On February 20, according to the Shanghai and Shenzhen Stock Exchange websites, the quantitative transaction reporting system was smoothly implemented. In the next stage, the Shanghai and Shenzhen Stock Exchanges will take comprehensive measures from the institutional end, access end, trading end, information end, and institutional end to continue to strengthen the monitoring and analysis of quantitative transactions, especially high-frequency transactions, and include the quantitative transactions of northbound investors in the reporting scope in accordance with the principle of consistency between domestic and foreign investors.

The reporter learned that this is the first time that the Shanghai and Shenzhen Stock Exchanges have launched a series of regulatory measures focused on quantitative trading, clarifying the regulatory attitude and reflecting the determination of the regulatory authorities to strengthen the supervision of quantitative trading and maintain market stability. In the future, relevant quantitative trading supervision measures will be matured and launched, and communication with various investors in the market will be fully strengthened to grasp the pace and intensity of work, standardize quantitative trading, and maintain the stable operation of the market.

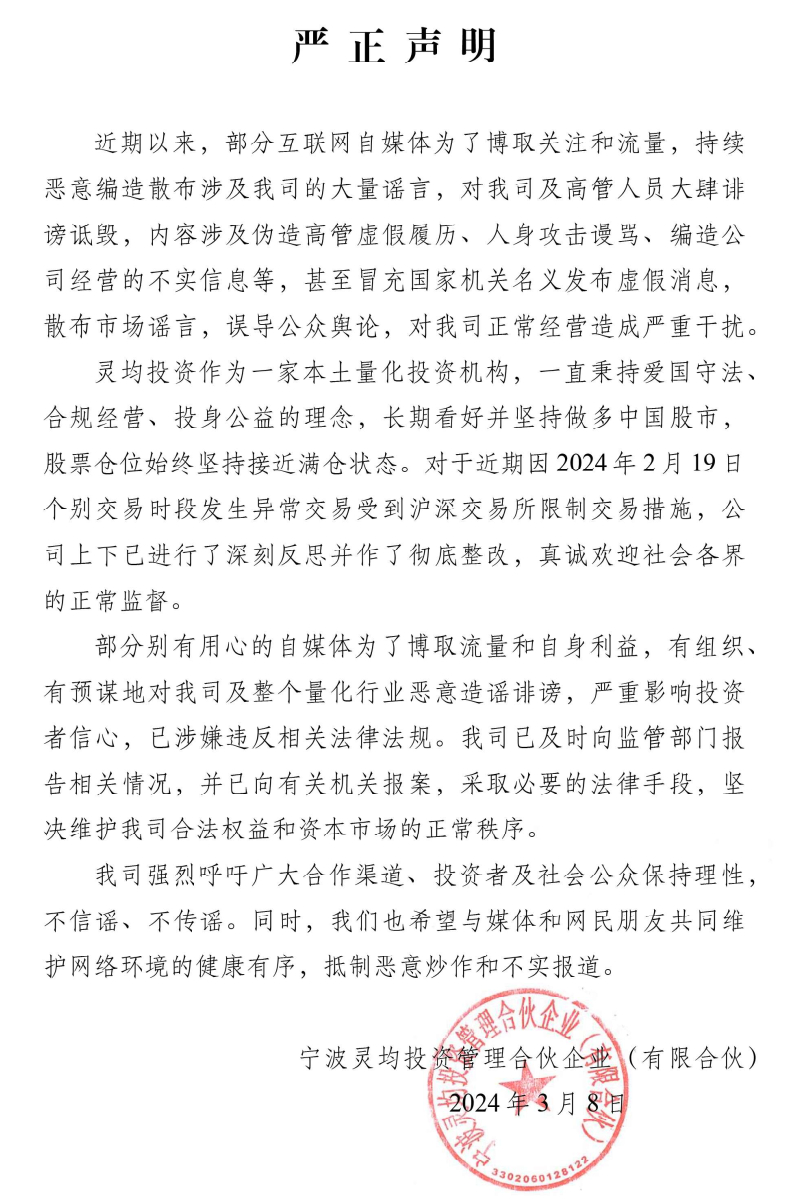

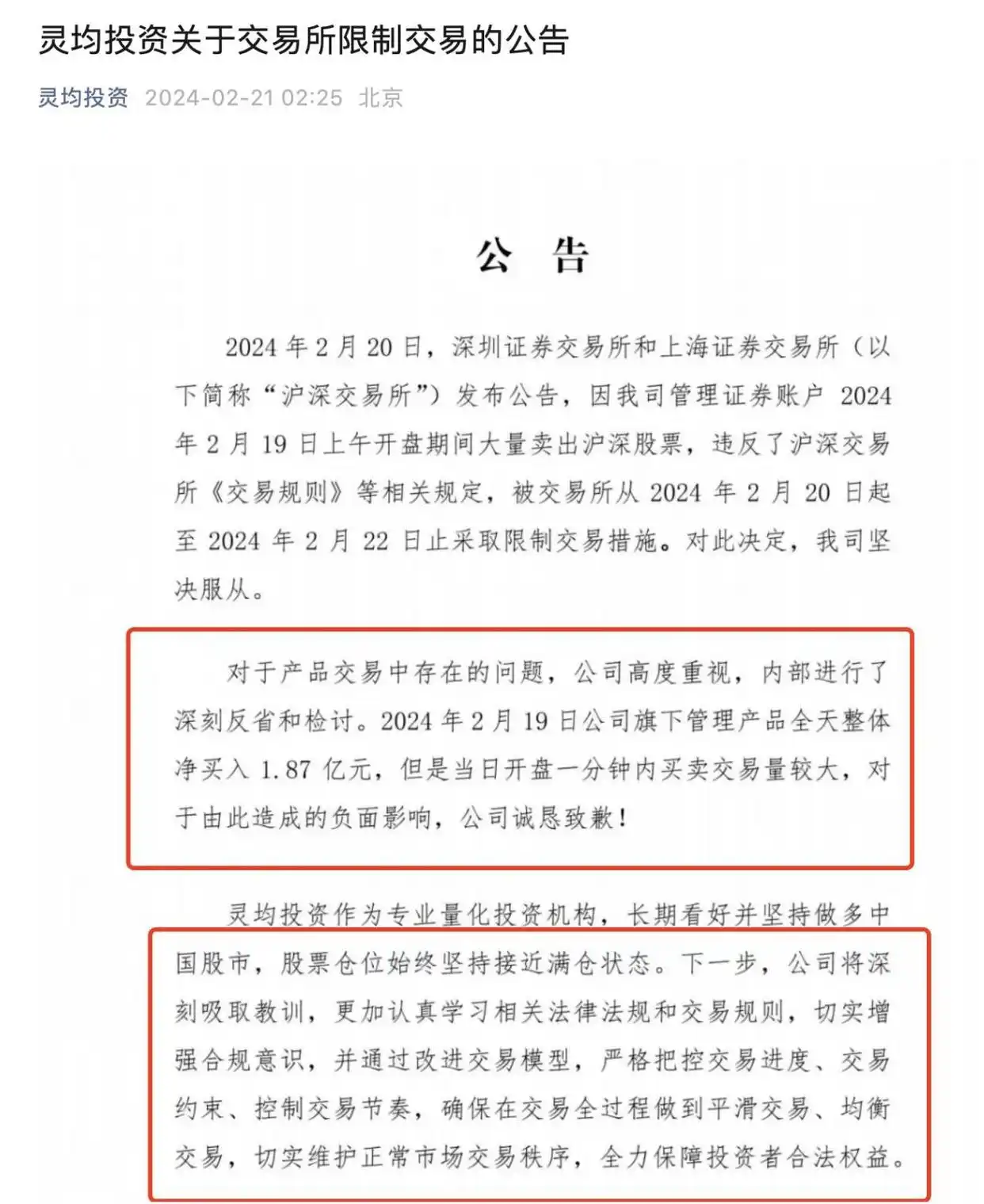

On that day, the Shanghai and Shenzhen Stock Exchanges issued a "penalty" for abnormal transactions of Ningbo Lingjun Investment Management Partnership (Limited Partnership) (hereinafter referred to as "Ningbo Lingjun"), restricted trading and initiated public condemnation procedures for Ningbo Lingjun. Industry insiders believe that supervision has "tears with thorns" and is intended to promote standardization and guide quantitative development. Regulatory authorities will respond quickly and strike hard at illegal activities that affect the normal trading order of the market and damage the legitimate rights and interests of investors.

