If we look at the expectation of interest rate cuts + the halving of Bitcoin's cyclical supply + the damage to the US dollar's credit + the regulatory friendliness of the Trump administration, it has supported the rise of cryptocurrencies from 2022 to the present.

As of June 23, the cryptocurrency market reached $3.3 trillion, an increase of nearly three times since 2023. Among them, the most well-known one, Bitcoin, which is the largest and contributes more than 60% of the market value, has also risen from less than 30,000 US dollars in mid-2023 to more than 100,000 US dollars today.

What does $3.3 trillion mean? It is equivalent to 3% of global GDP. If the overall crypto-assets are regarded as a national economy or a company called Crypto, then:

The current crypto-assets are equivalent to the economic level of an upper-middle-class developed country, beating France to rank 7th in the world;

It is also a company that has surpassed Apple (3 trillion) and become the third largest company in the world by market capitalization. Microsoft and Nvidia, which are at the top, have about 3.6 trillion. With the current trend, Crypto will become the global leader in just a short time.

Therefore, from the perspective of global asset allocation, cryptocurrency assets are becoming increasingly difficult to ignore, and Mr. Dolphin decided to start tracking them.

Considering that regulation is still the biggest influencing factor at the moment and is still in the middle zone from strict to relaxed, we give priority to leading companies with good business models and high compliance attributes to conduct research.

The crypto asset series starts with $Coinbase(COIN.US). This article will mainly discuss Coinbase’s business model and the core logic of future growth. The next article will focus on stablecoins and calculate the future value of Coinbase and $Circle(CRCL.US).

The following is a detailed analysis

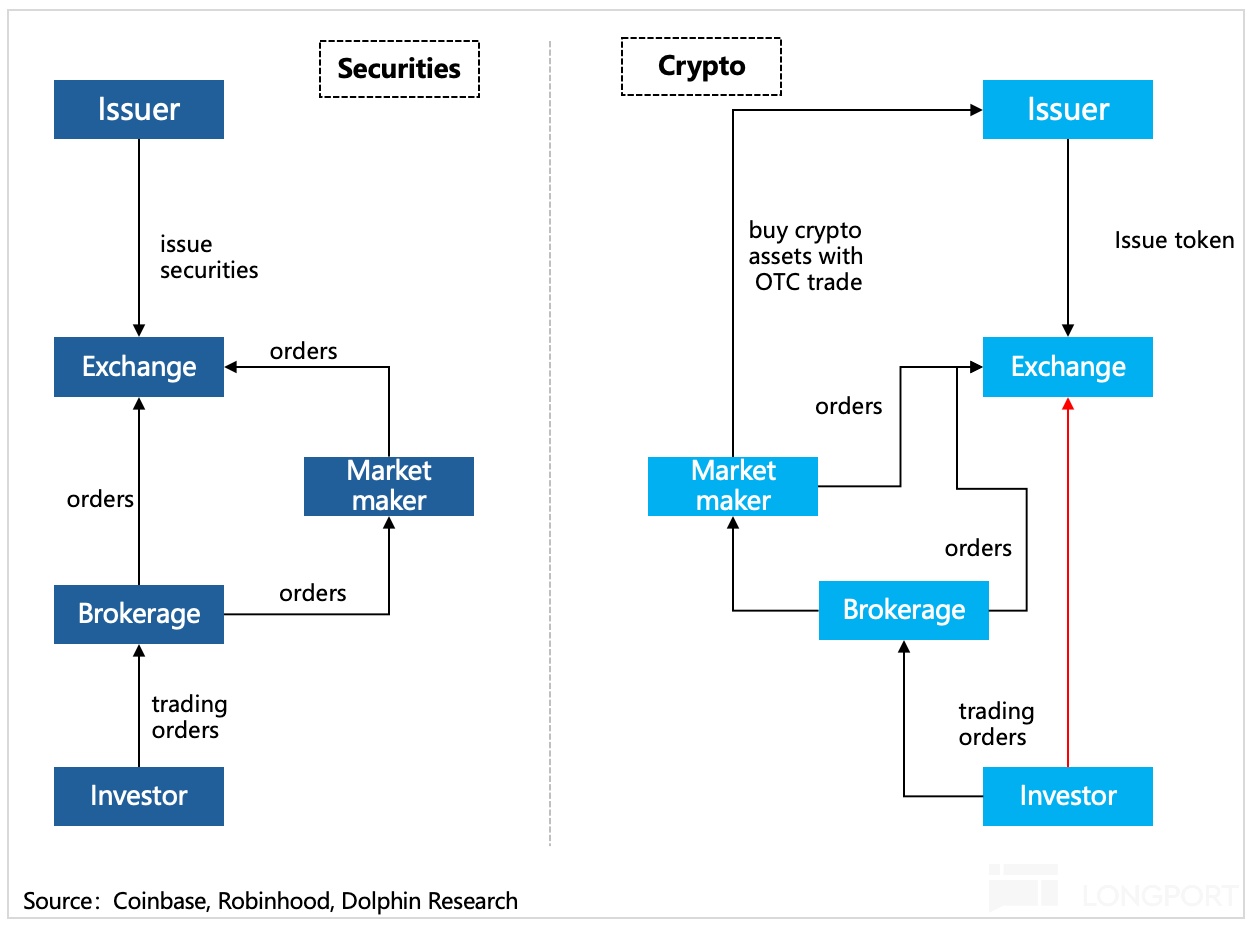

1. The exchange is not the end

If "cryptocurrency" is regarded as the target of a listed company in the stock market, or a commodity contract in the commodity market, then Coinbase is the New York Stock Exchange or CME Group. Its most basic function is to provide cryptocurrency quotations, matching, settlement and other exchange functions.

But unlike tradition, Coinbase has also seized the role of a "broker" – that is, it can directly face investors and provide services such as trading, lending, custody, staking, and cash withdrawals.

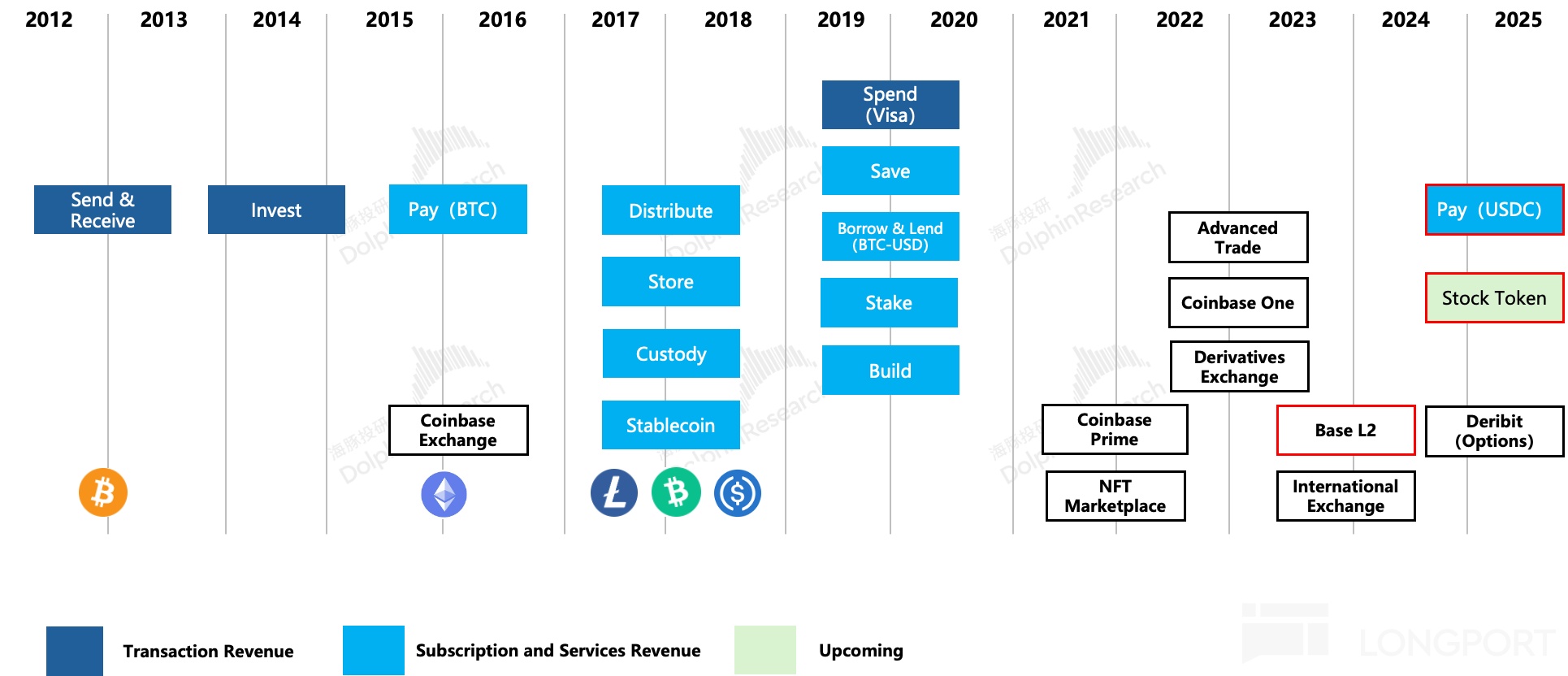

With the improvement of infrastructure such as digital wallets and merchant ecology, Coinbase quickly promoted payment scenarios mainly based on BTC. In 2019, it cooperated with Visa to launch Coinbase Card, allowing users to purchase physical goods with cards offline/online. However, an important reason for the slow promotion of payment scenarios is that the value of cryptocurrency fluctuates too much. Therefore, only after the stablecoin comes out and gets official recognition, Coinbase's payment scenario is expected to be truly promoted.

