Domestic substitution is unstoppable!

With the improvement of technological level, my country's high-end technology manufacturing industry has ushered in the time of domestic substitution.

The most typical ones are the semiconductor equipment and chip industries. According to relevant data, the localization rates of the two will be approximately 20% and 12% respectively in 2023. There is still a lot of room for improvement before complete localization.

Medical devices are also a very important domestic alternative.

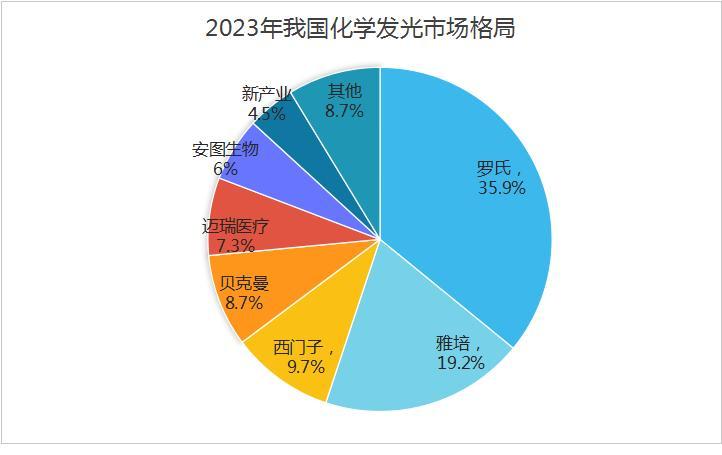

In 2023, in the field of "chemiluminescence" medical diagnosis in my country, foreign manufacturers such as Roche, Abbott, and Siemens still occupy more than 70% of the market share, while domestic medical device companies such as Mindray Medical, Antu Biotech, and New Industries account for less than 30% of the market.

Among them, New Industries is the leader that focuses most on chemiluminescence diagnosis.

As early as 2008, New Industries successfully developed the first fully automatic chemiluminescence analyzer in China, breaking the monopoly of imports. Later, in 2018, it launched the world's first luminometer with a detection speed of 600T/H, becoming one of the rare chemiluminescence diagnostic companies in my country that has successfully gone overseas.

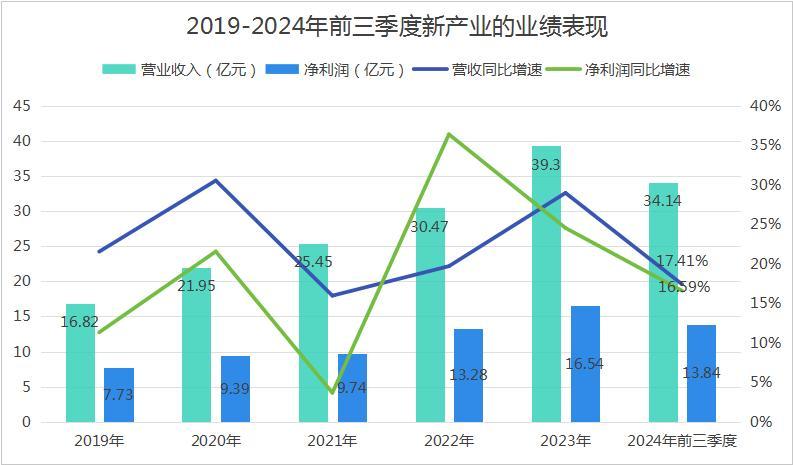

Against the background of domestic substitution, the performance of new industries has maintained rapid growth.

From 2019 to 2023, the company's revenue and net profit compound annual growth rates reached 23.21% and 18.97% respectively.

Until the first three quarters of 2024, the company's revenue and net profit were 3.414 billion yuan and 1.384 billion yuan respectively, still maintaining a rapid growth trend year-on-year.

Not only that, compared with companies in the same industry, the new industry also presents two outstanding advantages:

First, it has stronger resistance to centralized purchasing.

In recent years, with the normalization of centralized purchasing in the pharmaceutical industry, the biggest feature displayed by the new industry is its strong ability to resist centralized purchasing.

Especially compared with other in vitro diagnostic manufacturers, the new industry has shown a certain stability in performance.

