Let’s start with a collective turn on Wall Street

In the fall of 2024, Citrini Research released a report that was later widely cited. Its core argument pointed to a fact that made technology stock bulls uneasy: the crowding degree of AI concept stocks has reached its peak.

The chain reaction triggered by this report was dramatic. The technology sector has lost approximately US$300 billion in market value in just a few weeks, but funds have not left the market, but have begun a structural migration: from "light assets" such as software, algorithms, and models to the physical infrastructure that truly supports the operation of AI.

Morgan Stanley first extracted the essence of this trend and compiled an index called HALO – Heavy Assets, Low Obsolescence, which means "heavy assets, low obsolescence."

Goldman Sachs followed suit, and institutional consensus quickly formed. The core logic of HALO is not complicated: in a world where AI technology is iterating extremely fast and geopolitics is becoming increasingly turbulent, those hard assets with long construction cycles, high replication thresholds, and that will not be easily replaced by AI are the core assets that are truly worthy of long-term holding. Data centers, power grid infrastructure, nuclear power, mining, energy transportation networks – these tracks were quickly labeled as HALO assets.

The escalation of conflicts in the Middle East has added another layer of variables to this logic: when energy security upgrades from an "economic issue" to a "survival issue," the strategic value of hard assets is further amplified.

But amid this wave of repricing, one asset class has been severely undervalued: energy storage.

Counter-intuitive investment logic: The more powerful the AI, the more valuable energy storage is

In HALO's original framework, data centers and computing power networks were regarded as the "physical base" of the AI era. This judgment is not wrong, but it misses a key link: electricity is not only a matter of "sending out", but also a matter of "stability, storage and mobilization".

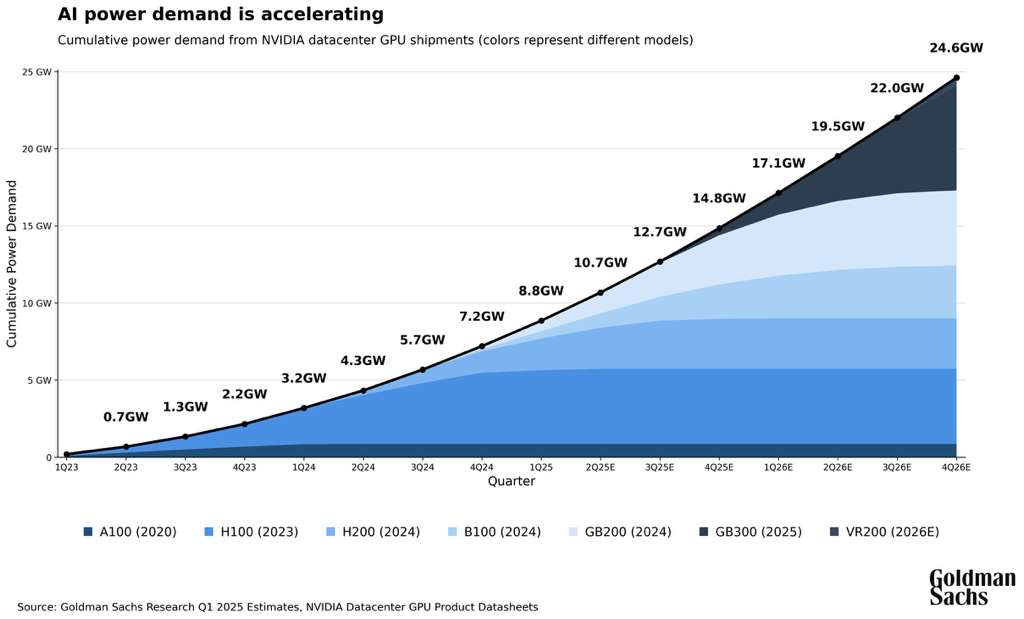

Data can help understand this judgment. Goldman Sachs predicts that global data center power demand will increase by 165% by 2030. The explosion of computing power means a sharp increase in the load of the power grid, and wind and solar power generation are naturally intermittent – photovoltaics stop outputting after the sun sets, and the wind turbines rotate stationary when there is no wind. There is a huge gap between the intermittency on the power generation side and the 24-hour random fluctuations on the power consumption side. The only thing that can fill this gap is energy storage.

This forms a counter-intuitive but highly deterministic investment logic: the more powerful the AI, the greater the demand for computing power, the greater the power gap, and the more valuable energy storage is. Energy storage has surpassed its traditional supporting role and become an indispensable core in the AI-computing power-power chain. Without energy storage, the power supply of the data center cannot be stable, and the explosion of computing power is a rootless tree.

Using the original definition of HALO on an item-by-item basis, the compliance of energy storage is more significant than that of many assets that have been included in the HALO framework.

Let’s look at the “asset-heavy” dimension first.

The investment in a 100-megawatt-hour energy storage power station often costs hundreds of millions of yuan, and the approval process involves multiple links such as grid connection permission, environmental impact assessment, and land approval. This means that the replication threshold for energy storage power plants is no lower than that of an oil pipeline or a nuclear power plant – they are both assets that are "too heavy to move".

