Bloomberg reporter Mark Gurman insisted on April 8 that Apple’s first foldable screen iPhone will still be released in September as planned.

Just the day before, Nikkei Asia reported another picture: the engineering verification and testing phase encountered more complex problems than expected. The hinge yield rate was only 30% to 65%, and the screen creases could not be eliminated. In the worst case, mass production may be delayed for several months.

The tug-of-war between the two voices just exposes the real dilemma of Apple’s folding screen – Huawei Mate

The era when suppliers worked hard to squeeze into Apple's supply chain is gone forever. What replaced it was a collective rational defense based on "Ophelia fear." Working for Apple has gone from being a ticket to the top spot in the A-share market to a toxic asset that may return to zero overnight.

Looking deeper, Apple itself is in structural trouble. It is still a reluctant monarch of the global supply chain and a sandwich layer in the geopolitical game. When security and politics replace pure market logic and become the primary variable in supply chain decisions, Apple's control techniques that rely on technological leadership and business reputation are experiencing unprecedented backlash. In this sense, Apple's toxicity does not only refer to its strong treatment of suppliers, but also to a distorted macro environment – an environment in which commercial rationality gives way to political narratives, and Apple is both a pressurer and a victim.

1. From the myth of wealth creation to the closed loop of fear

To understand Apple's current predicament, one must look back at the dramatic turnaround in its supply chain relationships over the past fifteen years.

It was an era of wealth creation belonging to the fruit chain. Wang Laichun, the founder of Luxshare Precision, once said that flying with the phoenix must be a handsome bird. In order to get orders from Apple, Luxshare pursues a close-to-customer strategy. Foxconn will build factories wherever they go. In 2017, when Inventec was struggling with the yield rate of AirPods, Luxshare not only overcame the problem, but also shortened the product delivery cycle from five to six weeks to one to three days, winning the exclusive OEM right in one fell swoop.

This faith-based collaboration has paid off handsomely. Luxshare Precision’s revenue was less than 10 billion yuan when it went public in 2010, but it had soared to 268.7 billion yuan in 2024. Wang Laichun also ranked the fourth richest female in China with a net worth of 85.5 billion yuan in March 2026. The same story happened to Goertek and Lens Technology. At that time, entering the fruit chain was synonymous with technical strength and global reputation, and was a proven high-speed upward path.

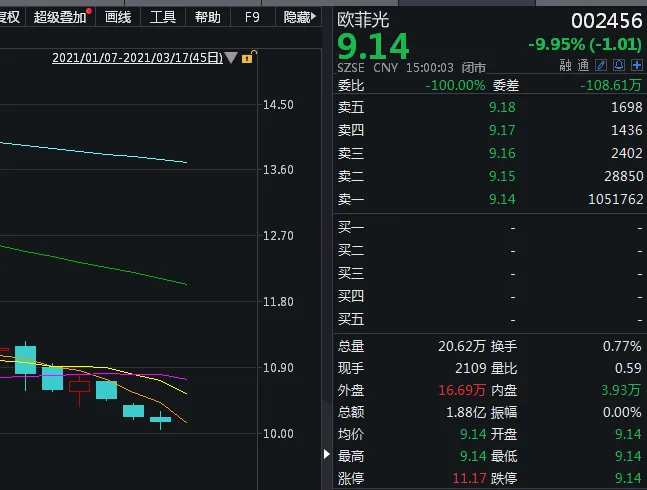

The turning point began in March 2021. Apple suddenly kicked OFILM out of the supply chain. The superficial reason was supply chain adjustment, but the industry generally believes that the geopolitical background of being included in the U.S. Entity List was the key pressure for Apple to make the decision to cut. This company that has been OEMing for Apple for many years collapsed instantly: its revenue in 2021 was cut by 52.75% year-on-year, with a net loss of 2.665 billion yuan, its stock price plummeted 70%, and its market value evaporated by more than 30 billion yuan. What's even more fatal is that some of the special equipment and process standards customized for Apple are difficult to directly reuse in Huawei and Xiaomi's product lines, resulting in low production capacity utilization during the conversion period and a sharp increase in asset impairment pressure.

However, Ou Feiguang did not die as expected. After the return of the Huawei Mate 60 series in 2023, OFILM won most of the orders for camera modules; in 2025, it will also exclusively supply camera modules for Xiaomi AI glasses and SU7 Ultra. This abandoned fruit chain company, once abandoned by Apple, relied on orders from Hualian and Milian to urgently add new production lines at its Nanchang factory, achieving a dramatic turnaround.

But the price of this renewal is that OFILM has shifted from being deeply bound to Apple to equally deeply dependent on Huawei and Xiaomi. In 2024, the sales revenue share of its top five customers will increase from 69.54% to 77.35%. OFILM's case has thus become a preview of suppliers' worst fears: no matter which chain they switch to, over-reliance on a single customer's high-investment model is a high-risk gamble.