In the first three quarters of 2024, among the top 10 companies in the in vitro diagnostic industry by revenue scale, New Industries is the only company to achieve a year-on-year growth rate of more than 15% in revenue and net profit, and its performance is significantly better than Antu Biotech, Wondfo Biotech, etc.

This is because among the in vitro diagnostic products that have been collected in recent years, chemiluminescence products have maintained a relatively mild price drop due to their high technical content and good market competition.

As we mentioned earlier, the new industry is the company that focuses most on chemiluminescent diagnosis. For example, Antu Biotech has a relatively broad layout of in vitro diagnostic products, Wondfo Biotech has a high market share in the field of POCT rapid detection, and Mindray Medical is a leader in comprehensive medical devices.

Second, profitability is stronger.

Compared with other in vitro diagnostic manufacturers, the new industry also presents an advantage in that it has stronger profitability.

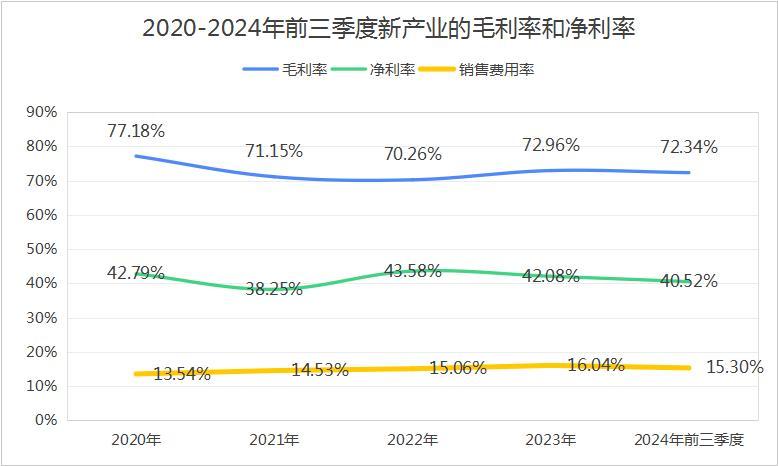

On the one hand, as a medical diagnosis manufacturer, the company's gross profit margin and net profit margin are already very high.

In the first three quarters of 2024, the gross profit margin and net profit margin of the new industry reached 72.34% and 40.52% respectively. Although a gross profit margin of 70% is common in the industry due to high technical barriers, a net profit margin of 40% is difficult. Even Mindray Medical, the leading medical device company, cannot reach it, only 36.3%.

While maintaining high gross profit margins, low sales expense ratios have become the key reason for the company to maintain high net profit margins. Since 2020, the sales expense ratios of new industries have basically remained below 16%.

This not only corresponds to the company's good market competition, but also reflects that it maintains high channel barriers for hospital sales.

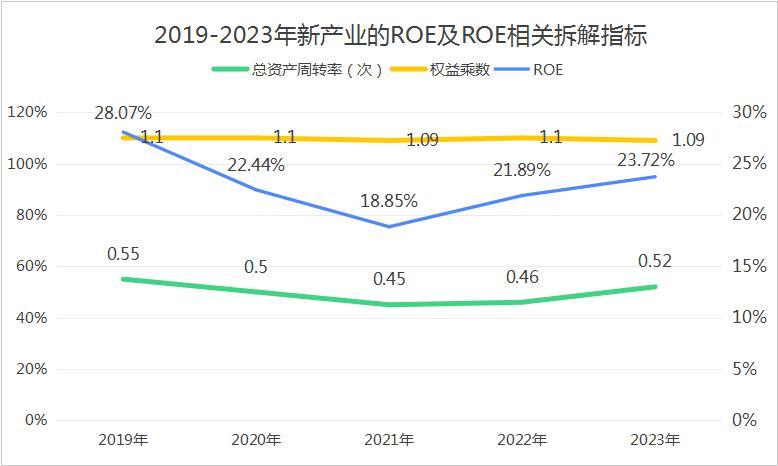

On the other hand, with the support of net interest rate, the new industry has also maintained a high ROE.

The company's average ROE from 2019 to 2023 is 22.99%, fully meeting the standards of an excellent company considered by Buffett (ROE>20%).