In addition to trading and payments, Coinbase is also applying for an equity token trading platform. Once approved by the SEC, it means that you can also invest in stocks indirectly on Coinbase.

At this point, Coinbase has a clearer blueprint for its future business landscape, which is to accelerate the listing of real assets on the chain and strive to create an on-chain comprehensive financial scenario platform, not just a pure cryptocurrency exchange.

Mr. Dolphin believes that payment and investment are key operations to expand the application scenarios of cryptocurrency, and the extension of scenarios means the expansion of the entire cryptocurrency market, which will also make more money for Coinbase, a "water seller."

In the cryptocurrency market, the existence of trading platforms such as Coinbase not only shortens the entire industry chain vertically, but also quickly and horizontally spans multiple demand scenarios. This is partly due to insufficient supervision of cryptocurrency in the past and the convenience of business expansion. For a leader like Coinbase, which is relatively top-notch in terms of scale and compliance, more penetration of supervision in the future will only help it eliminate potential opponents.

Therefore, we can naturally think that Coinbase should receive more profit distribution.

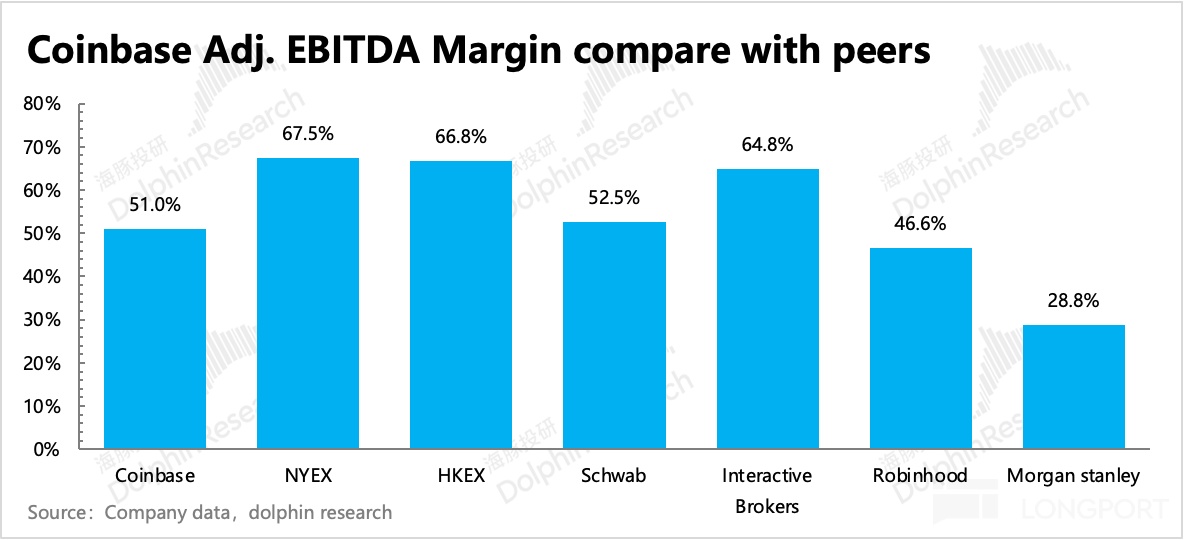

That's true, but Coinbase's performance has been inconsistent due to the high volatility of the cryptocurrency market. However, excluding the impact of special periods (such as listings, acquisitions, etc. that disturb short-term profit margins), profitability (measured by profit margins) in normal periods is still basically distributed in the range of 25% to 65%. Although the span is large, it can basically benchmark against mature traditional financial institutions.

Judging from the situation in 2024, Coinbase's profit margin is close to that of low-discount/commission-free brokers such as Robinhood, but lower than that of pure exchanges, indicating that it has not fully reflected the exchanges and more profit margins brought by the advantages of the industrial chain.

In the future, as crypto assets gain more universal recognition and continue to grow in the virtual currency market, as long as Coinbase's competitive position is stable, its profit margin upper limit will gradually be opened. In the end, Dolphin believes that it can reach a profit level that is more advantageous than traditional financial institutions.

2. Compliance advantages open up imagination space beyond “transaction”

So what kind of competitive environment does Coinbase face? Mr. Dolphin discussed the basic business and business model of Coinbase while sorting it out.

