On March 30, Allbirds announced that it would sell all of its intellectual property and core assets to brand management company American Exchange Group (AXNY) for a consideration of approximately US$39 million, and the listed company immediately initiated liquidation procedures.

Five years ago, this company that emerged as a "wool shoe" stood on Nasdaq, with a valuation of nearly US$4 billion, and was regarded as a model for DTC brands; five years later, its price is only a little over one-tenth of its 2021 IPO fundraising amount, which is only equivalent to about 1% of its peak market value.

Also in 2021, another company whose main business is sports shoes also rang the Nasdaq bell-Angpa.

The two companies almost completed their listings on the same beat: they are both representatives of "new consumer brands" and they both tell clear and moving growth narratives.

However, as time moves forward, they lead to completely different endings. One is still being considered as a candidate for the "next generation global sports brand", while the other has exited the stage in a near-liquidation manner.

If you stack these two trajectories together, you will find that their differentiation does not occur at the starting point, but exactly after the most similar place.

The same paradigm created two stars

For the first few years, Allbirds and On Running pretty much followed the same playbook.

They all start not with a "brand" but with an extremely clear product.

Allbirds was co-founded by former New Zealand professional players Tim Brown and Joey Zwillinger. It was launched in 2016 with a single product, Wool Runner. The brand uses merino wool, eucalyptus fiber and sugar cane-based SweetFoam soles as the pillars of its material narrative, advocating that people do not need to choose between high-quality products and environmental costs.

Angpa uses the Cloud series to transform the hollow cushioning structure into a technical experience that can be intuitively perceived.

What the two have in common is not material or structure, but that they have found a difference that can be repeated over and over again – a "language unit" that is enough to complete a cold start in a crowded market.

This kind of product quickly transcended the function itself and became a kind of identity label.

Allbirds quickly became popular in Silicon Valley. It has almost become the "default shoe" for practitioners in technology companies and the "work uniform" in the venture capital circle. Obama has worn it in public events, and DiCaprio has directly become a shareholder. Jack Ma has also appeared wearing Allbirds shoes.

Angpa starts from the runner group. The patented CloudTec cushioning technology and the quality sense of Swiss engineers allow it to quickly establish barriers between the running community and affordable luxury consumers, and gradually penetrate into the daily wear of the urban middle class.

They respectively carry two typical self-narratives: one is "rationality, environmental protection, restraint" and the other is "self-discipline, movement, efficiency".

In this sense, what they sell is never just shoes, but the path to "becoming a certain kind of person".

In order to ensure that this narrative is not diluted, both companies chose a highly consistent channel strategy in the early days: focusing on DTC, controlling the rhythm of stores, and treating distribution with caution.

Channels are no longer just sales tools, but part of brand expression, an interface that can continuously output values and aesthetics.

As these elements gradually take shape, the capital market will become the next stop. In 2021, they will be launched on the market at the most complete and conclusive stage of their respective narratives. The interval between their launches is only 47 days.

Landing in the capital market opened up the imagination of the two brands about the future. Immediately afterwards, the two companies unanimously moved towards the same goal: from a pair of shoes to a lifestyle brand, trying to cover a wider range of wearing scenarios and consumer needs.

If you only see this, it's hard to imagine that they will eventually lead to completely different endings.

The real fork occurs after the listing.

After the listing, the flexibility of the narrative began to diverge.

If the IPO is the starting point where the fortunes of the two companies begin to diverge, then the root cause of the bifurcation is not luck, but the actual depth of the brand moat.

The differentiation first appears in the underlying logic of the product.

What Angpai has built is a system that revolves around performance. Its core is always to "run better", to be lighter, more stable and more resilient. Technology here is not a decorative language, but the ability to continuously iterate. Each generation of product updates strengthens this center.

The starting point of Allbirds is materials. Wool, eucalyptus fiber, and sugar cane midsole, these elements form a complete and moving "sustainable narrative."

However, the material itself is difficult to form a long-term barrier. It can be imitated and replaced, and it is difficult to bring significant performance leaps in each generation of products. Therefore, environmental protection has become more of an attitude expression rather than a rigid demand.

This difference is further amplified in usage scenarios.

Running is a high-frequency, quantifiable behavior, which naturally requires continuous optimization of equipment and naturally leads to repurchase; while commuting shoes are closer to "durable goods". A pair of shoes can be worn for a long time, and the reasons for updating are often insufficient.

As a result, one brand can continuously strengthen its own value through continued use, while the other can more easily stay in the freshness of the “first purchase”.

The sustainability of the brand narrative was also tested at this stage.