A series of measures highlight investor-oriented

According to the website of the Shanghai and Shenzhen Stock Exchanges, quantitative trading regulatory measures include strictly implementing the reporting system and clarifying the access arrangements of "reporting first, trading later"; strengthening the authorization management of quantitative trading market conditions, and improving the differentiated charging mechanism; improving abnormal transaction monitoring and monitoring standards, strengthening the supervision of abnormal transactions and abnormal order cancellations; strengthening the monitoring and regulation of leveraged quantitative products, and strengthening futures and spot linkage supervision.

According to market analysts, the policies introduced this time are highly targeted and emphasize investor-oriented. For example, the requirement to "report first, then trade" will help to further accurately identify quantitative transactions; in view of the information advantages of quantitative transactions, clearly strengthen market authorization management; in view of recent quantitative transactions in small market capitalization stocks, clearly strengthen the monitoring and regulation of leveraged products to prevent stampedes in a short period of time. Including the self-regulatory management measures taken against Ningbo Lingjun this time, it is a reflection of the regulatory authorities’ strengthening supervision of abnormal trading behaviors.

"In the early stage, the regulatory authorities established a quantitative transaction reporting system. In accordance with the requirements, we have completed the reporting of existing customers, established a customer transaction monitoring system, and organized and mobilized relevant customers to report." A relevant person from Huatai Securities said that in the future, the company will continue to dynamically follow up on new additions, changes, etc., strictly implement the reporting system, and strengthen the detection of abnormal trading behavior.

The Shanghai and Shenzhen Stock Exchanges have also proposed specific measures from the institutional side, including further consolidating the customer management responsibilities of securities companies, improving the self-regulatory management cooperation mechanism with the Securities Association and the Fund Industry Association, and strengthening the transaction supervision of quantitative private equity and other institutions; strengthening communication with the Hong Kong Stock Exchange, in accordance with the principle of consistency between domestic and foreign capital, clarifying the reporting arrangements for northbound investors in the Shanghai-Shenzhen-Hong Kong Stock Connect, and including quantitative transactions by northbound investors within the reporting scope.

He Wenqi, chairman of Shenzhen Chengqi, said that the measures introduced this time will help reduce the impact of illegal quantitative transactions on the market and maintain the stability and fairness of transactions. The quantitative trading reporting system has been implemented for nearly half a year. This quantitative trading regulatory measure emphasizes the supervision of frequent orders and withdrawals, strengthens the monitoring of leveraged products, and clarifies the principles of northbound quantitative trading reporting, releasing a signal for supervision to further standardize quantitative trading.

The Shanghai and Shenzhen Stock Exchanges also stated that in the next step, they will adhere to the investor-oriented approach, take the maintenance of fairness as the starting point and end point of their work, learn from international regulatory practices, seek advantages and avoid disadvantages, and establish and improve quantitative trading regulatory arrangements. For abnormal transactions that affect market order, the Shanghai and Shenzhen Stock Exchanges will resolutely take self-regulatory management measures, and those suspected of violating laws and regulations and serious circumstances will be reported to the China Securities Regulatory Commission for investigation and punishment.

Mature one, launch one

For the first time, the Shanghai and Shenzhen Stock Exchanges have launched a policy "combination punch" from the institutional end, access end, trading end, information end, institutional end, etc. to further strengthen the pertinence and accuracy of quantitative trading supervision.

A relevant person from the Market Supervision Department of the China Securities Regulatory Commission told reporters that the China Securities Regulatory Commission has always paid attention to the development and supervision of quantitative trading. In recent years, it has successively promoted many tasks, including bringing quantitative trading into the scope of securities laws, establishing a data collection mechanism for leading quantitative institutions, strengthening quantitative trading monitoring and analysis, establishing a programmed transaction reporting system, strengthening private placement and securities lending supervision, etc. The "combination" of quantitative trading supervision launched this time is strong, strengthening supervision from multiple dimensions, and basically covering the main aspects of quantitative trading business operations.

"The series of quantitative trading supervision measures introduced in the next stage will be mature one by one and launched one by one, and we will fully strengthen communication with various investors in the market, grasp the pace and intensity of work, promote the standardized and healthy development of quantitative trading, and maintain the stable operation of the market." The above-mentioned person said.

Relevant people from Huatai Securities said that the relevant regulatory measures this time proposed a series of arrangements from various aspects such as access reporting mechanism, regulatory coverage, trading behavior and supporting systems, focusing on the programmed transaction reporting management system that has been implemented in the early stage, reflecting the "thorny" supervision, and further eliminating regulatory gaps.

Quantitative trading supervision emphasizes seeking advantages and avoiding disadvantages

There is currently a lot of market discussion about quantitative regulation. Many opinions believe that quantitative trading started late, but developed rapidly and had a greater impact on the market.