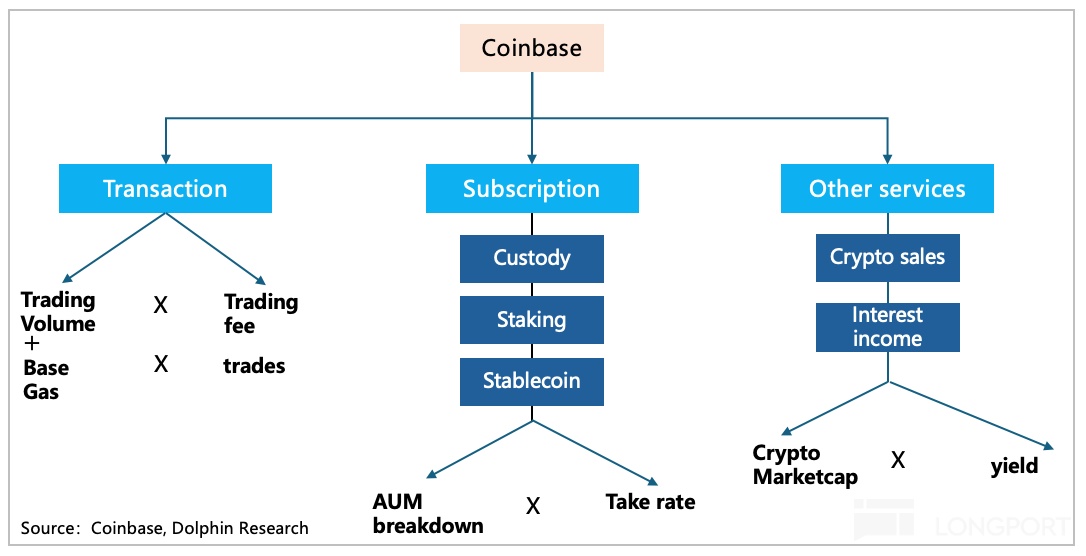

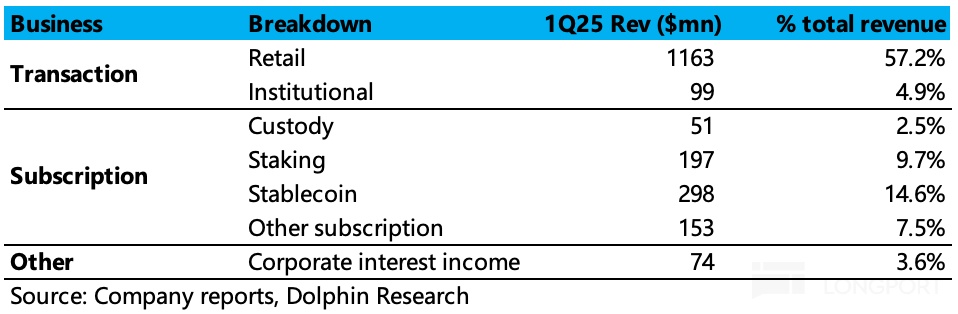

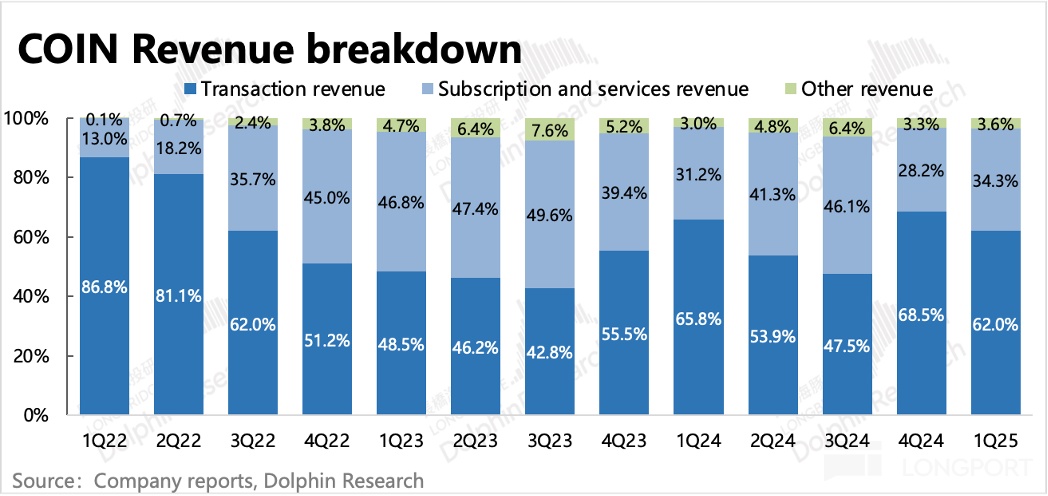

Looking directly at the figure below, from the perspective of revenue contribution categories, Coinbase has three main sources of revenue: transaction revenue, subscription revenue, and others.

Among them, trading revenue is highly susceptible to the impact of trading conditions, but it is also Coinbase’s current revenue generator, accounting for 50%. Subscription income and others (including custody settlement, staking, stablecoin, data/cloud, and company investment income, etc.) are more like a lubricant. Since the growth is relatively stable, it can slightly smooth the fluctuations in trading income.

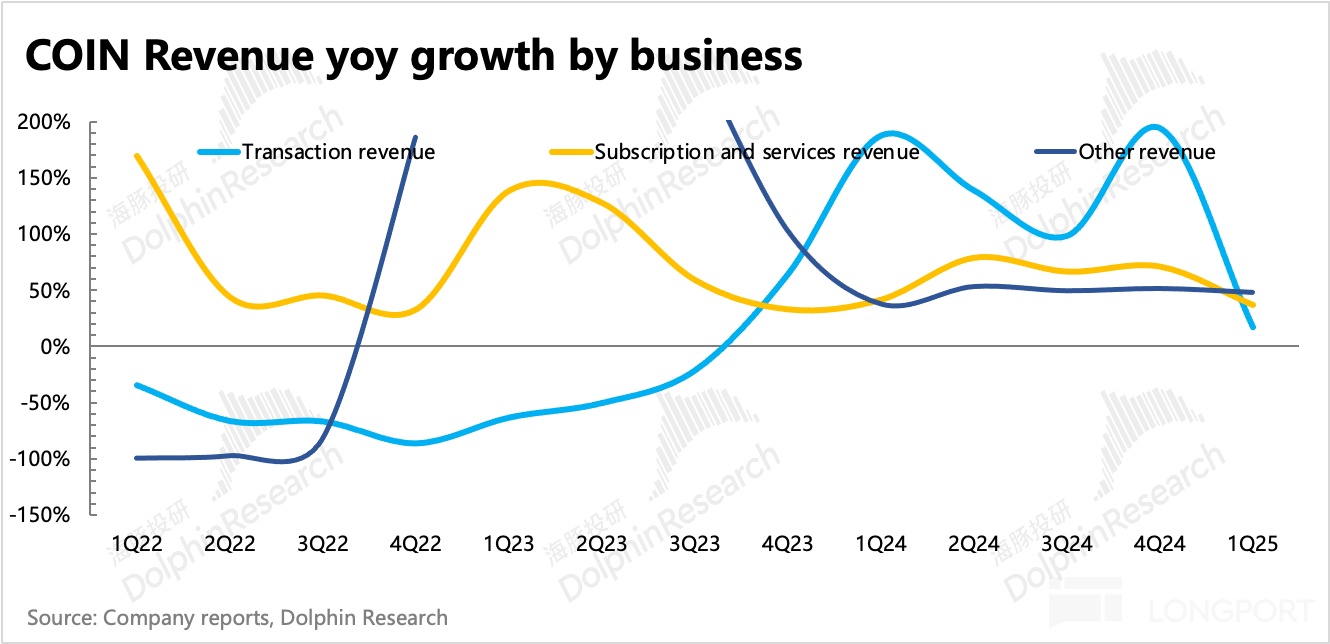

But an obvious trend is that as scenarios broaden, competition intensifies, and the structure of incremental funding sources changes, Coinbase will become less and less dependent on transaction revenue in the future.

1. Transaction thresholds will gradually be lowered

Compared with its peers, Coinbase's product advantages are compliance and security, but its disadvantages are high handling fees for retail investors and a shortage of derivatives trading varieties. However, due to these two shortcomings, Coinbase has been rapidly catching up with its peers in the past 1-2 years.

Source: CoinDesk

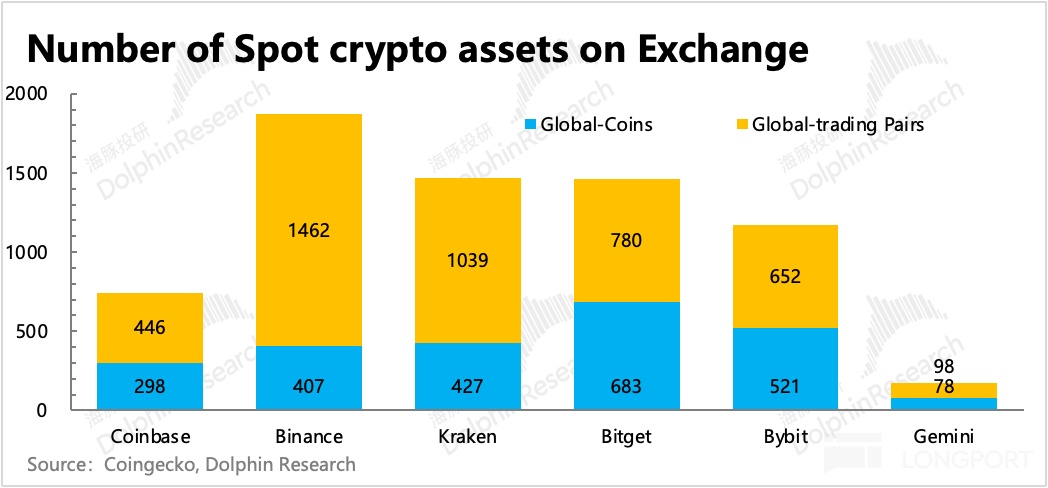

Coinbase currently operates three exchanges, Coinbase Exchange for spot trading, Coinbase International Exchange (CIE) for non-U.S. professional individuals and institutional transactions, and Coinbase Derivatives Exchange (CDE), a derivatives exchange transformed through the acquisition of FairX.

The above three exchanges cover the vast majority of nearly 300 cryptocurrencies currently in the market. In the US spot trading market, Coinbase is the absolute leader in terms of product coverage (compliance thresholds prevent peers from launching long-tail currencies on a large scale). But if you look at global regions and include derivatives transactions, the trading types covered by Coinbase are not at the top. For example, the gap with Binance and Bybit is obvious.

