The Shanghai Composite Index has been positive for five consecutive times, the market liquidity crisis has been resolved, and Lingjun was punished with a "boomerang", but quantitative trading has once again been pushed into the spotlight of public opinion.

After experiencing a sharp retracement of net worth and a series of pressures from customer redemptions, micro-cap stocks rose sharply for two days. Unexpectedly, the 24 hours before and after the quantitative private equity giant Lingjun was fined was the real "darkest moment" of quantification.

The resurgence of rumors, the announcement of Lingjun’s punishment, and the late-night apology have triggered a huge discussion in the entire industry about “why we have come to this point” and “where we will go from here” in quantification. Reporters from the Financial Associated Press have followed up on quantification for a long time and interviewed many institutions. They reviewed the 24 hours of quantification and the three major doubts that still exist in the industry.

Where does quantification go from here? Three major questions in the industry

Following Lingjun’s punishment, it was reported on the Internet that a quantitative private equity person said that “China’s stock market quantitative funds have closed down.” Such remarks were immediately denied by the parties involved.

What is unavoidable is that after the fermentation of news events, the great discussion about quantification has once again begun: How did the industry review the unprecedented tragedy of quantification? Investors asked, "Can I still invest in quantitative trading after a sharp retracement?" Some people once again mentioned the 828 incident in 2023 and reiterated the quantitative selling.

Some asset managers also believe that quantitative supervision needs to put the establishment of capital gains tax on short-term trading on the agenda.

Focusing on this, reporters from the Financial Associated Press interviewed industry insiders and learned that the current industry still has the following three major questions that need to be answered:

First of all, how to control the size of orders when placing quantitative trading orders?

Previously, the new regulations on programmatic trading clarified that high-frequency trading is the focus of supervision: that is, if the maximum declaration rate reaches more than 300 transactions per second or the maximum number of declarations in a single day reaches more than 20,000 transactions, the transaction can adjust the abnormal transaction identification standards according to the situation. In the announcement of the punishment of Lingjun by the Shanghai and Shenzhen Stock Exchanges, the reason was that "a large number of orders were concentrated in a short period of time, which accounted for a high proportion of the market turnover during the period, triggering a rapid decline in the index and seriously affecting the trading order."

Quantitative private equity said that even if it is not high-frequency trading, there is a lot of quantitative daily rolling trading frequency. Generally, it is sold at the opening and the funds are withdrawn before buying. From the current regulatory direction, in addition to avoiding high-frequency trading, it is also necessary to consider whether it will affect the index performance.

Secondly, will quantification “stop”? How to balance benefits and risks?

From the perspective of the industry, the risks of quantitative private equity are not without signs, but most people choose to run blindly.

A certain quantitative private equity said that the company adjusted its strategy last year because it realized that the CSI 500 was very risky and not cost-effective. However, the market enthusiasm concealed that the index had no excess risk. Looking at the excess and returns brought by the risk, how to balance it?

The above-mentioned people said that at that time, the risks had not yet emerged, and not doing this part of the excess would bring about underperformance and investor complaints. Today, if you review the market, you will find that rationally facing the excess of 300, 500, and 1,000, accepting the attenuation of alpha is an objective law. Trying to use opportunistic tricks such as iteration to chase false excess will ultimately be short-lived, and the worse result will be backlash.

However, in the face of huge temptation, how many institutions in the market can predict the risks? Dare to make adjustments? In most cases, extreme risks come and it is impossible to escape unscathed.

Third, how big is the current scale of DMA? How much money has 4 times leverage leveraged in the market?

It is undeniable that some quantitative private equity companies have criticized the restrictions on DMA trading before the holidays, and some institutions have blamed this for the retracement of net worth. In fact, in reviewing the sharp decline in micro-cap stocks, how much impact will DMA's restricted trading have on the product? The industry is inconclusive.

Industry insiders said that the path to triggering the liquidity crisis of micro-cap stocks is very clear. It was triggered by Snowball’s knock-in, and Snowball hedged and sold futures. The bulls chose to wait and see because they were waiting for the risk to be released, which in turn triggered a widening of the discount, a domino effect, and quantitative neutral strategies to close positions and sell CSI 500 and CSI 1000 constituent stocks. Subsequently, regulatory measures such as securities lending accelerated the decline of small and micro stocks, and the liquidity crisis really began. High-leverage DMA positions were liquidated. The DMA was restricted from February 5 to February 8 of the same month, for a total of 4 days.