The sustainable development that Allbirds has always adhered to is undoubtedly a correct proposition, but it does not automatically constitute a reason to buy. As more and more brands begin to talk about environmental protection, and as regulation and public opinion continue to increase their demands for "green narratives," this advantage is quickly diluted.

After the IPO, Allbirds faced continuous questions about growth from public companies. Management chose the mistake that almost all consumer brands under the same pressure would make: replacing deepening with expansion.

In 2022, the company will open a large number of stores, with a peak of more than 50 stores worldwide. At the same time, the product line began to accelerate its expansion into the fields of sports performance and clothing, from the launch of Tree Flyer, which focuses on running scenes, to the layout of categories such as wool leggings and jackets, and the introduction of product talents with Nike and Adidas backgrounds in an attempt to complement professional sports capabilities.

But this path did not work as expected.

Its performance running shoes have limited recognition among professional runners, and some products have been questioned in terms of durability and functionality. The clothing line has also failed to establish a stable repurchase logic, which has brought inventory pressure to a certain extent. At the same time, new series such as Pacer and Riser lack clear product memory points and fail to continue the explosive effect of the early Wool Runner.

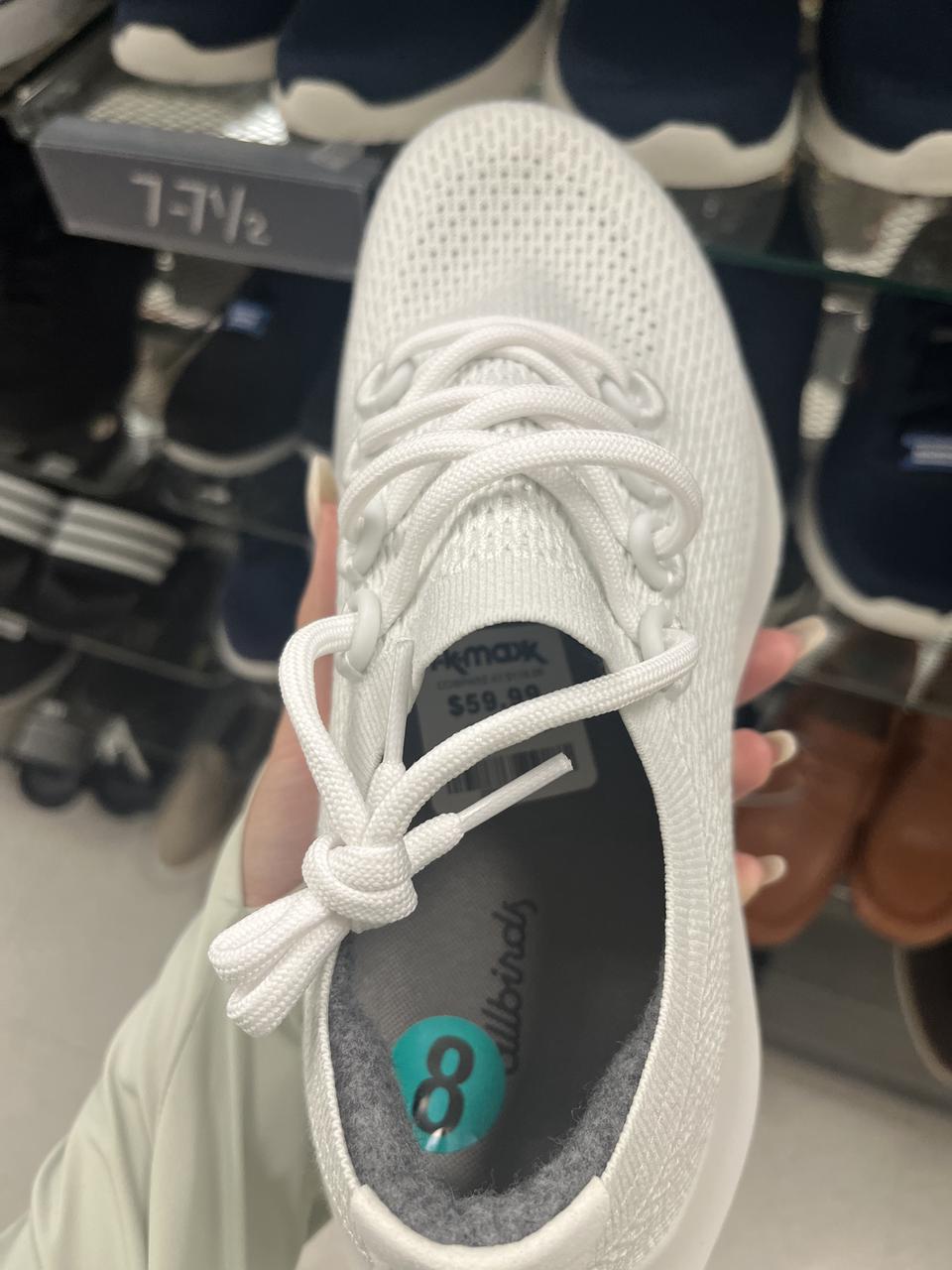

In 2023, Allbirds has entered TK Maxx (special sale mall), with a price tag of 59.99 Australian dollars, which is almost half the price. It’s only been two years since it landed on Nasdaq.