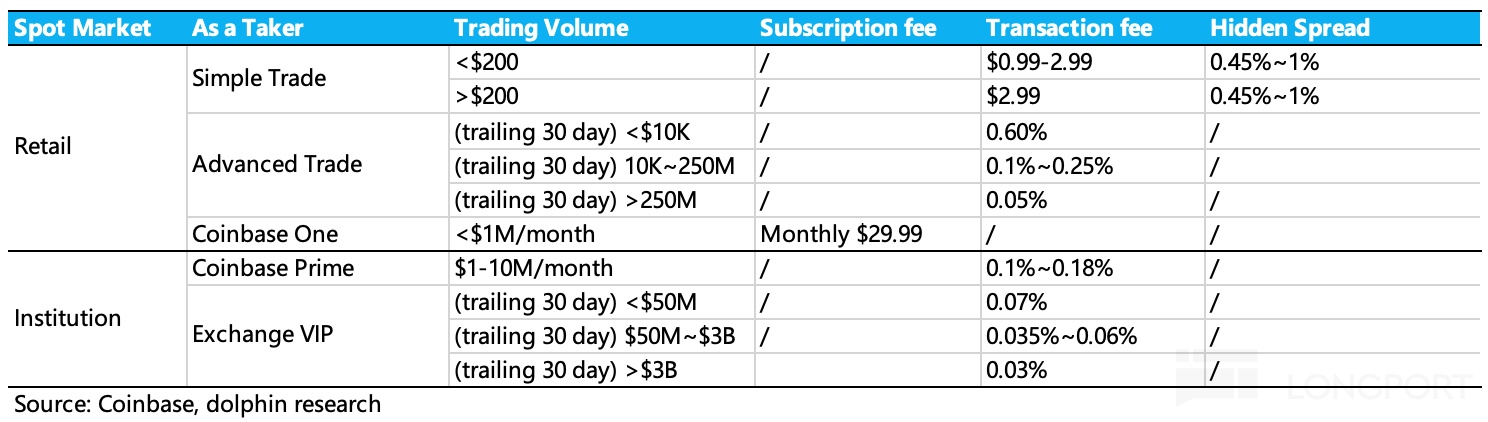

In addition to the range of trading instruments, the biggest difference in Coinbase trading includes transaction costs. Like traditional securities trading, Coinbase’s trading fees are based on trade size and a certain (tiered) rate. For example, the figure below shows the fee details of Taker (quick order taker) traders. Maker (pending order) traders' fees are generally lower than Taker:

For ordinary retail investors, the above-mentioned different transaction methods (simple transaction, advanced transaction, Coinbase one transaction) have different transaction costs. User transaction cost = "transaction rate + official hidden spread":

1) The transaction cost for retail investors can be as low as 0.05% and as high as 2.5% (at the end of 2022, for retail investors’ transactions of more than US$200, the transaction rate will be reduced from 1.49% to a maximum of 0.6%).

2) For institutional users using Prime or Exchange VIP levels, the rate quotation is in the range of 0.03%-0.18%.

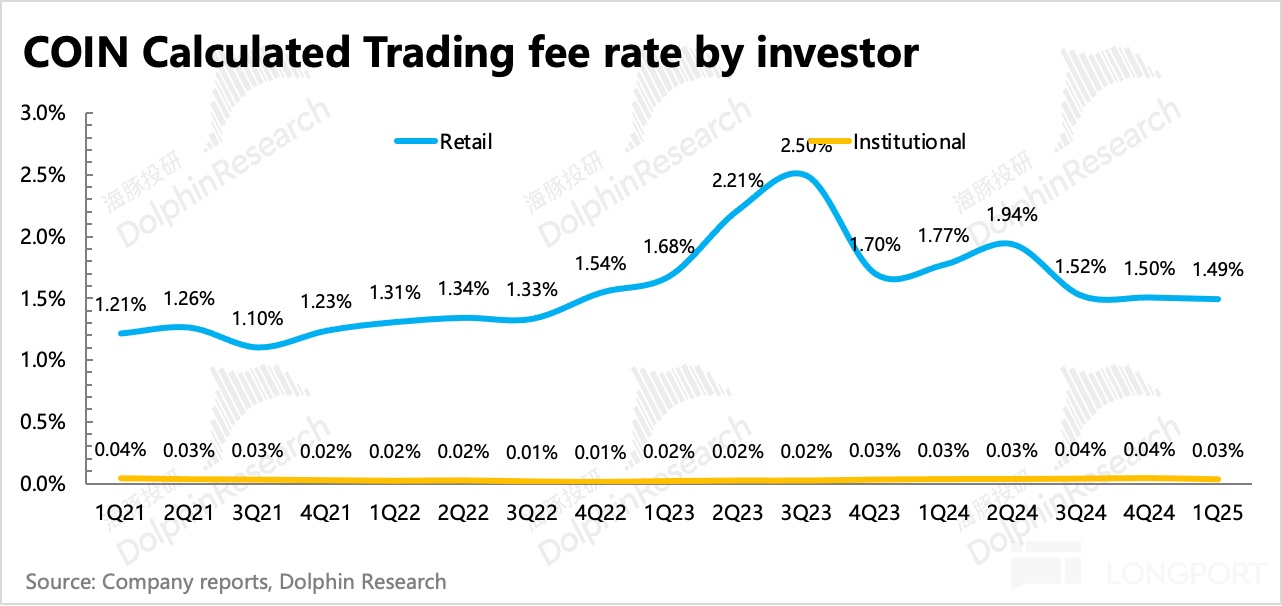

If we look directly at the comprehensive rates reflected in the final financial report, the transaction rates (including spread) for retail investors and institutions are 1.49% and 0.03% respectively. Compared with peers (especially exchange peers), this charging level is mainly for retail investors, and Coinbase does not have an advantage.

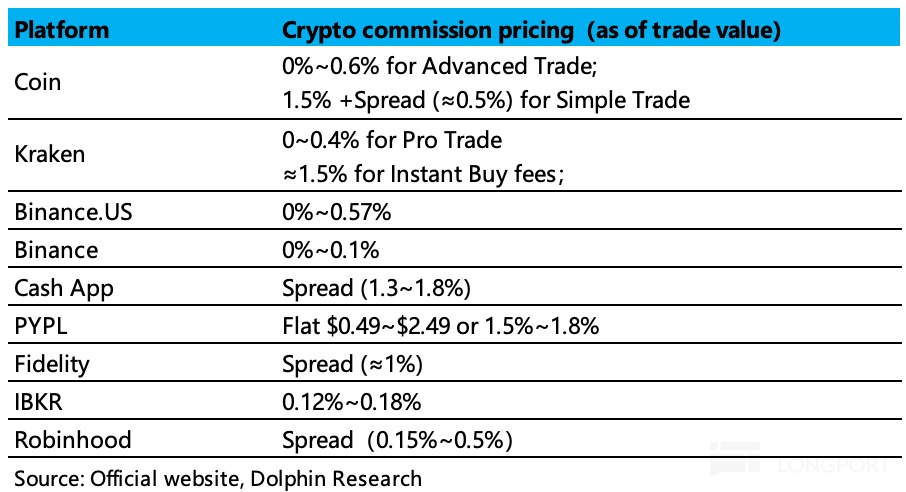

Taking Binance as an example, the highest-level fee rate for retail spot transactions is 0.1%, which is only 1/6 of Coinbase (after the Coinbase price reduction in 2023). If you use BNB (Binance Coin) to pay the handling fee, then this rate can be discounted by 25%.

As shown in the figure below, among other platforms that can trade cryptocurrencies, those with exchange attributes are cheaper than Coinbase. Other platforms that are mainly payment institutions will be more expensive. The transaction fees of discount brokers are also lower than Coinbase.

Coinbase has already had a fee reduction in August 2022, when Advanced Trade was launched. For users with a transaction volume of less than 10K in the past 30 days, the transaction cost (transaction fees Taker 0.6%, Maker 0.4%, basically no hidden spread) is less than half of Simple Trade (1.49% + about 0.5%spread).

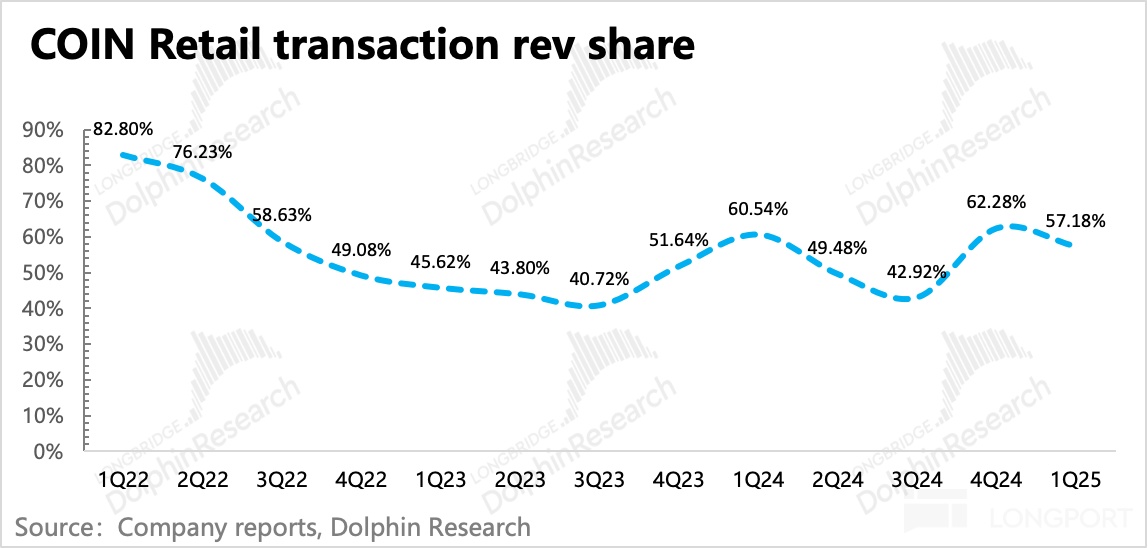

The small number of trading varieties (mainly derivatives) and high transaction costs can easily affect retail investors’ enthusiasm for trading. Although the Coinbase platform has the largest number of cryptocurrency assets in the world (12% AUC), Coinbase only accounts for 5% in terms of transaction size. This is only for spot prices. If derivatives transactions are included, Coinbase’s total transaction size will be directly outside the TOP10.