Judging from the decline in quantitative net worth, it started with the decline of the Wind micro-cap index in January this year, reaching its maximum retracement in the last week before the Spring Festival, with individual products falling by more than 20% in a single week. In the view of most observers, the selling restrictions have exacerbated the retracement of net worth, but the retracement cannot be entirely attributed to regulatory measures.

In addition, it is worth noting that regarding whether securities firms can restrict the selling of quantitative private placements, in fact, there is a clear explanation in the 2023 programmatic trading. In strengthening the front-end management of members (brokerages), the exchange proposed that if customers’ programmed transactions may affect the security of the trading system or the normal trading order, members (brokerages) can take measures such as rejecting their programmed trading entrustments and canceling relevant declarations.

From the last day before the Spring Festival to the present, small and micro-cap stocks have started to rebound. In four trading days, the Wind micro-cap stock index has increased by nearly 30%. While the micro-cap market is still worth looking forward to, what is the size of DMA? What potential risks does high leverage bring? It deserves industry attention.

Regarding the scale of DMA, the industry speculates that as of the end of last year, the stock scale may have reached 100 billion. Counting 4 times leverage, the market capital leveraged is about 400 billion to 500 billion.

How big is the impact on the market? An analysis by an organization estimates that there is a certain diminishing effect when the scale changes hands. From observation, the turnover rate of tens of billions of private equity can reach 200 times when it reaches 500 million, about 120 times when it reaches 4 billion, and the turnover rate of tens of billions of scale is about 30 to 40 times. From this, we also refer to the turnover rate of DMA. Returning to what the regulator mentioned, "there are also problems such as strategic convergence and transaction resonance at some points in time, which increase market fluctuations". There are also traces to follow.

Full review 24 hours before quantification

The first stage (February 20, 12:00-15:00): Storm is coming, rumors are flying everywhere

Beginning at noon on February 20, a link to a collection of rumors about quantitative private equity giants was spread on social platforms. The rumors were mixed with "the liquidation of hundreds of billions of quantitative products, a huge loss of 1.5 billion in self-operated products, a DMA debt of 6 billion, the company's bankruptcy and even jumping off the building." The main body of the rumors involves Huanfang Investment, Mingtun Investment, Jiukun Asset and other leading quantitative private equity institutions.

These rumors before the Spring Festival have once again spread in the form of a collection and intensified. A reporter from the Financial Associated Press verified with a number of quantitative private equity and third-party institutions that the micro-cap liquidity crisis has caused the net value of some products to retreat. It is true that some products have encountered greater redemption pressure and even been liquidated, but there is no "liquidation of hundreds of billions of products." Some companies bluntly said: "The above screenshots are rumors. There were rumors of bankruptcy and jumping off buildings before the Spring Festival. These extreme statements are not true." Some leading quantitative private equity companies also said that the company does not have DMA products, and there is no problem of owing huge amounts of money to brokers.

The second stage (15:00-24:00 on February 20): Punishment is implemented, supervision is quantitative and qualitative

There are still a lot of messages asking for confirmation, and regulatory penalties have pushed the discussion to a climax. It is worth noting that this is the first time a penalty decision has been implemented after the new regulations on programmed trading in September last year, and the target of punishment is Lingjun, a giant in quantitative private equity.

February 20, 17:03 pm: The Shenzhen Stock Exchange announced that the Shenzhen Stock Exchange discovered during its transaction monitoring that within 42 seconds from 9:30:00 to 9:30:42, multiple securities accounts owned by Lingjun Investment automatically generated trading instructions through computer programs, placed a large number of orders in a short period of time, and sold a total of 1.372 billion yuan in Shenzhen Stock Exchange stocks. During this period, the Shenzhen Stock Exchange Component Index fell rapidly, affecting the normal trading order. The Shenzhen Stock Exchange decided to suspend trading in Lingjun’s account for three days and initiate a public censure record disciplinary procedure.

At around 17:40, the Shanghai Stock Exchange also announced that because Lingjun sold a large number of Shanghai stocks totaling 1.195 billion yuan in one minute, it had suspended trading for three days and issued a public censure record.

