company collects franchise management fees and ingredient price differences.

This model was extremely efficient in the era of horse racing, but once the profitability of a single store declines, the franchisee's urge to close the store is almost unstoppable.

In the first half of 2024, Juewei's average single store revenue was approximately 169,000 yuan, a year-on-year decrease of approximately 11%.

Franchisees cannot make money, and the chain reaction is to withdraw stores in batches. Juewei's sharp decline in the number of stores in the past two years is not so much a strategic contraction of "intensive cultivation" as it is the result of franchisees voting with their feet.

If the problem of Juewei in the past was "slowing growth", then after the tax payment, the problem has been completely magnified to "the failure of the profit model".

Faced with pressure on its main business, Juewei began to invest in catering as early as 2017, investing in more than ten brands such as Hefu Lo Noodles, Kuafu Fried Skewers, and Shuyishao Xiancao in the form of industrial funds, in an attempt to build a so-called "gourmet ecosystem."

As of the 2025 interim report, Juewei's long-term equity investment reached 2.38 billion yuan, which is the largest single asset on the balance sheet, accounting for nearly 30% of total assets.

However, this road failed.

Invested brands are generally experiencing a consumption winter, and investment losses under equity method accounting have also become one of the important weights that crush the income statement.

The company clearly mentioned in its performance forecast that an increase in non-operating expenses and investment losses under equity method accounting were important reasons for the substantial change in profits.

The main business is declining, the investment sector is losing money, and both legs are lame at the same time. It is almost inevitable that Juewei will fall into its first loss in 2025.

It is worth noting that among the three giants of braised food, Juewei is the only company to have a net loss in 2025.

Zhou Hei Ya's revenue in 2025 will be 2.536 billion yuan, a year-on-year increase of 3.47%, and the net profit attributable to the parent company will be 157 million yuan, a year-on-year increase of more than 60%; Huang Shanghuang's profits in the same period have also rebounded significantly.

Zhou Hei Ya's rebound path is relatively clear: focus on optimizing store structure, vigorously develop instant retail channels, and reduce expense ratios.

But Juewei’s franchise model naturally limits this path. If the headquarters vigorously develops real-time retail, it will directly erode the terminal sales of franchisees and shake the basis of interest distribution of the entire system.

The dilemma faced by Juewei is not just "the need for a better strategy", but that its core business model has encountered structural failure in the current consumption environment.

The back payment of 342 million in taxes is a general settlement of the financial loopholes in the past five years; the implementation of ST risk warning, stock trading on the risk warning board, and the narrowing of the daily price limit to 5% are real-time rulings given by the capital market.

In the past, the market value of the "Duck Neck King" once exceeded 60 billion, but now it is slowly digesting historical bills within the daily increase and decrease limit of 5%.

This is not only the plight of a company, but also a microcosm of the official end of the old braised food era of "opening a business to make a profit, and franchisees flocking in".