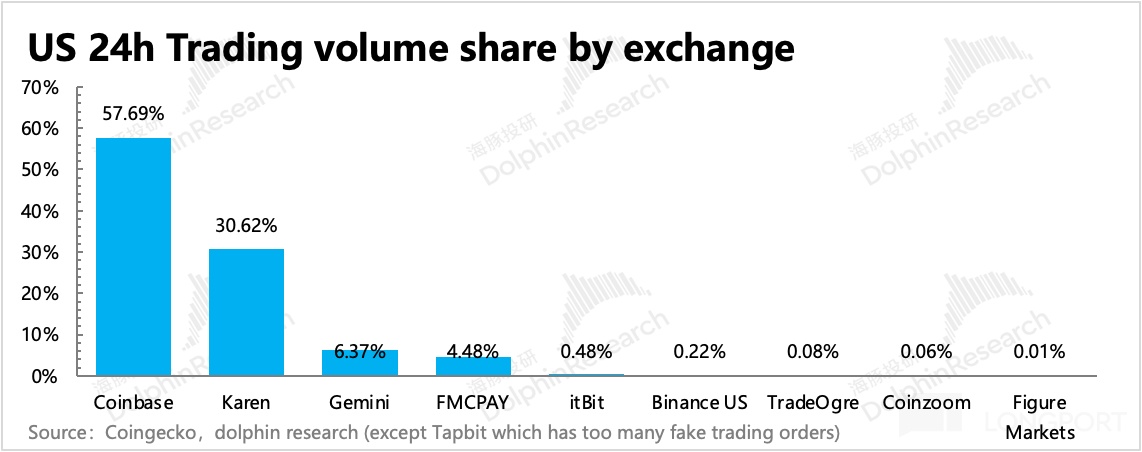

Only in the United States, due to license compliance issues, Coinbase can dominate the market, accounting for more than 50% of the country's spot trading volume.

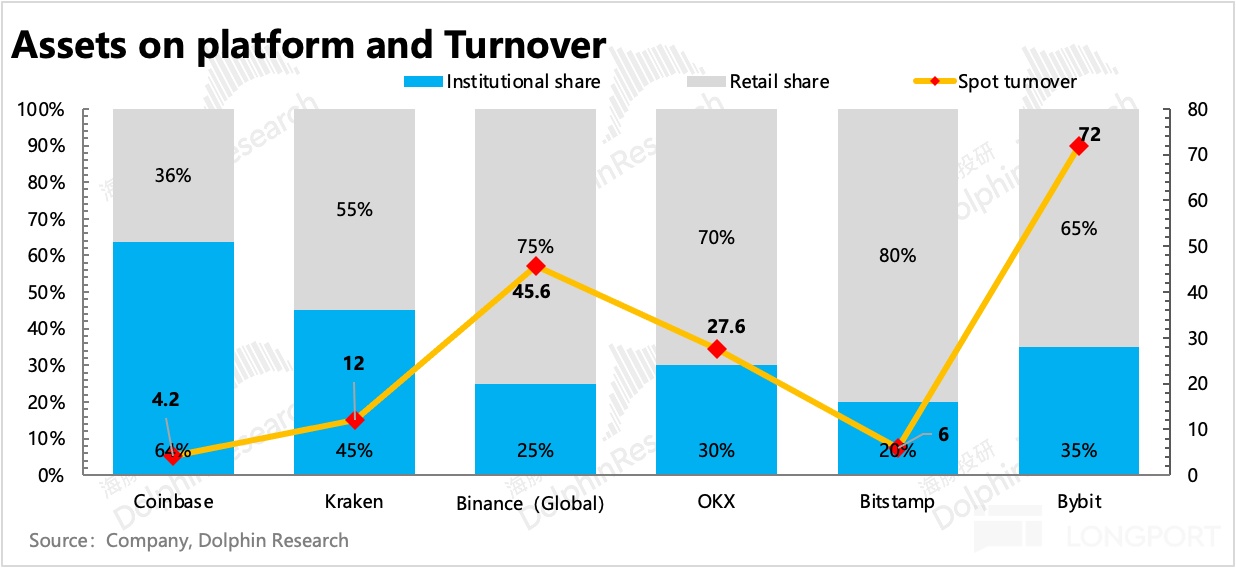

Why is Coinbase’s asset volume high, but its transaction size not large enough?

The problem lies in the turnover rate. Coinbase is significantly lower than its peers, and it does not have the high risk and high volatility characteristics of withdrawing crypto assets. But the turnover rate is just an appearance. Behind it is the difference in capital structure (user attributes), and user attributes are essentially caused by product features/advantages and disadvantages.

A common trading feature is that for current cryptocurrencies, the proportion of retail investors aiming for long-term asset allocation is constantly growing, and this group of users naturally trades at a low frequency. Currently, most institutions still use high-frequency trading to quantify fluctuation returns, but as mainstream funds are accelerating their entry, the overall trading frequency of institutions will decrease in the future.

Due to the limited number of trading varieties and higher transaction costs on Coinbase, it is not very attractive to high-frequency trading retail investors. However, its compliance and security have attracted high-net-worth retail investors with long-term allocations, as well as mainstream funds that also have strict compliance requirements for investment custody, both of which belong to low-frequency trading groups.

Of course, Coinbase is also very aware of its trading disadvantages and is working hard to catch up with its peers.

Regarding the problem of few trading varieties, Coinbase has accelerated the launch of new currency transactions and announced the acquisition of Deribit (the world's largest cryptocurrency options and futures trading platform) in early May to make up for its lack of derivatives trading varieties and related institutional customers. (For details about Deribit, Dolphin will discuss it after the Q2 financial report merges with Deribit)

Regarding the issue of high transaction costs, in fact, this is associated with the transaction scale. In the short term, Coinbase transaction fees remain high. In addition to bearing additional compliance costs and other technical fees (such as Base development costs), it may also be due to the low transaction scale, which makes it reluctant to lower the price to the bottom when "cutting oneself".

But from a longer-term perspective, Dolphin believes that Coinbase’s “price cuts” will continue soon.

(1) Relaxation of compliance, internal clearance, and intensified external competition

In the future, competition will not be limited to intra-industry competition among crypto asset exchanges. The growing threat will also come from external competition from traditional financial institutions.

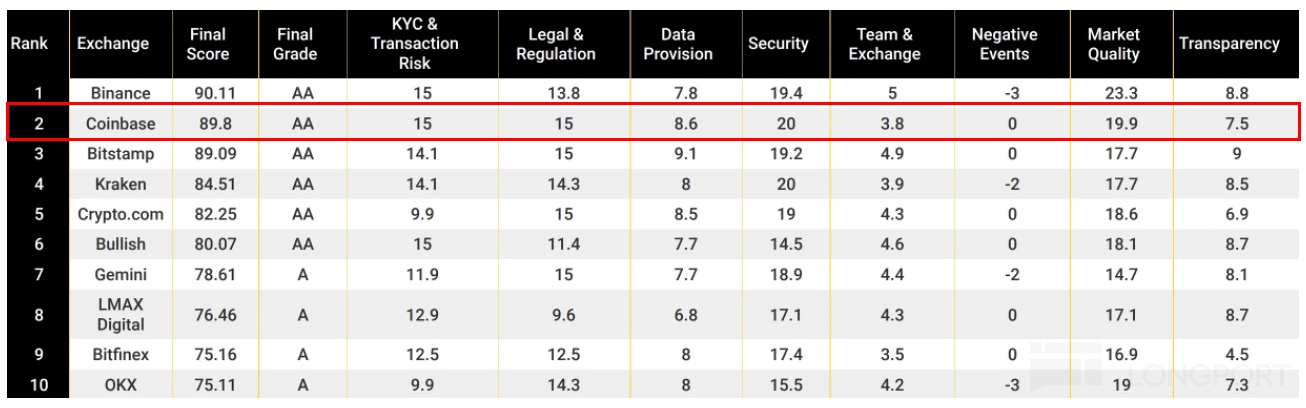

In terms of current competition in the industry, Coinbase's main advantage is "compliance", especially in the US market. The key to Coinbase being the only publicly traded cryptocurrency exchange is that it was also the first to gain access to operate throughout the United States.