If OFILM's resurrection had given the market a glimmer of luck, then the experience of Wingtech Technology had completely extinguished this glimmer of hope. In 2021, Wingtech acquired OFILM's original Apple camera business for 2.42 billion yuan, intending to enter the fruit chain. After difficult compliance reforms and production line upgrades, its Kunming factory will finally start manufacturing MacBooks for Apple in 2023. However, in December 2024, Wingtech was included in the entity list by the U.S. Department of Commerce, and all efforts came to nothing in an instant. In 2025, Wingtech was forced to sell all of its foundry business to Luxshare Precision for about 4.4 billion yuan.

Apple’s sandwich layer dilemma is highlighted here. OFILM was abandoned due to Apple's hedging choice under geopolitical pressure; Wingtech was blocked due to external sanctions beyond its control. Apple is both the enforcer of pressure and the passive party unable to protect its partners. This dual role allows suppliers to see clearly the fact that when cooperating with Apple, they not only have to face its commercial strength, but also bear non-market risks that it cannot shield. No matter how good the technology is, it may be abandoned by Apple for non-commercial reasons; compliance operations may also be sanctioned by external forces beyond Apple's control.

The two cases are superimposed to form a complete closed loop of fear – it declares to all Chinese suppliers that investing in dedicated assets and excessive technology investment for Apple is a high-risk gamble with an uncontrollable outcome. The risk-benefit formula of Fruit Chain Certification, which once symbolized glory and wealth, has been completely rewritten.

2. From faith-based cooperation to risk pricing

Fear directly leads to fundamental changes in behavioral patterns.

In the past, the belief-based cooperation that took the initiative to advance regardless of costs has now been replaced by a calculated and defense-first risk consideration. This shift is essentially about pricing non-market risks.

Leading suppliers are taking the initiative to reduce their dependence on Apple. Luxshare Precision's revenue from Apple has dropped from approximately 75% in 2022 to 64.3% in the first half of 2025. Its strategic focus has clearly shifted: through the acquisition of Germany's Leoni wiring harness business and Wingtech's ODM department, it will aggressively enter the automotive electronics and Android mobile phone camps. In the first nine months of 2025, Luxshare's automotive business revenue surged 155% year-on-year to 23.7 billion yuan. Lens Technology is also reducing Apple's sales proportion. Its new energy vehicle business revenue will increase by 39.47% in 2023. Its customer list includes Tesla, BYD, Ideal, Weilai, etc. Resources are flowing from the uncertain Apple folding screen project to a track with more certainty and policy support.

Investment strategies have also shifted from specialized to general purpose.

In the past, suppliers would spend huge sums of money to build dedicated production lines for specific Apple products. For example, in 2021, Luxshare invested 11 billion yuan in Kunshan to build a super factory equivalent to the size of 40 football fields in order to compete for iPhone orders. Now, facing Apple’s folding screen project, the first principle for suppliers is to avoid repeating the mistakes of OFILM. They refuse to build production lines that only serve Apple, and require that the production lines must be compatible with the standards of customers such as Huawei and Xiaomi to prevent assets from being scrapped if orders change due to commercial or non-commercial reasons. They even began to require Apple to prepay for investment in production lines, subverting the traditional investment first and amortization after success model. This is equivalent to requiring Apple to pay a deposit for potential political cut-off risks.

Technology interactions similarly shift from transparency to retention.

"Nikkei Asia" reported an intriguing detail: Apple purchased domestically produced folding screens for disassembly, but was still unable to solve the crease problem. This is most likely a technology retention strategy. Take Huawei Mate X6 as an example. Its hinge patents have exceeded 2,850, and the crease depth is controlled to 0.08 mm, which is difficult to distinguish with the naked eye. China's supply chain already has the ability to achieve crease-free production, but in the face of Apple, they have the incentive to show that the technology is not feasible in the game.

The most fundamental changes occur at the negotiating table. In the past, suppliers accepted Apple's harsh terms in exchange for admission, including 90 to 120-day accounting periods, 5% annual price reduction requirements, and technology exclusivity. Now, they are beginning to demand a risk premium from OFILM: technical protection clauses signed in advance to prevent technology from being transferred to Indian or Vietnamese suppliers; a clear exit compensation mechanism to prevent being kicked out without reason or for political reasons; and a shorter accounting period. In short, the shift from cooperation first and then discussing money has become to insuring political risks first and then discussing business cooperation. If Apple does not agree, suppliers would rather give up the order than make unguaranteed excess investment. The annual reduction mechanism that Apple used to control costs and the threat of second suppliers to control technology are failing in the face of this new algorithm.