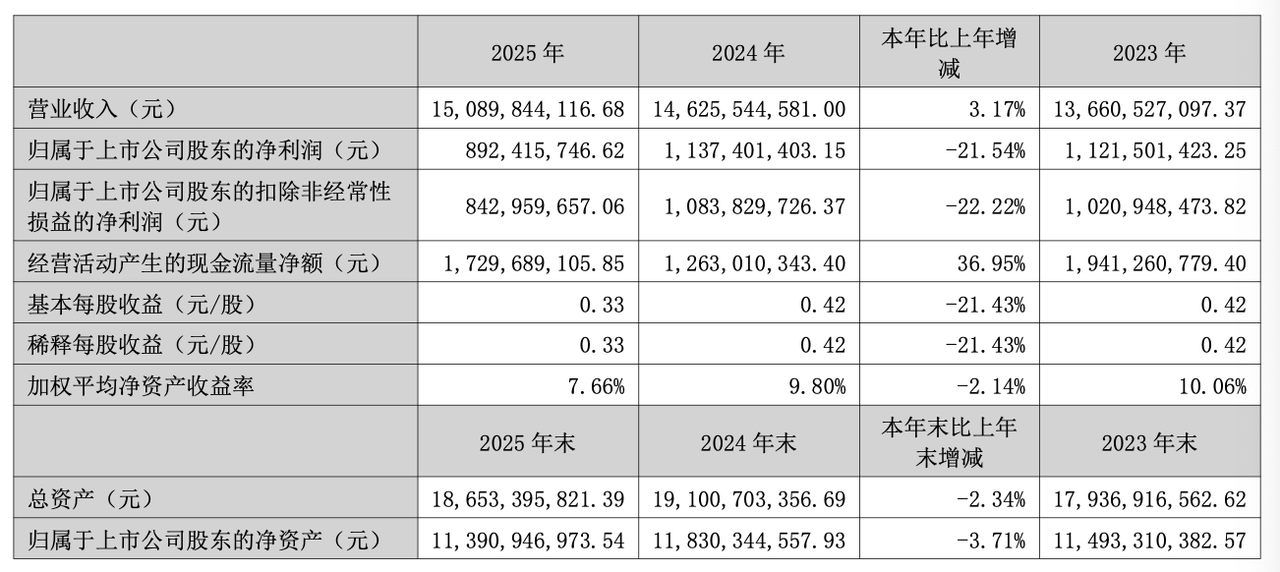

In 2025, Semir Apparel handed over an annual report card that seemed stable at first glance: revenue remained at 15 billion yuan, an increase of 3.17 percentage points.

In a year when overall consumption is under pressure, it is not easy to maintain scale.

But if you look away from revenue, the real changes in this company occur on the other side. In addition to low single-digit growth in revenue, net profit attributable to the parent company, earnings per share, total assets, and net assets attributable to shareholders of listed companies all recorded negative growth.

Behind the increase in revenue but not profit is: franchise stores continue to have net outflows, direct sales revenue has increased by more than 30% year-on-year, and sales expense rates have increased. The income is still there, but the price that needs to be paid in exchange for this income is no longer the same.

The company is using higher costs to maintain what it built two decades ago.

How do the neighbors of Baleno survive today?

Semir's early success was actually not that complicated.

In 1996, Qiu Guanghe started in Wenzhou, using the franchise chain model. Most of the store's rent, decoration, and inventory are borne by franchisees. The headquarters charges brand fees and product price differences, leveraging an extremely wide channel network with extremely low own assets.

The elegance of this model is that expansion requires almost no additional capital, the risk is spread among thousands of franchisees, and the headquarters reaps the bargaining power of scale.

There is still a gap in the low-tier market. User acquisition depends on store density. Opening a new store means adding a new batch of customers. The logic was almost impeccable at first.

That is also a very typical dividend of the times. There is room for channels, consumption is growing, and competition is not yet too fierce. "Opening a store" is almost equal to "having customers", and expansion is almost equal to "growth".

At first it was Semir’s casual wear. In its early days, Semir's positioning of "comfortable experience and quality life" attracted many young people in the face of the then "street fighters" Baleno and Giordano.

But by 2010, the space for casual wear began to narrow, and competition turned from incremental to stock. Qiu Guanghe’s children’s clothing brand Balabala began to take over the “big stick” of growth.

Qiu Guanghe's eyes were very vicious. As early as 2002, he saw a gap in the children's clothing market, advocated professionalism, fashion, and vitality, and aimed at well-off families in middle-income families.

At that time, China's children's clothing market was extremely low-concentration, with messy products and a brand vacuum. Balabala uses chain franchising and uses similar channel genes as casual clothing to rapidly replicate and expand.

