The A-share market on January 29 directly divided investors. On one side, resource stocks were frantically grabbing their daily limits. Hunan Gold, Sichuan Gold, and Yuguang Gold and Lead were stuck at their daily limits. Silver and non-ferrous metals soared 10.04% in one day, and the total market value suddenly reached 102.26 billion. On the other hand, the GEM Index fell 1.8% and fell below 3,300 points. More than 3,100 stocks were green, and nearly 30 stocks fell directly to their daily limits. More importantly, the "bad news" that everyone has been waiting for for a long time has finally come to fruition. Many people are holding money in their hands and are worried: resource stocks are so popular and the bad news has just come out. Should they increase or reduce their positions now? In fact, there is really no need to panic. Once the logic behind it is straightened out, the operation will naturally have a direction.

First, let’s talk about why resource stocks suddenly broke out collectively. This is not just speculation, it is all supported by solid logic. First, commodity prices are rising. Since January, the US crude oil 2606 contract has risen from US$57/barrel to US$61.7/barrel, an increase of nearly 8%. Energy resources stocks such as oil and coal have followed suit. Nonferrous metals are even more powerful. The Shenwan Nonferrous Metals Index has risen by 94.73% in 2025, and has risen by 18.59% since January 2026. Gold, copper, and aluminum are not as strong because of the US dollar, and everyone feels that the global economy is about to recover, and prices have been rising. Let’s talk about the gold sector. Hunan gold, Sichuan gold, and China gold hit their daily limit on the same day. This is because gold can serve as a safe haven. The global situation is now a bit uncertain, and funds are crowding here.

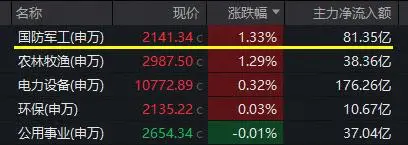

Secondly, funds are "changing places", moving away from the previously popular theme stocks such as AI applications and consumer electronics, and investing in sectors such as resources and finance that are supported by performance. Data show that on January 29, the transaction volume of the two cities was 1.42 trillion yuan, with 4.5 billion yuan of funds flowing in from the non-ferrous metals and coal sectors, while 6.2 billion yuan and 4.8 billion yuan from the media and consumer electronics sectors went out. Why change? The main reason is that the end of January to the beginning of February is a period of intensive annual report forecasts. Many theme stocks have no performance and funds are afraid of being depleted. However, resource stocks have followed the increase in commodity prices and the certainty of making money in annual reports is high, so they have naturally become a "safe haven" for funds.

There is also implicit support from policies. The country’s “15th Five-Year Plan” clearly states that it will accelerate the development of emerging industries. Resource recycling and new energy materials are key directions. Many resource stocks are on this track. For example, lithium, cobalt, and nickel in non-ferrous metals are the core raw materials for new energy vehicle batteries. Now that there are more and more new energy vehicles, the demand will only grow. In addition, on January 19, the central bank lowered the re-lending and re-discount rates by 0.25 percentage points, releasing funds to support the real economy, and the procyclical resource sector directly benefited.

Let’s talk about the “bad news” that everyone is most concerned about. The new regulations on integration were implemented on January 19. The new regulations increase the minimum financing margin ratio from 80% to 100%, and new financing cannot use the previous leverage. Many people are worried that market funds will tighten. But the actual situation is that this bad news has been digested by the market for almost 10 days, and the new regulations are "new and old". The previous financing balance of 2.7 trillion yuan will not be affected, and the market average maintenance ratio of guarantees is as high as 288%. The actual impact is not that big. On January 29, 5.68 billion yuan of northbound funds flowed in, which shows that foreign investors did not take this bad news seriously at all. Instead, they took advantage of the market adjustment to add positions in heavyweight stocks such as banks and semiconductors, which indirectly boosted the popularity of resource stocks.

So here’s the question, what should we do now, after a bad news and resource stocks hit their daily limit? It is definitely not possible to blindly chase the rise. Only rational layout is reliable. You can refer to these three suggestions.