In recent years, despite the ups and downs in ROE, the company has not only overcome the impact of centralized procurement on the net profit margin, but also maintained the stability of the total asset turnover rate and equity multiplier. In particular, the fluctuation of the equity multiplier does not exceed 0.1, and the asset-liability ratio has always been controlled at around 8%-9%.

So, with the support of many advantages, is the new industry expected to continue to maintain good growth?

1. The domestic industry market maintains high prosperity, and it is time for domestic substitution

As we all know, chemiluminescent diagnosis is the largest in vitro diagnostic market segment in my country. Its demand comes from clinical diagnosis of patients. It has a wide range of applications, covering the examination of tumor markers, thyroid function, infectious diseases and many other diseases.

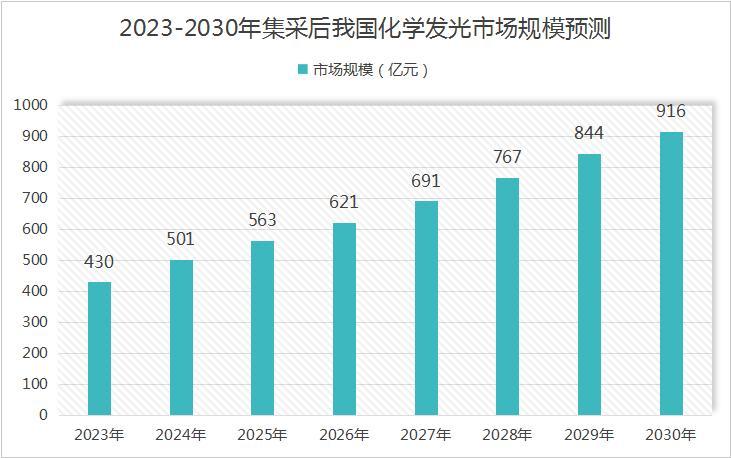

In 2023, my country's chemiluminescence market size will reach approximately 43 billion yuan. In the future, as my country's population ages and medical standards improve, the industry market size is still expected to maintain a rapid growth trend.

Some institutions predict that my country's chemiluminescence market size will grow to 91.6 billion yuan in 2030, with a compound annual growth rate of 10.88% from 2023 to 2030.

On this basis, domestic manufacturers such as New Industries still have a large space for domestic substitution, and are expected to achieve a scale growth rate that exceeds that of the industry.

2. The company continues to expand overseas and other in vitro diagnostic markets

Nowadays, the new industry is no longer satisfied with the domestic chemiluminescence market and is gradually expanding to overseas and other in vitro diagnostic markets.

One is the overseas market. In recent years, driven by global public health events, the company has successfully expanded its market overseas by virtue of its product advantages. In 2023, the proportion of overseas revenue has reached 33.63%.

At the same time, the company's installed capacity of medium and large instruments in overseas markets is still increasing, reaching 64.8% in the first half of 2024. In the future, driven by in vitro diagnostic instruments, the company's reagent products are expected to continue to increase in volume.

One is the other in vitro diagnostic market, including biochemical diagnosis, molecular diagnosis, coagulation diagnostic products, etc.

To this end, new industries continue to increase investment in research and development. From 2020 to 2023, the company's research and development expense rate increased from less than 7% to 9.32%. In the first three quarters of 2024, research and development expenses increased by 20.66% year-on-year to 327 million yuan.

However, some people may worry whether the deployment of other in vitro diagnostic products in the new industry will bring greater risks of centralized procurement.

In fact, there is no need to worry about this, because although centralized purchasing will reduce product prices, it will increase sales. For new industries, other in vitro diagnostic markets are equivalent to a large blank market cake, and companies will generate increments as long as they deploy.

Moreover, in the provincial alliance centralized procurement that was just launched in January 2025, the average price of the two major categories of chemiluminescent swollen labels and thyroid gland products fell by 53.9%. The decrease was still moderate, and at the same time, the proportion of products reported in the new industry reached more than 10%.

Therefore, in the future, on the basis of domestic substitution and the company's own development, new industries are still expected to maintain performance growth.