"The impact of quantitative trading on the market must be viewed dialectically." Relevant people from the Shanghai and Shenzhen exchanges said that on the one hand, quantitative trading is usually operated with full or high positions, which provides more liquidity to the market and helps promote price discovery. On the other hand, quantitative trading, especially high-frequency trading, has characteristics such as fast transaction speed, strong processing power, and the use of artificial intelligence. It has strong technical advantages, information advantages, and trading advantages over the majority of investors. In addition, some micro-cap trading behaviors have convergence in strategies, transactions, and even trading hours, which further amplifies the fluctuations of individual stocks, thereby causing market resonance.

A relevant person from the Market Supervision Department of the China Securities Regulatory Commission told a reporter from the Shanghai Stock Exchange that the Shanghai and Shenzhen Stock Exchanges have comprehensively implemented policies to supervise quantitative trading, not to kill quantitative trading with one stick, nor to ban quantitative trading. Instead, during the daily supervision process, it has been found that there are more quantitative transactions, the frequency of transactions, the frequency of placing and canceling orders is too high, there are phenomena such as excessive use of information advantages, exacerbating information asymmetry, etc., and the unfairness brought to the market has become increasingly obvious.

"Considering the current market situation of 200 million investors, and the risk of increasing market volatility in quantitative high-frequency trading under a specific market environment, it is necessary to take advantage of the situation to promote its standardized development and make it more investor-oriented." said the person above.

Focus on high-frequency trading, in line with international practice

A relevant person from the Market Supervision Department of the China Securities Regulatory Commission said that the focus of this quantitative trading supervision is on high-frequency trading. Judging from international experience, overseas markets generally implement stricter supervision on quantitative transactions, especially high-frequency transactions, to prevent negative impacts on market order.

For example, Germany, Japan, etc. have centralized regulations on quantitative trading in the form of written laws and implement access registration management for high-frequency traders. Germany stipulates the definition and characteristics of algorithmic trading and high-frequency trading, exchange fees, transaction monitoring indicators, system requirements, etc.; Japan has formulated and issued regulatory guidelines specifically for the supervision of high-frequency trading actors.

Markets such as the United States limit the speed at which high-frequency traders can obtain trading information, reduce information asymmetry, and ensure optimal execution of investor orders. At the same time, they clearly prohibit any market participant from participating in, specifying, or intending to conduct destructive trading behaviors, including "spoofing" and other market manipulation behaviors that have emerged with the rise of high-frequency trading.

Many market participants have also reported that the quantitative transaction reporting system established in the early stage imposes additional reporting requirements on high-frequency transactions, so as not to affect the security of the exchange system and normal trading order. This is also in line with internationally accepted practices.

The quantitative transaction reporting system was implemented smoothly

On September 1 last year, the Shanghai and Shenzhen Stock Exchanges issued the "Notice on Matters Concerning the Reporting of Stock Programmed Trading" and the "Notice on Matters Concerning Strengthening the Management of Programmed Trading", establishing a special reporting system and corresponding regulatory arrangements for quantitative trading, which will be officially implemented on October 9, 2023. At present, the above-mentioned system has been implemented smoothly.

The reporter learned from the Market Supervision Department of the China Securities Regulatory Commission that at present, existing investors have achieved "repayment of all dues", and incremental investors "report first, then trade". The quality of reports from all parties generally meets the requirements, laying the foundation for further strengthening and improving quantitative trading supervision.

It is reported that the content of the quantitative trading report is very detailed, including basic account information, account fund information, transaction information, trading software information and other major categories. There are also specific requirements under the major categories. For example, the account fund information requires filling in the account fund size, fund source, and source proportion. For leveraged funds, the leveraged fund source and leverage ratio need to be filled in. The transaction information requires filling in the transaction type, whether it is a quantitative transaction, the main strategy type and overview, auxiliary strategies and overview, futures market account name and code, trading order execution method and overview, the highest account declaration rate, the highest number of declarations in a single day, etc.

A relevant person from the Market Supervision Department of the China Securities Regulatory Commission said that unreported investors cannot conduct programmed transactions, which is equivalent to allowing investors to "driving with a license" in the first place, providing institutional conditions for timely discovery of violations and real-time monitoring.

Editor: Tao Jiyan | Reviewer: Li Zhen | Supervisor: Wan Junwei