At 19:05, the Shanghai and Shenzhen Stock Exchanges respectively announced the smooth implementation of the quantitative trading reporting system. This is also the first time since the new regulations on programmed trading that the supervision has issued an announcement with "quantitative trading" as the clear subject. The two exchanges have the same caliber and have given characterization to quantitative trading: While quantitative trading helps provide liquidity to the market and promote price discovery, quantitative trading, especially high-frequency trading, also has problems such as strategic convergence and trading resonance at some points in time, increasing market volatility.

Subsequently, the exchange stated that it will continue to strengthen the monitoring and analysis of quantitative trading, especially high-frequency trading, with six major measures.

First, strictly implement the reporting system and clarify the access arrangements of “report first, trade later”;

The second is to strengthen the authorization management of quantitative trading prices and improve the differentiated charging mechanism;

The third is to improve the monitoring and control standards for abnormal transactions and strengthen the supervision of abnormal transactions and abnormal order cancellations;

The fourth is to strengthen the monitoring and regulation of leveraged quantitative products and strengthen the joint supervision of futures and spots.

The fifth is to further consolidate the customer management responsibilities of securities companies, improve the self-regulatory management cooperation mechanism with the Securities Industry Association and the Fund Industry Association, and strengthen the transaction supervision of quantitative private equity and other institutions, etc.

Sixth, the exchange will strengthen communication with the Hong Kong Stock Exchange, clarify the reporting arrangements for northbound investors in Shanghai-Hong Kong Stock Connect in accordance with the principle of consistency between domestic and foreign investors, and include quantitative transactions by northbound investors within the reporting scope.

A number of quantitative private equity firms have also launched self-certifications and clarifications. At around 21:24 in the evening, media reported that the quantitative giant Huanfang denied the liquidation of its products and stated that the company had never done any DMA leverage transactions.

In the evening, the recent product operation instructions and apologies of quantitative private equity companies such as World Frontier Assets, Xuanxin Assets, and Longqi Fund were also reported one after another. Most of the quantitative four times said that they would strengthen risk control constraints and reduce risk exposure.

In addition, a leading quantitative private equity reporter told a reporter from the Financial Associated Press that he "changed his strategy overnight". The initial plan is to change the trading frequency in some specific time periods to reduce the frequency of triggering transactions.

The third stage (0:00-8:00 on February 21) Lingjun, the punished institution, apologized late at night