China's children's consumer market began to expand rapidly in the mid-2010s. At that time, China was experiencing the peak of newborns. The two-child policy coupled with consumption upgrades meant that post-80s parents who were willing to spend money on their children needed branded children's clothing.

Semir Clothing has taken another "hitchhike".

The shift to children's clothing business is particularly important for Semir Apparel. It is more like a structural correction.

Semir Apparel's core business, casual apparel, is essentially a typical cyclical business: affected by fashion, with obvious fluctuations and strong substitution. Such companies are not scarce in the capital market, and it is difficult to obtain stable valuation expectations.

Barabara changed that. Children's clothing consumption is closer to immediate needs, with higher repurchase frequency and longer life cycle. It provides Semir with a more stable source of income and allows the company to move from an "apparel company" to a "consumer products company."

In 2011, Semir Apparel was listed on the Shenzhen Stock Exchange. As a core asset, Balabala is a solid backing for its successful listing. From 2015 to 2019, Semir Apparel’s operating income grew at double digits.

The environment begins to change

2020 will be a turning point for Semir Apparel’s performance.

That year, Semir's apparel operating revenue was 15.2 billion yuan, a year-on-year decrease of 21.37%, and its net profit was 806 million yuan, a year-on-year decrease of 48%. The net profit was almost halved.

Change doesn't happen suddenly.

The franchise system is an advantage in the expansion stage, but when the market enters stock competition, this system begins to expose its other side: difficult management, uneven efficiency, and weak brand execution.

For a brand trying to move up, this is a real hurdle.

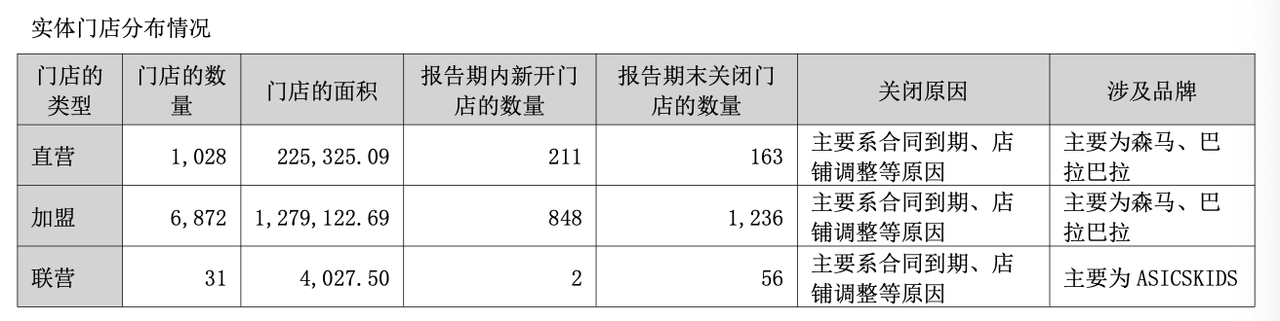

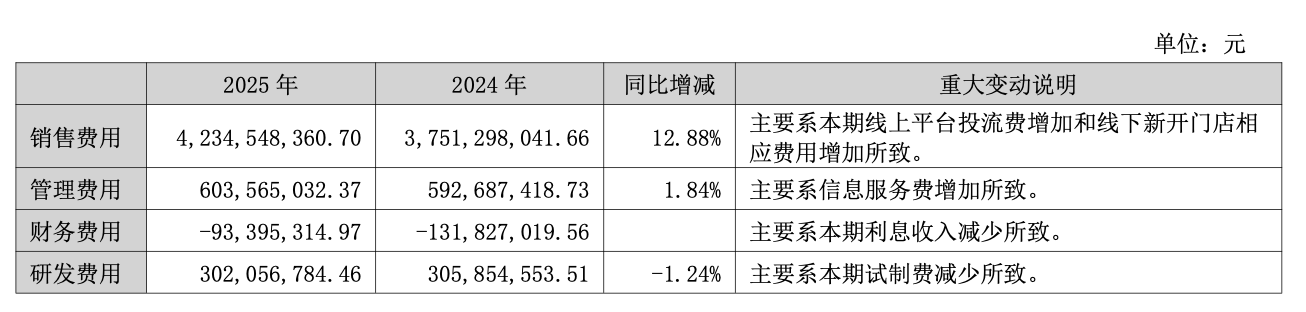

So Semir began to shrink franchises and expand direct sales. In 2025, the company closed 163 directly operated stores and opened 211 new ones; it closed 1,236 franchise stores and opened 848 new ones.