First, don’t blindly buy stocks with their daily limit in mind. You must choose the right segment. Resource stocks are not monolithic and have different logics in different fields. Precious metals such as gold and silver are mainly driven by risk aversion and the weakening of the US dollar. They are suitable for short-term layout. If you have spare money, you can allocate small positions, but don't chase highs and wait for a correction before buying. Lithium, cobalt, and nickel among non-ferrous metals benefit from the long-term demand for new energy vehicles and energy storage, and are suitable for long-term holding. Focus on companies with stable production capacity and long-term cooperation with leading battery manufacturers, whose performance is more reliable. Traditional energy resource stocks such as coal and oil follow the fluctuations in commodity prices. You can pay attention to them in the short term, but you must pay attention to the rhythm and do not stand guard at high prices.

Second, control the position and enter the market in batches. Don't put all your eggs in one basket. Now the market is clearly divided. The Shanghai Composite Index is oscillating around 4150 points supported by heavyweight stocks, but the ChiNext Index has fallen sharply, and the profit-making effect is not good. In this case, don’t place heavy bets on resource stocks. It is recommended to control the position at 30% to 50%, and use some funds to test it out first. For example, if you are optimistic about a certain color stock, buy half of it first, and then cover the position after a correction. Don’t be greedy if it continues to rise, and close as soon as you see good results. At the same time, it can be paired with some financial stocks or stocks in stable growth sectors to balance risks. For example, bank stocks have low valuations and stable dividends, which can hedge against the fluctuations of resource stocks.

Third, look at performance in the long term and policies in the short term to avoid the trap of high valuation. Resource stocks are rising now, and the core is the certainty of expected performance increases. Therefore, when choosing stocks, you must read the annual report preview, and give priority to companies with clear performance growth and reasonable price-to-earning ratios. Don't buy stocks that have no performance support and rely solely on conceptual speculation. For example, some resource stocks have more than doubled, with price-to-earning ratios as high as hundreds of times. Even if they are still rising in the short term, don't chase them. The risk is too high. In addition, we should pay attention to policy changes, such as the pace of subsequent interest rate cuts by the Federal Reserve and Indonesia's nickel mining quota policy. These will affect commodity prices and in turn affect the trend of resource stocks, so be prepared to respond in advance.

There is also a market signal to pay attention to: January 29 is "big tickets stabilize the market, small tickets are under pressure". Weighted indexes such as the Shanghai Stock Exchange 50 and CSI 300 are rising, while the CSI 1000 and ChiNext are falling. This pattern may continue until the Spring Festival. Therefore, in operation, we should favor leading resource stocks in the mid-to-large caps and avoid small-cap resource stocks. Small-cap stocks have weak capital capacity. Once the market sentiment turns, they will fall harder than large-cap stocks.

In fact, from a long-term perspective, the current environment for A-shares is not bad. In terms of policy, "stability is the top priority", the China Securities Regulatory Commission is promoting the entry of medium and long-term funds into the market, and the central bank is also releasing liquidity; in terms of industry, the procyclical sector has benefited from economic recovery, and tracks such as new energy and resource recycling have long-term growth logic. The rising trend of resource stocks is essentially the pursuit of performance certainty by funds, but the negative news on January 29 gave rational investors an opportunity to enter the market.

However, there is no guarantee of profit or loss in investment. Although resource stocks are strong now, they also have the risk of volatility. For example, commodity prices may fall back, and policies may be fine-tuned, all of which will affect stock price trends. Therefore, we must remain rational in operations, do not be dazzled by the short-term rising limit trend, and do not panic and cut meat because of a single negative.

In the final analysis, the A-share market split on January 29 was the result of funds re-finding their direction after the bad news came to fruition. The rise of resource stocks is supported by both performance and policies. It deserves attention but is by no means a reason to blindly follow the trend. Choosing the right segment, controlling positions, and keeping a close eye on performance and policy changes are the keys to surviving market fluctuations before the Spring Festival. The structural opportunities of A-shares have always been hidden in rational judgment rather than following the trend of short-term emotions. As the pace of economic recovery gradually becomes clearer and policy dividends continue to be released, those targets that are truly supported by performance and in line with industry trends will eventually gain a firm foothold in the market and bring continuous value returns to investors.