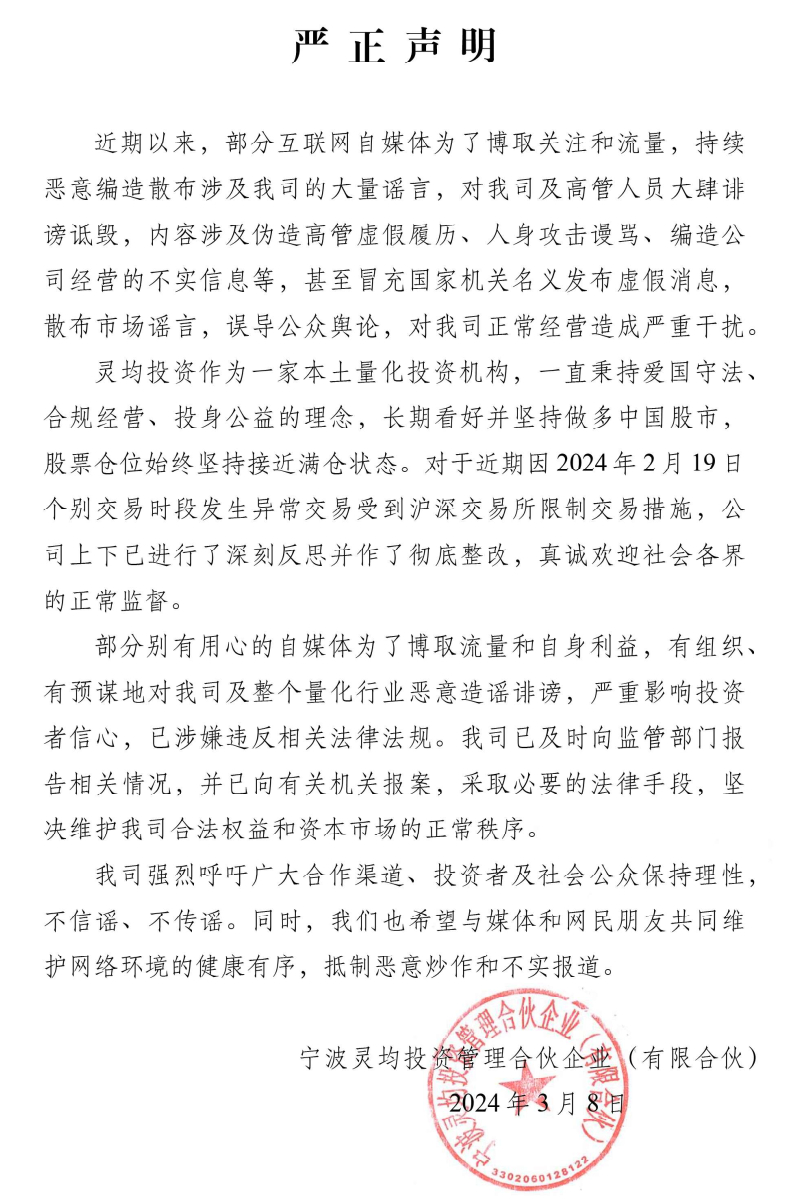

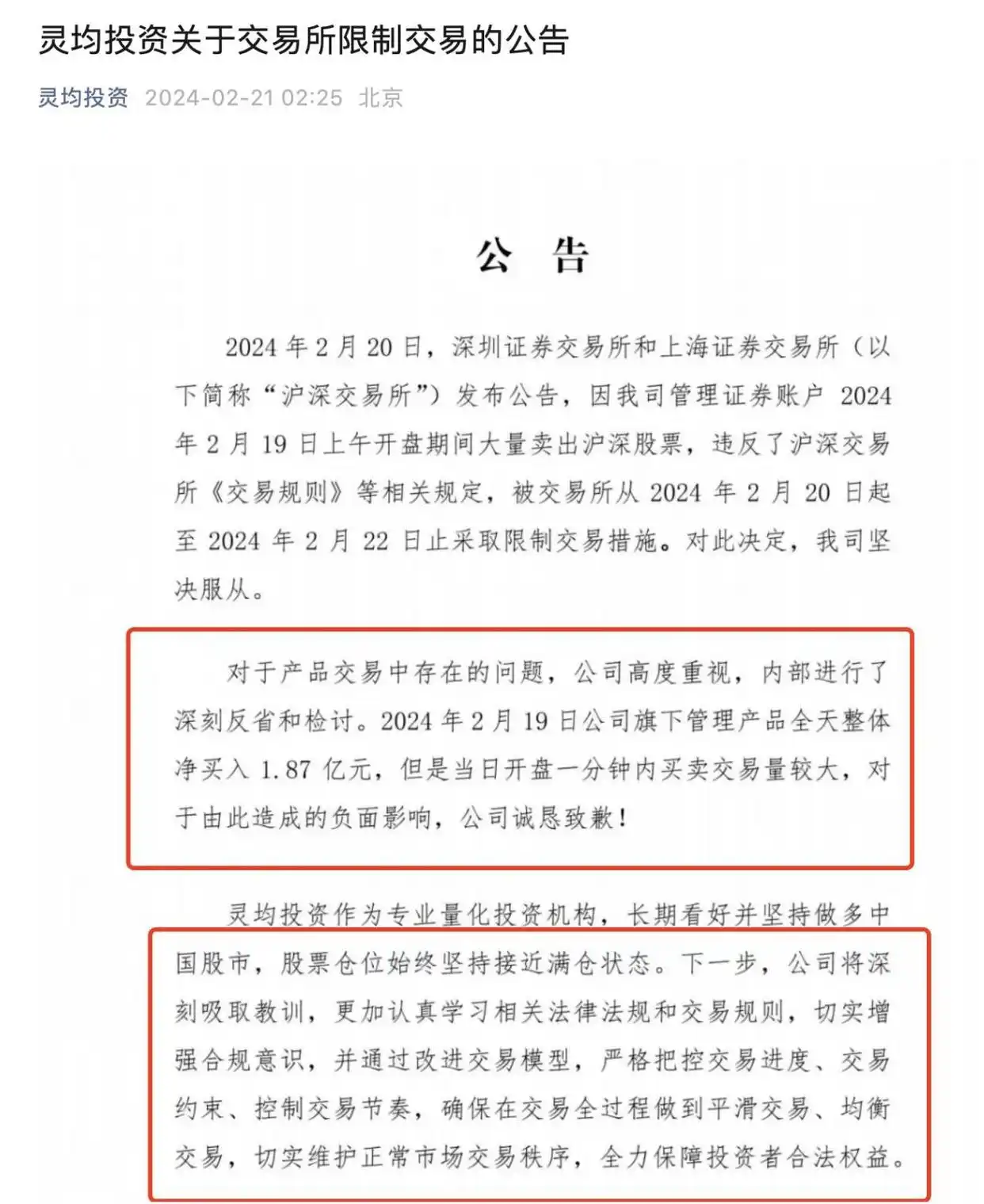

At 2:25 a.m. on February 21, Lingjun Investment issued an announcement on the exchange's trading restrictions, expressing "firm obedience", in-depth review, and apology to the investment.

Lingjun Investment stated in the announcement that the company will resolutely comply with the trading restrictions imposed by the Shanghai and Shenzhen Stock Exchanges. The company attaches great importance to the problems existing in product transactions and has conducted deep introspection and review internally.

The announcement also explained the transactions on the day of the penalty: On February 19, 2024, Lingjun’s management products had an overall net purchase of 187 million yuan throughout the day, but the trading volume was large within one minute of the opening of the day. The company sincerely apologizes for the negative impact caused.

The announcement also mentioned that Lingjun Investment, as a professional quantitative investment institution, is optimistic about and insists on being long in the Chinese stock market in the long term, and its stock positions have always been close to full. In the next step, the company will learn lessons deeply, study relevant laws, regulations and trading rules more seriously, effectively enhance compliance awareness, and by improving the trading model, strictly control the transaction progress, transaction constraints, and transaction rhythm to ensure smooth and balanced transactions throughout the transaction process, effectively maintain the normal market transaction order, and fully protect the legitimate rights and interests of investors.

The fourth stage (8:00-12:00 on February 21) The China Securities Regulatory Commission emphasizes that "one item will be matured and another item will be launched in the future" for quantitative supervision.

After the exchange took action, the China Securities Regulatory Commission also explained and emphasized quantitative supervision. According to multiple media reports, the Market Supervision Department of the China Securities Regulatory Commission stated that the China Securities Regulatory Commission has always paid attention to the development and supervision of quantitative trading. In recent years, it has successively promoted many tasks, including bringing quantitative trading into the scope of securities laws, establishing a data collection mechanism for leading quantitative institutions, strengthening quantitative trading monitoring and analysis, establishing a programmed transaction reporting system, strengthening private placement and securities lending supervision, etc.