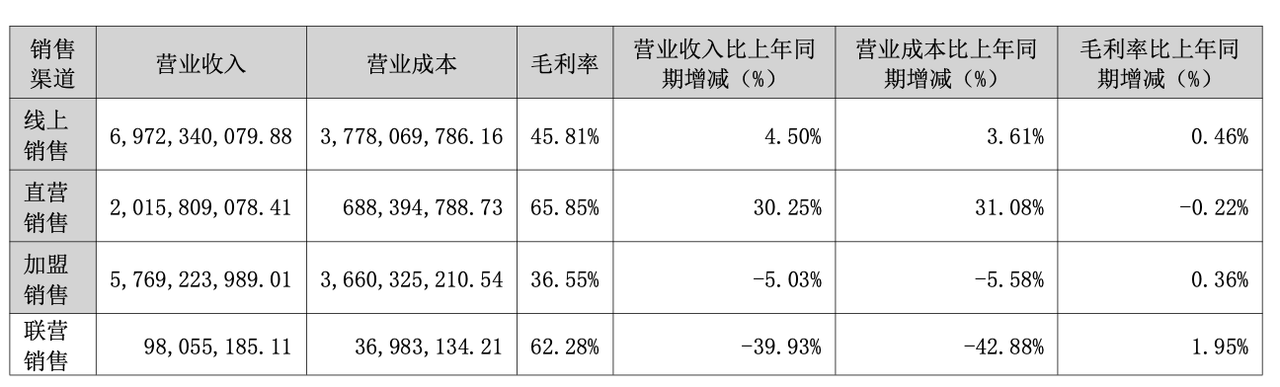

During the period, the revenue growth rate brought by the direct operation model reached 30.25%, the revenue brought by franchise stores decreased by more than 5 percentage points compared with the previous year, and online sales revenue increased by 4.50%.

Increasing direct sales gives Semir greater control over channels and makes brand execution more unified.

But there's a trade-off: It's a heavier set of business.

The essence of franchising is to transfer fixed costs such as rent and labor. Once it changes to direct operation, store rent, shopping guide salary, and inventory risk will all fall back on the company.

The larger the scale, the more obvious this weight becomes.

At the same time, traffic is becoming more expensive.

In the past, stores were the entrance to traffic. Things are different now. Consumers are spending more and more time on their mobile phones, on short video platforms, and on various content. The store is still there, but it is no longer an entrance, it is just a conversion scene.

Traffic on social/e-commerce platforms is becoming more and more expensive, and it has become a continuously rising item in sales expenses.

In 2025, Semir Clothing's sales expenses will reach 4.235 billion, a year-on-year increase of 12.88%, mainly due to the increase in online platform shipping fees and the corresponding increase in expenses for newly opened offline stores in this period.

The increase in traffic costs is actually a change in the form of channel costs. In the past, it was rent, but now it is traffic price. It’s just that the latter is more uncontrollable and unpredictable.

Children's clothing, a trump card, is also a focus point

If only the cost structure is changing, it can be said to be a "transformation pain" and it is an acceptable transition.

But there's another thing that makes the problem even harder to deal with: dependence on children's clothing.