Let’s look at the dimension of “low elimination rate”.

AI can optimize the dispatching strategy of energy storage power stations and improve charging and discharging efficiency, but it cannot replace a physical energy storage power station to provide inertial support and frequency regulation for the power grid. This is the real "AI optimized but irreplaceable". An analogy may be more intuitive: AI can optimize flight scheduling, but it cannot replace an airport. Energy storage power stations are to the power system what airports are to the aviation system – they are indispensable physical nodes.

The real threshold for energy storage assets: not to create it, but to “survive it”

"Making batteries" and "operating energy storage power stations" are two completely different businesses.

The outside world's understanding of the energy storage industry often remains on the simplified model of "batteries put into containers." But for professional investors, the first step in understanding energy storage assets is to distinguish between the two distinct value segments of "manufacturing" and "operation."

Failure analysis data from the Electric Power Research Institute (EPRI) shows that energy storage system failures occur more in system integration and operation than in battery manufacturing itself. This discovery subverts many people’s intuition: the moat of energy storage assets is not only the upstream cells, but also includes the “integration + operation” of the midstream and downstream.

Whoever can turn a pile of hardware into an asset that can run safely for 25 years and continue to generate income is the real winner. This is similar to the logic of the real estate industry: it is not difficult to build a building, but what is difficult is to make it continue to generate stable cash flow for 25 years.

Energy storage is entering the "trading era": a power station is a trading desk.

As the power spot market accelerates globally, the profit model of energy storage is undergoing a fundamental change. The operation of early energy storage power stations was relatively simple – charging during valley hours, discharging during peak hours, and earning the peak-valley price difference. But now, the rate of return of energy storage power stations increasingly depends on the operator's ability to accurately capture arbitrage opportunities amid power price fluctuations, participate in frequency regulation services, and respond to grid dispatch. This is no longer a pure hardware business, but a comprehensive ability competition of "hardware + algorithm + market understanding".

Industry data shows that excellent trading strategies can significantly increase the internal rate of return (IRR) of energy storage projects.

Just last April 1, green technology company Envision Technology Group released the world’s first 12.5MWh AI energy storage system. Through the deep integration of large models and physical AI, energy storage power stations can evolve into intelligent entities that can actively trade.

By accurately capturing power market signals, the system can further increase IRR by 4-8% during the entire life cycle. This operational generation gap from passive response to active gain is redefining the value boundary of energy storage assets.

Reliability in extreme scenarios: a key variable in asset pricing

The deployment of energy storage power stations is moving from greenhouse conditions to the harshest environments in the world. The summer surface temperature in the deserts of the Middle East can reach 50°C, the winter temperature in the Arctic Circle can be as low as -60°C, and the high-humidity and high-salt environment in Southeast Asia are extremely corrosive to electronic components. To allow an energy storage power station to operate safely for 25 years in these environments will not test a single technology, but a whole set of system capabilities from design, manufacturing to operation and maintenance.

The picture shows the distant view of Yicha Ganhada energy storage power station

Envision Energy Storage's delivery and operation record in extreme and complex scenes such as extreme cold and deserts – so far no major safety incidents – is essentially accumulating an "operational credit" that is difficult to be quickly copied by latecomers. To investors, this "operating credit" is similar to the underwriting record in the insurance industry. It cannot be obtained quickly through capital expenditures, but can only be accumulated slowly through time and performance.

This is precisely the most typical characteristic of HALO assets: moat is a function of time, not capital.

If the physical robustness in extreme environments guarantees the "bottom line of survival" of assets, then playing a proactive role at the power grid system level determines the "upper limit of value" of assets.

One cutting-edge trend that deserves investors' attention is "network-based energy storage." Traditional energy storage power stations are "grid-following", that is, they passively respond to the dispatching instructions of the power grid. Network-based energy storage goes a step further. It can actively maintain the voltage and frequency stability of the power grid. To put it simply, it not only "uses the network", but can "build the network".

This capability is possessed by only a handful of companies worldwide, and the unit price is more than 15% higher than conventional energy storage. Envision is the first company in the world to pass the China Electric Power Research Institute's full-scenario network construction test, which means that it has obtained a ticket that only a very few players can get.

From an investment perspective, network-building capabilities are similar to the “franchise” of the energy storage industry—the technical threshold itself constitutes a scarcity premium, and in the foreseeable future, the demand for network-based energy storage will accelerate as the penetration rate of new energy increases.

China, the most irreplaceable pole in the global energy storage landscape

When discussing HALO assets, an often mentioned point is that real hard assets must not only be heavy, but also "scarce". In the global energy storage landscape, China's scarcity is structural.

At present, China's new energy storage installed capacity accounts for more than 40% of the world's total, but more importantly, China is the only country in the world that has full-chain closed-loop capabilities from upstream mineral resources, midstream battery manufacturing, downstream system integration to terminal operation and maintenance services.

What does this industry depth mean? It means that Chinese energy storage companies have far greater control over the entire value chain than their competitors in other countries. As stated in the HALO document – "China's production capacity that can provide a complete set of power grid equipment is extremely scarce" – replace "power grid equipment" with "energy storage system", and the logic is completely established.