Allbirds' cumulative net losses in the five fiscal years have reached US$419 million, and revenue has continued to shrink from a peak of US$298 million in 2022. What's even more cruel is that every year that losses narrowed was accompanied by a further decline in revenue.

This is a typical sign of a company seeking to survive through contraction rather than growing toward profitability.

The Chinese market: a misjudged field

Allbirds officially entered the Chinese market in 2019, which is not too late in itself.

At that time, it was the most active stage of the new consumer brand narrative. The DTC model was repeatedly verified. Capital and public opinion were looking for the next "China's Allbirds".

The problem is not that it comes too late, but that it brings a set of paths that have been established in the West but may not be applicable to China.

In the first few years, Allbirds in China almost completely continued its approach to the US market: emphasizing brand tone, controlling channel rhythm, focusing on direct-operated stores and online channels, and trying to copy the diffusion path of "Silicon Valley to the world".

But this path quickly encountered structural resistance in China.

In a consumer market driven by efficiency, channels are first and foremost "scale machines" rather than "narrative media."

When Nike, Adidas and even local brands have completed their penetration through mature distribution systems, it will be difficult for a brand that emphasizes restrained expansion to establish a sufficient market presence in a short period of time. The "slow" that Allbirds insists on is more easily understood as "weak" in the Chinese context.

The real turning point will occur in 2024. Allbirds handed over the exclusive distribution and operation rights to Belle Fashion Group in mainland China, Macau and Taiwan markets, closed some directly operated stores, and shifted its channels to a full distribution system.

From a capability structure perspective, Belle is almost the “opposite” of Allbirds.

It has a dense offline network, mature local operating capabilities and a highly industrialized supply chain system. It has helped Champion achieve annual revenue of over 1 billion yuan and thousands of stores in China. In a market that emphasizes scale and efficiency, this is exactly what Allbirds is missing.

But the problem is that this "complementarity" comes too late.

He entered China in 2019 and completed the path switch from DTC to distribution in 2024. The five years in between were not only time costs, but also a missed window period.

Especially in the Chinese market, "environmental protection" has always remained at the cognitive level and is difficult to transform into a stable purchasing motivation. When the product itself cannot form a clear advantage in performance or design, no matter how strong the channel is, it can only amplify mediocrity.

As a result, this cooperation is more like a "structural remedy" than a true growth engine. The entry of Belle did not change the fundamentals of the brand. Instead, it marked to some extent that Allbirds gave up its active control over the Chinese market.

Compared with Angpa's unconcealed ambitions for the Chinese market, Allbirds regards the Chinese market as an "important growth engine" in theory, but is always on the margins in actual operations. It's mentioned over and over again, but never actually implemented.

When the brand finally tried to enter in a more localized way, the time and resources it had were no longer enough to support a real reconstruction.

The ending of Allbirds can easily be simplified as a story about failure, but if you put it back on a longer timeline, it is actually more like a manifestation of the boundaries of methodology.

In the past ten years, a new consumption path centered on "hot products + narrative + DTC" has been repeatedly verified and quickly copied. Allbirds is one of the most typical and complete cases in this set of paths.

Its problem is not that it took the wrong steps, but that when this path reaches its extreme, a lower-level question must be answered: what is left after the story is told.

Wu Xiaobo steps on Wool Runner at the 2025 Thoughts Site

The answer given by Allbirds is the product itself, which is a performance that can continue to evolve, and a user experience that can be repeatedly verified; while Allbirds relies on a value proposition that needs to be constantly emphasized, but is difficult to support purchase independently.

In the Chinese market, Angpai is still insisting on DTC, and Allbirds' dilemma is that it has not had time to establish a strong enough "reason for trading."

When the market returns to simpler judgment standards, the difference becomes irreversible.

$39 million is not a simple price, it is more like a full stop. It marks not only the end of a brand, but also the final manifestation of a set of "narrative-first" consumption logic in the real world.