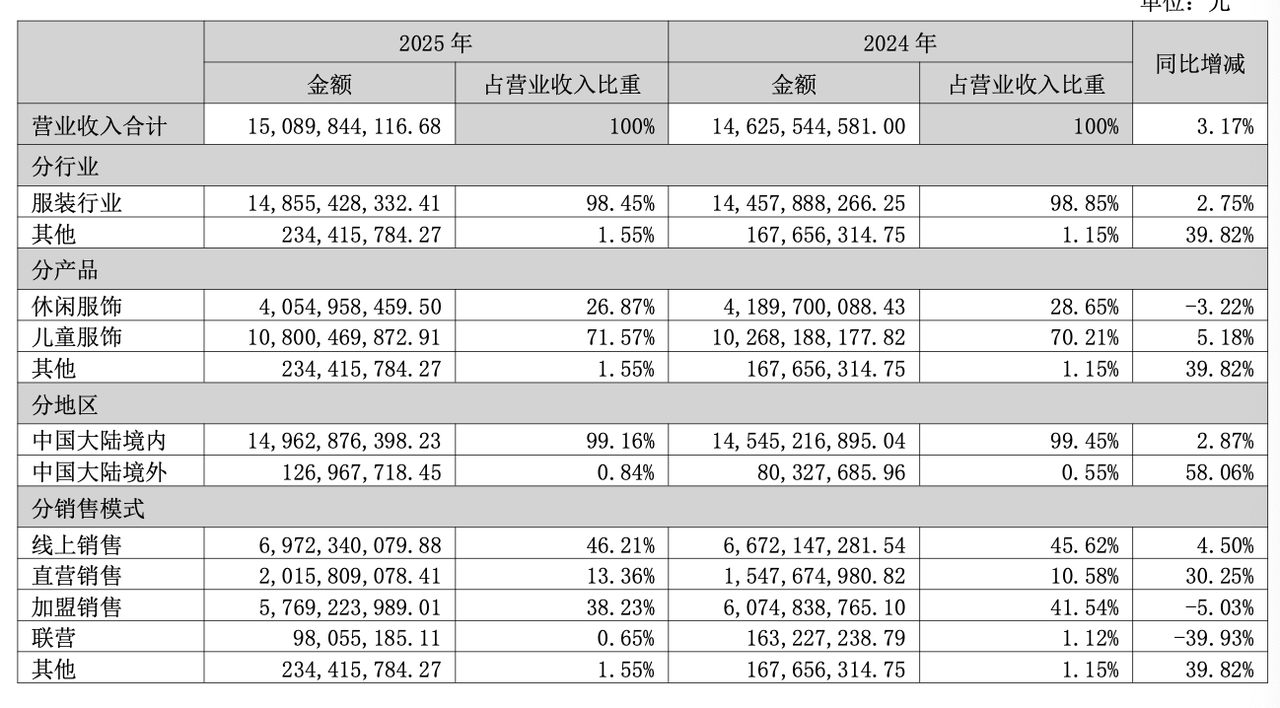

In 2025, Semir's children's clothing revenue will be 10.8 billion yuan, accounting for more than 71% of the overall revenue, and its proportion of total revenue has quietly increased by 1.36 percentage points.

Coupled with the two authorized businesses of ASICS Kids and PUMA Kids, the entire group's business focus is almost entirely concentrated on children's consumption.

From a strategic logic point of view, this is a deliberate choice.

Balabala has achieved the largest scale in the domestic children's clothing market, and its brand recognition and channel coverage have reached a certain level. The judgment itself of concentrating resources on this strongest line and cultivating it deeply rather than spreading it out makes sense.

But this also means that all external pressures will be concentrated on children’s consumption. There is no other business curve to cushion, no other categories to hedge costs.

The demand for children's clothing market has gone through two stages in the past ten years: first, the incremental period driven by demographic dividend, and then the quality improvement driven by consumption upgrade. Balabala has experienced both stages.

But now is the third stage.

Declining birth rates, intensified consumption stratification, and intensified competition among domestic and foreign brands are not structural trends that a company can fight against. As a result, those problems that originally belonged to "industry changes" will directly become Semir's problems.

Balabala general manager Will said in an interview that the declining birth rate is actually a reshuffle in the industry, and "the next competitive focus of children's clothing is whether it can truly understand the parent-child relationship in this era."

Behind this is Balabala's ability to seize the changes in the children's clothing market. Children's clothing is no longer just for children's consumption, but a part of family relationships. It began to introduce narratives of companionship, growth and interaction into its products and marketing, trying to embed itself in family relationships.

But this understanding is still superficial.

It is more like inheriting a set of mainstream consensus that has been formed and covering different families and different scenarios as much as possible, rather than proactively proposing a more distinct value position. The result is that the expression is broad enough, but not deep enough; the coverage is broad enough, but it is difficult to form a stronger identity.

The lack of a clear position is bound to make it difficult to establish stronger recognition and premium. This also allows a variable that could have become a "new moat" to remain in the "marketing language" stage for the time being.

It's changing its way of life, but it hasn't fully adapted yet

Judging from its actions, Semir is not a company that is blind to changes.

Shrinking franchising and expanding direct sales is to solve the problem of channel control; increasing sales investment is responding to the migration of traffic entrances; deepening the focus on children's clothing is concentrating resources in the most advantageous direction.

Semir has also invested in mid- to high-end brands.

Semir Apparel's cooperative brands include Jason Wu and SHUKU, and it has established joint ventures with the two brands respectively. In addition, in addition to Asics Kids and Puma Kids, Semir Clothing also has a Nordic fashion lifestyle brand Marc O' Polo.

These judgments, taken individually, all make sense.

But there is a question that, taken together, remains unanswered: If it no longer relies on low-cost expansion, what exactly is the core advantage of this business?

This is not a question that can be answered with a strategy document, it needs to be proven with real business results.

Is it product power? Then there needs to be visible investment and differentiation in design, research and development, and fabrics, so that consumers can actively choose Balabala at the same price, not because "the store is close to home."

Is it brand power? Then it is necessary to achieve a certain level of emotional resonance and mental occupation, so that "buying clothes for children" becomes a habitual cognition, rather than a choice that can be replaced at any time.

Is it a user relationship? Then we need a consumer operation system that can continue to accumulate and be activated repeatedly, so that every parent who buys Balabala will have a higher repurchase rate and stronger brand stickiness.

Semir is doing all three of these things. But to what extent it has been achieved and how many real barriers to competition it has created are still unclear.

Before this answer appears, all it can do is maintain its current scale and position at a higher cost. It's a working business, but not an easy one.

Although it has not entered a real crisis, Semir Apparel is getting further and further away from that period of easier "counting money". Not into a real crisis, but it's moving further and further away from that easier period.