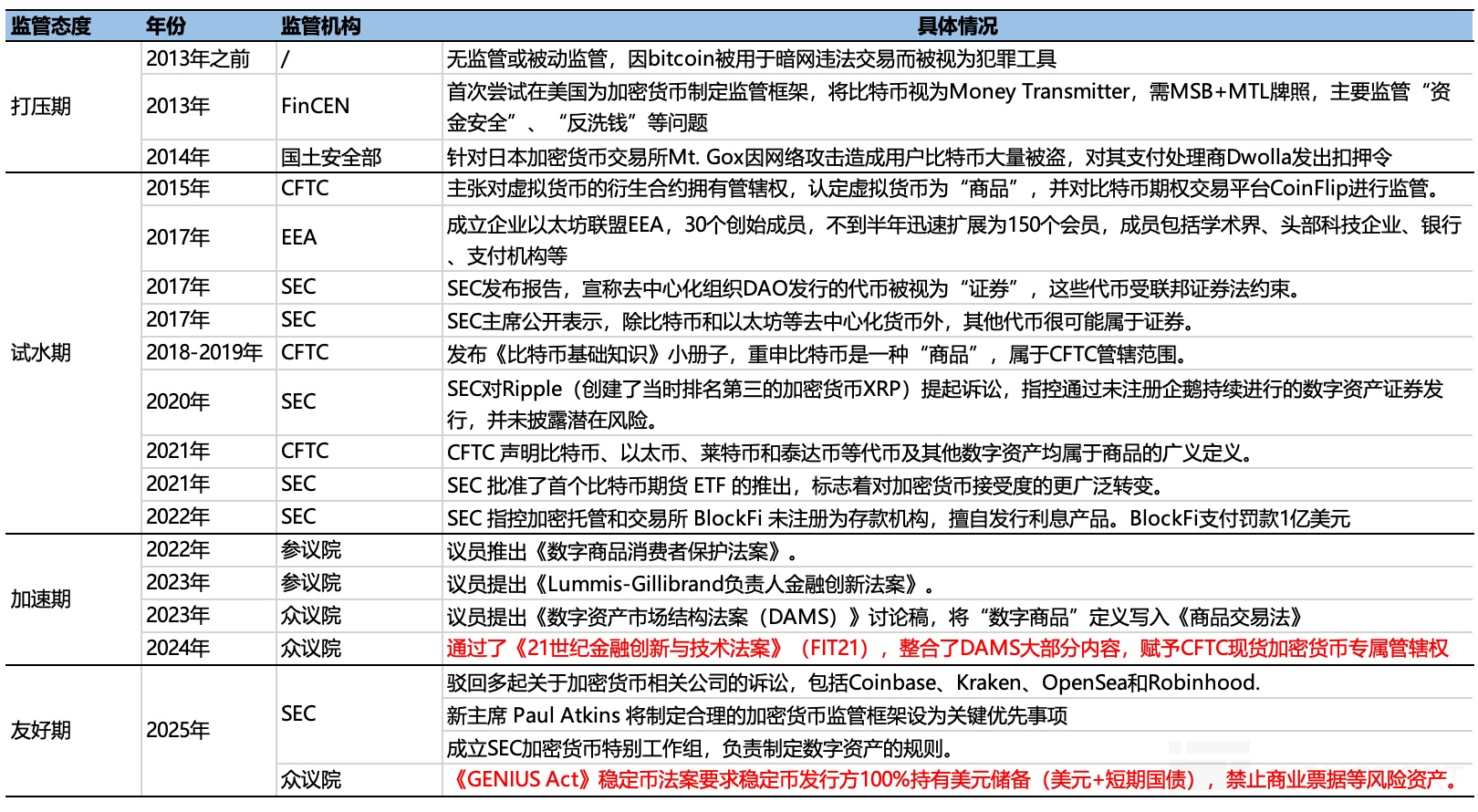

But the opposite of "compliance" is that it does not have an advantage in the types of trading assets (cryptocurrency types, derivative types). However, since 2025, with the active "platform" of the Trump administration, cryptocurrency has gradually been recognized by more mainstream officials.

The main method of “recognition” is to include it in the category of “friendly regulation” for non-suppressive purposes, of which the U.S. Market Structure Act and Stable Coin Act are the main drivers.

The Market Structure Act passed by the House of Representatives gives the CFTC exclusive jurisdiction over spot cryptocurrencies. If it continues to pass the Senate vote and the presidential signature and takes effect, it will mean the end of the jurisdictional dispute between the SEC and the CFTC.

The advantage of being regulated by the CFTC instead of the SEC is that it is more convenient to regulate:

1) No need to apply for an additional license (ATS+BD); 2) Reduce liquidation costs; 3) No information disclosure is required one by one for the listing of new tokens;

Under the jurisdiction of the CFTC, cryptocurrency exchanges that make derivatives only need to register with the broker, while those who make spot transactions do not even need to register with the CFTC. This not only saves high compliance costs (legal affairs, auditing, etc.), but also eliminates the need to modify the existing system to connect to the NMS-level clearing pipeline.

It is naturally a good thing that regulation is increasingly recognizing crypto assets. As more funds pour into the cryptocurrency market, leaders such as Coinbase that have done a good job in compliance will directly benefit, and long-tail small platforms will continue to clear out.

But at the same time, official recognition will also push traditional financial institutions to start boldly accelerating transformation. Especially some platforms that rely on business innovation to make breakthroughs will be more responsive to decisions at the forefront of the industry.

For retail users, such as brokerage Robinhood, or payment wallet Block, etc. The two platforms have supported the purchase and sale of cryptocurrency many years ago, and subsequently expanded into areas such as "merchant payment" by improving "investment scenarios". However, in view of compliance and security requirements, traditional financial institutions mainly focus on the top cryptocurrencies BTC, ETH, etc. "Fewer trading varieties" is their most obvious disadvantage facing the Coinbase platform.

However, as cryptocurrencies become more widely recognized, it is reasonable to imagine that traditional financial institutions will be more motivated to expand the scope of cryptocurrencies. These platforms with their own user and scenario advantages will compete more directly with Coinbase.

(2) More funds flow into institutions

Another impact of regulatory recognition is the change in the way capital flows. In the past, institutions involved in cryptocurrency market transactions mainly relied on the quantification of fluctuating returns. Mainstream institutions would have limited allocation scale due to compliance issues. However, as regulatory restrictions are opened, the participation of mainstream institutions will further increase in the future.

So for new retail investors, the way to allocate cryptocurrency may not necessarily require "in person". From the perspective of fund security and convenience, allocation can be done by investing in institutional funds.

Therefore, the market share of pure retail transactions will further shrink, and competition will not decrease but increase, and fee reduction will also become the only way for Coinbase.