The series of quantitative trading supervision measures introduced in the next stage will be matured one by one and launched one by one. We will fully strengthen communication with various investors in the market, grasp the pace and intensity of work, promote the standardized and healthy development of quantitative trading, and maintain the stable operation of the market.

“The focus of this quantitative trading supervision is on high-frequency trading.” The above-mentioned person further said that judging from international experience, overseas markets generally implement stricter supervision on quantitative trading, especially high-frequency trading, to prevent negative impacts on market order.

Germany, Japan, etc. have centralized regulations on quantitative trading in the form of written laws and implement access registration management for high-frequency traders. Germany stipulates the definition and characteristics of algorithmic trading and high-frequency trading, exchange fees, transaction monitoring indicators, system requirements, etc.; Japan has formulated and issued regulatory guidelines specifically for the supervision of high-frequency trading actors.

Markets such as the United States limit the speed at which high-frequency traders can obtain trading information, reduce information asymmetry, and ensure optimal execution of investor orders. At the same time, they clearly prohibit any market participant from participating in, specifying, or intending to conduct destructive trading behaviors, including "spoofing" and other market manipulation behaviors that have emerged with the rise of high-frequency trading.

Regarding the special reporting system for quantitative transactions currently implemented, supervision emphasizes that existing investors are currently "repaying all their dues" and incremental investors are "reporting first and then trading." Unreported investors cannot conduct programmed transactions, which is equivalent to allowing investors to "driving with a license" in the first place, providing institutional conditions for timely discovery of violations and real-time monitoring. (Reporter Yan Jun)

Trainee editor: Li Wenyu | Reviewer: Li Zhen | Supervisor: Wan Junwei