Another implication of this industry-wide chain capability lies in the resilience of the supply chain. When there is a supply shock in a certain link – whether it is upstream lithium ore price fluctuations or midstream chip shortages – Chinese companies can digest and adjust within the internal chain. For those competitors that rely on external procurement, every link may become a weak point.

In 2025, China's investment in energy storage capacity expansion will exceed 800 billion yuan, and the iteration speed of large-capacity battery cells will be half a year. This speed is not accidental. It is the natural result of the scale effect and manufacturing efficiency that China has accumulated over the years in the field of new energy.

It should be emphasized that this is not a low-price competition. Low-price competition involves sacrificing quality for price, while the cost advantage of China's energy storage comes from the downward shift of the cost curve driven by scale effects and manufacturing efficiency. For global buyers, the price-performance ratio of Chinese energy storage systems leaves no alternative in the short to medium term. This is not an opinion, but an economic fact – any attempt to replicate energy storage capacity of the same scale and efficiency outside of China would require at least 10 years and hundreds of billions of dollars of investment.

In the context of geographical fragmentation and supply chain restructuring, China's manufacturing capabilities alone are not enough. The localization of supply chains is accelerating around the world, and the European Union, the United States, and the Middle East are all formulating local manufacturing requirements. This means that the competition in the future energy storage industry will not only be “who can build it well”, but also “who can build it well in multiple locations around the world at the same time.”

As the earliest representative of energy storage companies to implement international layout, Envision has 14 manufacturing bases around the world, covering core markets such as China, Japan, the United States, and Europe, and has a leading market share in markets such as the United Kingdom. This capability combination of "localized manufacturing + global operations" exactly responds to the core of HALO's logic – in geopolitical turmoil, whoever can occupy an irreplaceable position in supply chain reconstruction is the real hard asset. In contrast, energy storage companies that only operate in a single market will face the risk of being marginalized in the wave of supply chain restructuring.

From “selling equipment” to “selling system solutions”: The value transition of Chinese energy storage companies

In the early days, China's energy storage market mainly sold batteries and hardware overseas, which placed it at a lower position in the value chain. With the tightening of the export tax rebate policy that began on April 1 this year, the focus of industry competition is shifting from "price game" to "technology-driven and service value-added" – leading companies are completing a key value transition, from exporting a single hardware product to exporting a complete set of "hardware + software + operations" solutions.

In this context, it is no longer an option for Chinese new energy companies to accelerate their global localization layout, but a necessity. Only by completing the deep integration of the supply chain as soon as possible can we seize future opportunities.

Envision's 680MW/1360MWh energy storage project in Carrington, UK, is such a typical case. In this project, Envision not only sells equipment, but also provides a complete system including AI dispatch and power transaction optimization.

Upon completion, the project will provide two hours of electricity supply to 2.2 million households. This figure alone illustrates the scale and impact of energy storage assets – it is no longer a "supporting equipment", but an infrastructure that can affect the lives of millions of people.

Not only that, going back to the AIDC mentioned at the beginning, Envision and Tencent have launched the world's first 100% green electricity direct supply data center in Chifeng, Inner Mongolia. The comprehensive energy cost has been reduced by more than 40%, and the annual carbon emissions can be reduced by up to 180,000 tons. Behind this is Envision's multi-scenario energy solution from "core" to "network", which can effectively solve the power bottleneck of data centers in the era of AI computing power.

In the AI era, whoever controls stable, green and affordable energy will control core productivity.

Envision joins hands with Tencent to launch the world's first 100% green electricity direct supply data center in Chifeng, Inner Mongolia

From an investment perspective, this transition from “selling products” to “selling solutions” means three changes:

Higher customer stickiness. When your solution is deeply embedded in the customer's asset operations, switching costs become extremely high; stronger pricing power. What you are selling is no longer standardized hardware, but system capabilities that are difficult to replicate, economical and sustainable power, and thicker profit margins.

There is another often-overlooked dimension to the irreplaceability of energy storage in China: the policy environment. From national-level energy storage development planning to local-level distribution and storage requirements, from power market reform to the mechanism design of energy storage capacity electricity prices, China has a systematic institutional framework for the development of the entire energy storage industry chain, and it is constantly improving. This institutional advantage provides stable expectations and market space for energy storage companies.

At the same time, the deepening of China’s electricity market reform is creating more profitable scenarios for energy storage assets. With the full spread of the spot market and the improvement of the ancillary service market, the income sources of energy storage assets are moving from a single peak and valley arbitrage to diversification. This means that the return certainty of energy storage assets in the Chinese market is increasing, and return certainty is precisely the most important indicator for long-term capital.

Conclusion: Deterministic Anchors

Let us return to the core proposition of HALO. In an era of accelerating technological iterations and restructuring of the geopolitical landscape, investors need to find deterministic anchor points that will not be blown away by the next wave of technology or washed away by geopolitical turmoil. Energy storage assets are just such an anchor.