2. Future added value will come from the expansion of on-chain scenarios

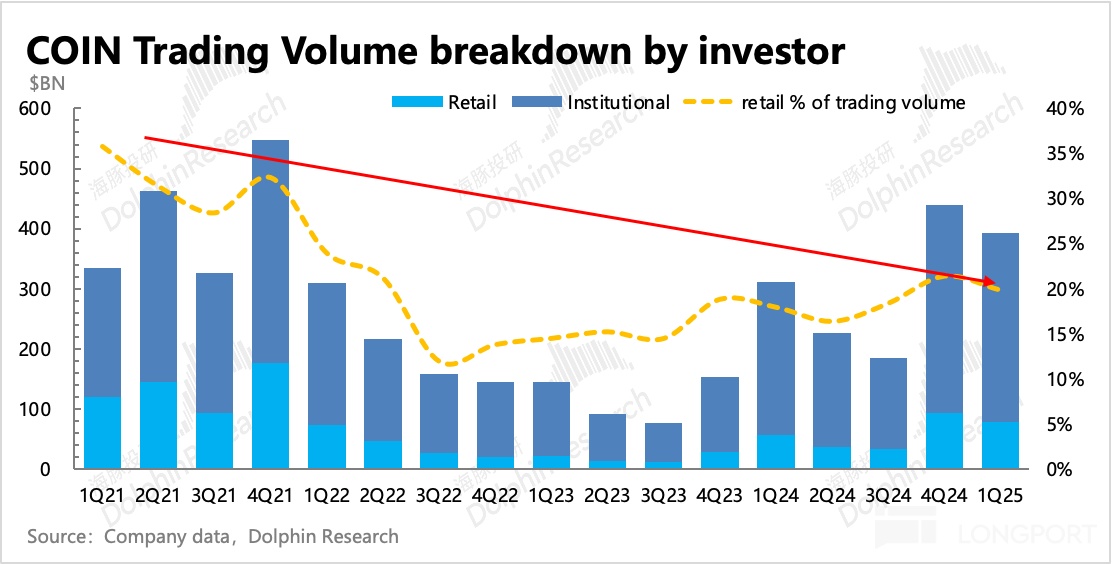

As of 1Q25, Coinbase's retail transaction revenue (transaction fees + spread) accounted for 92% of transaction revenue and 57% of total revenue. At the same time, the marginal profit brought by transactions is also very high, so if the fee reduction cannot immediately bring a significant increase in transaction size, then the fee reduction will have a very large impact on Coinbase's overall performance.

But since it is a major trend that cannot be changed, this means that developing non-trading income is crucial now and in the future.

Currently, Coinbase's non-trading revenue mainly refers to subscription revenue from comprehensive finance including custody, staking, stablecoins, and lending. For this part of the functional requirements, in addition to the development of payment scenarios, which relies more on retail users, the requirements for other scenarios mainly come from users with relatively large funds, so the service targets are mainly institutional customers.

Therefore, lowering the threshold for capital entry with lower transaction fees and expanding added value through comprehensive financial services are the reasons why Coinbase is more willing to go all the way to lower institutional transaction rates (to bring them in line with peer levels).

Let’s take a closer look at the segmented businesses that currently account for a relatively large proportion of the subscription business and will be able to simultaneously expand revenue scale as institutions enter the market in the future:

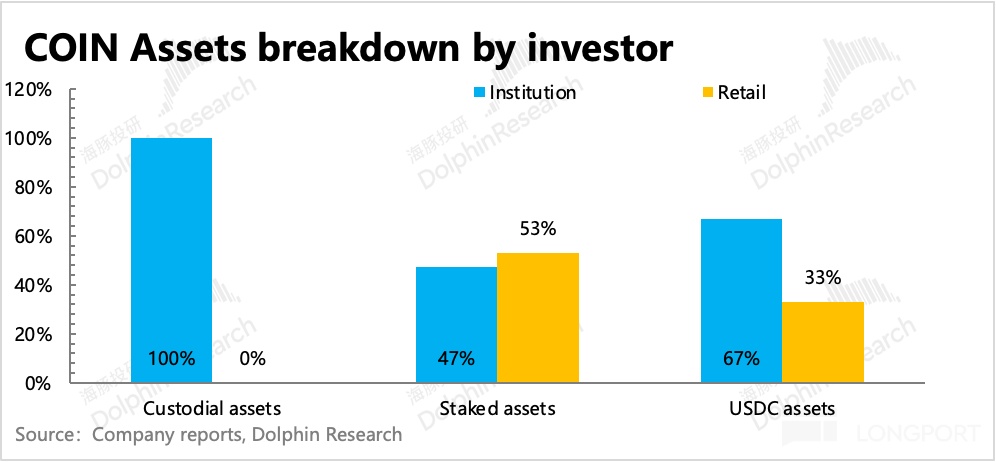

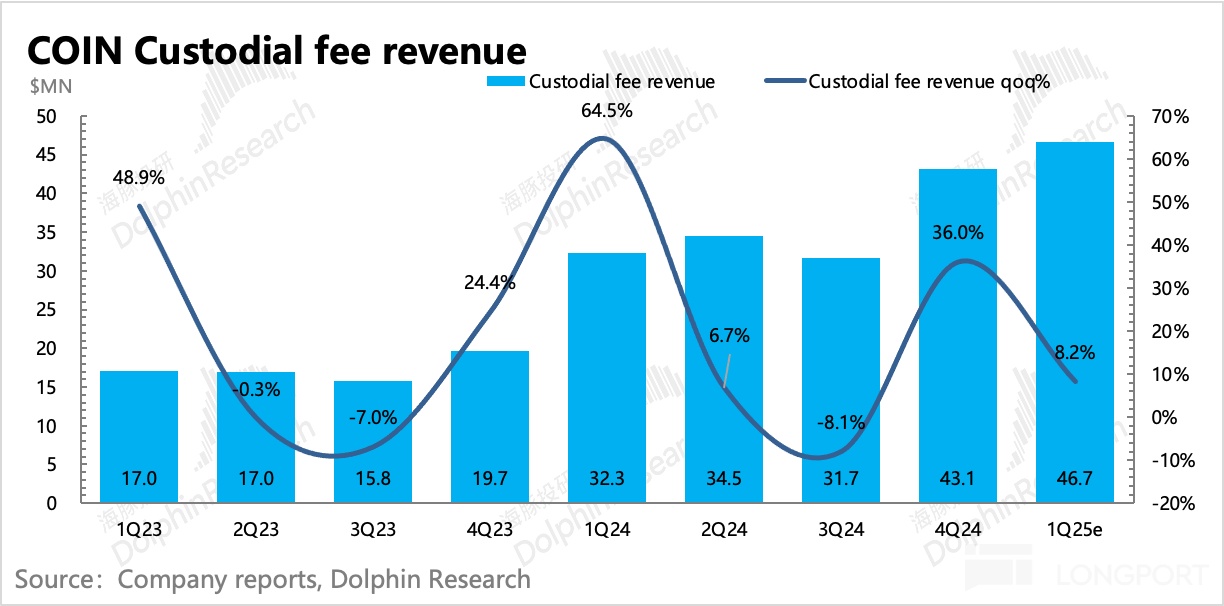

(1) Institutional custody: the easiest value-added service to develop

Fund custody is generally derived from trading business and is mainly for institutional customers. It provides services such as cold storage of cryptocurrency, 24*7 withdrawal process, insurance, auditing and compliance reconciliation reports. The calculated comprehensive custody fee is around 0.1%. (It will no longer be disclosed separately from the first quarter of 2025. The figure below shows Dolphin’s estimated value)

As rates are basically stable, the growth of custody revenue is mainly driven by the expansion of the institution's capital scale. For institutions, Coinbase’s compliance advantage is the first factor they consider when considering a platform. Therefore, for Coinbase, as long as the regulatory trend continues to be relaxed in the future, this revenue growth can continue.

But it will also face the problem of external competition in the long term. When traditional financial institutions that are more compliant and have cross-market assets are "dimensionally reduced", how can Coinbase attract more mainstream funds?

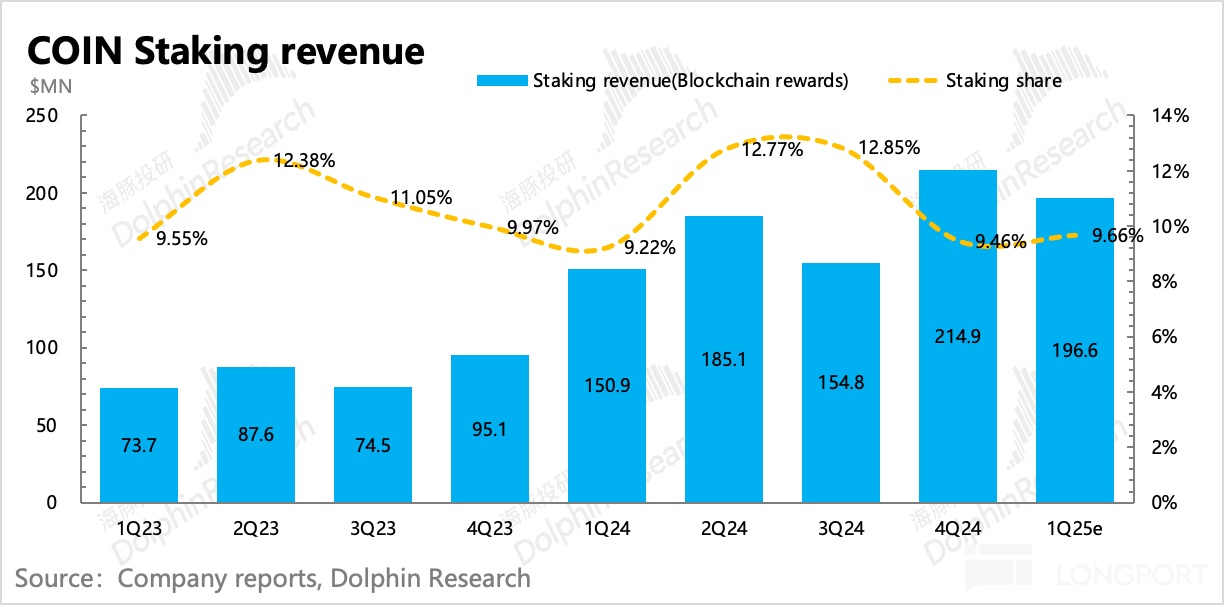

(2) Pledge income: There is a ceiling for mid- to long-term growth

Before joining hands with Circle in 2022, the largest source of Coinbase's non-trading business was crypto asset staking, which once accounted for nearly 13% of total revenue.

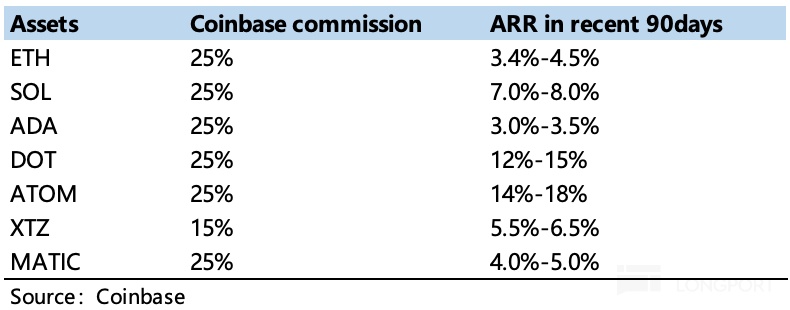

Crypto-asset pledge income is similar to the income gained by users investing in crypto-assets in mining projects (becoming a verifier of a mainstream PoS public chain), in which Coinbase shares a custody service fee. After Coinbase receives the revenue from the front-end, 25% of the money is retained by Coinbase, and the remainder is given to users.

The staking yield can vary greatly between different currencies, and is usually related to the stability of the currency's currency value, the inflation rate (the proportion of supply increase), and the degree of crowding (total pledge amount) competing to become validators.

The staking yield of leading cryptocurrencies is generally low, mainly because their supply is fixed or decreasing. However, due to the relatively stable currency value, the competition for validators to "employ" is too crowded. Since you need to have more "margin" (pledged assets) to become a validator, the income from single-coin staking will be diluted.

As shown in the figure below, the Ethereum pledge return rate of the top ETH is 3.4%~4.5%, but the return rate of the small currency DOT Polkadot is 12%~15%.

In the short term, pledge income will basically expand with the expansion of the scale of pledged assets. However, in the medium to long term, when the supply is relatively limited, the block production rate of high-quality cryptocurrencies will trend downward. Even if the block production rate of low-quality/niche cryptocurrencies is high, the currency value may not be high or fluctuate. After the staking incentives are actually converted into U.S. dollar values, the actual staking yield is actually not high. Therefore, this trend will limit the long-term growth space of pledge business income.

It seems that (1)-(2), Coinbase’s subscription business, with the expansion of the cryptocurrency market pie and stable competitive advantages (security, compliance, official website) in the short and medium term, there is no need to worry about growth. However, if traditional institutions accelerate their demise in the long term, what is the reason why Coinbase can still be regarded as the “preferred” among mainstream institutions?

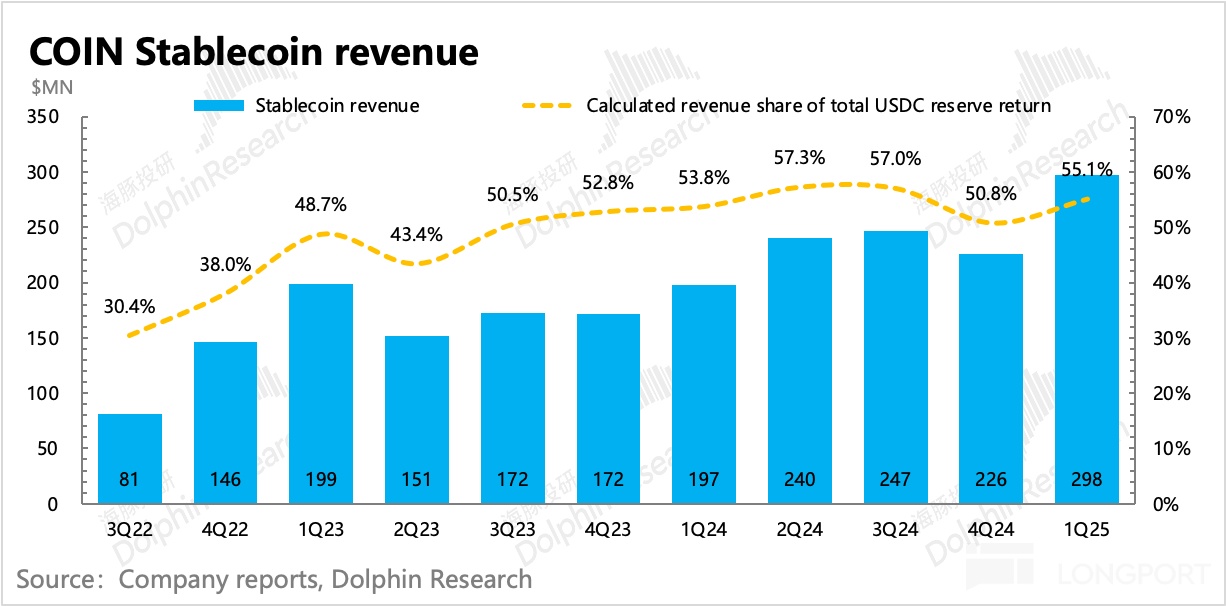

The answer is (3) stable currency business. On the one hand, the cryptocurrency pie will be enlarged. With official recognition, real assets will be uploaded to the chain faster. Funds will no longer flow into the cryptocurrency market due to speculative demand, but will become a more stable payment and store of value. On the other hand, Coinbase's excess advantage comes from its current special position in the USDC industry chain.

Therefore, the stablecoin business, which accounts for 15% of revenue, is the main artery for Coinbase's future growth, and is also the key to determining whether Coinbase's valuation has been reached. At present, Coinbase's comprehensive share ratio in the stablecoin business reaches 55%, but the actual USDC holdings on the platform only account for 17%. It is obvious that Coinbase has a "privilege".

But the problem is that part of Coinbase’s special position on stablecoins stems from its deep tie to Circle. However, the interests of both parties are not entirely consistent. Based on user demand, Coinbase may provide similar distribution facilities to USDT, another stablecoin with a larger market size. After Circle is listed, it will also demand growth in revenue, thereby trying to obtain a larger share ratio.

These business differences, as far as Coinbase currently has a small amount of equity investment in Circle (the Center alliance, in which both parties held 50-50 shares in the early days, was disbanded in 2023, and the USDC issuance rights were vested in Circle), it is difficult to guarantee that the expansion of the differences will not affect the cooperation between the two parties:

For example, at the end of last year, Binance, a competitor of Coinbase, was introduced into ecological cooperation. Although Binance's share is very low and almost negligible, it actually weakens Coinbase's competitive advantage due to USDC.

In addition, Circle is also increasing its share of total revenue by grabbing USDC balances (rebates through its Mint wallet to encourage market makers and local payment companies to keep funds to be issued in Mint instead of exchange wallets), and by expanding the demand scenarios that must be connected to issuers (such as cross-chain bridges, Tokenized T-Bills, and traditional clearing).

The 2023 agreement has an agreed period of 7 years, that is, before 2030, the sharing of interests between the two may not change much. Enlarging the USDC cake is certainly a top priority (the scarcity of Circle begins to be questioned after a 6-fold increase), but what about after seven years?

With the expected market size of trillions, how much can USDC get? In the USDC ecosystem, Coinbase and Circle, one owns the scenario side and the other controls the issuance side. In the end, who will have more say? In other words, who has greater value in the future, Coinbase or Circle? In the next article, Mr. Dolphin will focus on the discussion around stablecoins.

Risk disclosure and statement of this article: Dolphin Investment Research Disclaimer and General Disclosure