On the 28th, the U.S. Federal Deposit Insurance Corporation (FDIC) issued new regulations clarifying that banks can carry out crypto-asset-related businesses without prior approval. This policy shift not only paves the way for U.S. banks to participate in the crypto market, but also triggers ripple effects around the world.

On March 28, 2025, the U.S. Federal Deposit Insurance Corporation (FDIC) issued the "Procedural Guidelines for Banks to Engage in Crypto-Related Activities" (FIL-7-2025), clarifying that FDIC-supervised banks can carry out crypto-asset-related businesses without prior approval (FDIC Clarifies Process for Banks to Engage in Crypto-Related Activities | FDIC.gov). This new regulation revokes the notification requirement for 2022 (FIL-16-2022), marking a major change in US regulatory attitudes towards banks’ involvement in the crypto field.

The following will provide an in-depth analysis of the impact of this guidance on the cryptocurrency market from four dimensions: regulatory impact, market confidence, bank participation, and changes in trading volume.

(Note: Based on the summary and analysis of public information on the Internet, reference sources are attached to the article and do not constitute investment advice. Please abide by the law)

1. Brief introduction to FDIC and FIL-16-2022

The FDIC is an important banking regulatory agency in the United States. It is responsible for the depositor protection of American banks and the resolution of bankrupt banks, and eliminates the risk of runs through the deposit insurance system. For example, when Silicon Valley Bank went bankrupt in 2023, the FDIC completed the repayment of insured deposits within 48 hours and recovered funds through asset auctions.

In order to avoid bank bankruptcy, the FDIC pays special attention to the review and supervision of financial indicators such as bank capital adequacy, liquidity, compliance, risk management, and risk ratings.

The revoked FIL-16-2022 is a regulatory requirement introduced in 2022 to deal with the risks of cryptocurrency. The core is that if banks want to engage in cryptocurrency-related business, they need to apply for approval in advance.

2. U.S. regulatory deregulation and global linkage 2.1. Local regulatory changes in the United States

The FDIC’s new guidelines remove the requirement for banks to apply for prior approval to conduct crypto business, and instead allow banks to independently participate in crypto asset activities within the “permissible” scope, but emphasize that they must follow the principles of safety and soundness and do a good job in risk management.

This means that Bank of America has greater autonomy in various types of encryption businesses such as custody, stable currency reserves, issuance of digital assets, and node operations. FDIC Acting Chairman Travis Hill said that the new policy is "a reversal of the flawed practices of the past three years" and that the FDIC will take a series of measures to provide new paths for banks to participate in encryption and blockchain activities. He criticized previous regulations for discouraging innovation through non-public means and acknowledged that banks had not been given clear guidance in the past.

This change in stance is consistent with the actions of the U.S. Office of Comptroller of the Currency (OCC): The OCC also clarified in early March that national banks can carry out crypto custody, stablecoin payments and other businesses, and revoked the old guidance requiring pre-approval.

As for the Federal Reserve, Governor Michelle Bowman also agreed in the same speech that "legitimate companies should not be excluded from the banking system in the name of regulatory policies" and called for a "reasonable and supportive" regulatory attitude towards new technologies.

Overall, U.S. regulatory agencies, under the leadership of the new government, are returning to the main line of "supporting innovative development", easing compliance resistance but requiring banks to strengthen their own risk controls. This will enable the U.S. banking industry’s compliance requirements for encryption businesses to shift from “pre-licensing” to “on-the-fly monitoring”, maintaining high standards in anti-money laundering, network security, consumer protection, etc., while not erecting unnecessary obstacles to new businesses.

2.2. Potential effects in Europe

The shift in U.S. policy immediately attracted European attention. To put it bluntly, the European Union does not want the negative impact of digital dollar hegemony on Europe.

Eurozone finance ministers discussed the new stance of the United States on March 10, 2025, expressing concerns that the United States’ embrace of crypto-assets may affect Europe’s monetary sovereignty and financial stability. Eurogroup Chairman Donoghue made it clear that he linked this issue to Europe's own autonomy and the resilience of the euro, and emphasized that the launch of a digital euro has become even more critical.

Villeroy, executive member of the European Central Bank and President of the Bank of France, warned: "The United States' encouragement of crypto assets and non-bank finance may be sowing the seeds for future turmoil." Once a financial crisis occurs, it may come from the United States and Europe. It can be seen that European regulators are cautious about the encryption-friendly policies of the United States and are worried about the expansion of US dollar-denominated stable coins in the euro zone.

However, on the other hand, the EU itself is also advancing the framework: the "Crypto Asset Market Regulation" (MiCA) passed in 2024 sets licenses and specifications for stablecoin issuance and encryption service providers, and supports innovative development under the premise of "clear regulatory requirements."

Some large banks in Europe have already laid out their digital asset business in advance. For example, Standard Chartered Bank has obtained a Luxembourg license to carry out crypto custody, and Societe Generale has issued Euro stablecoins. This shows that the EU's overall strategy is to strictly control risks while not giving up digital financial innovation.

The U.S. policy shift may prompt the EU to accelerate the implementation of MiCA and strengthen the digital euro process to prevent the impact of U.S. dollar crypto assets on the euro system while ensuring that Europe does not fall behind in a new round of financial innovation.

As for the UK, although it has left the EU, it has similar concerns to the EU in terms of financial supervision.

On the one hand, large British banks (such as HSBC and SCB) pay close attention to U.S. trends due to their global business; on the other hand, the British government announced its vision of building a "global crypto asset center" as early as 2022. Under the new policy environment, the United Kingdom may be more active in promoting its own version of crypto regulatory reform and releasing signals to support innovation in sync with the United States.

In short, all walks of life in Europe are taking the lead in the United States to prevent risks and promote regulations. The policy tone may be fine-tuned but there will not be extreme changes in deregulation.

2.3. Singapore continues to open up

The Monetary Authority of Singapore (MAS) has taken an open and cautious attitude towards the crypto industry in recent years, and the US move is expected to strengthen this trend.

In fact, Singapore has already adopted a license system to manage digital payment token exchanges, allowing Crypto.com, Coinbase Singapore, etc. to operate under licenses, and will release a regulatory framework for stablecoins in 2023 (requiring single-currency stablecoins to have sufficient reserves, etc.).

MAS also leads projects such as "Project Guardian" and explores the application of DeFi (Decentralized Finance) in the financial market with banks such as JPMorgan Chase and DBS. As it is already at the forefront of regulating innovation, Singaporean regulators may not respond directly to the FDIC statement, but the loosening of US regulations has reduced Singapore's concerns, proving that its policy of "supporting regulated innovation" is correct.

It is foreseeable that MAS will continue to improve local regulations (such as expanding guidance on banks' custody of cryptoassets and promoting more institutional-level innovation pilots), and strengthen cooperation and communication with the United States and Europe through international forums (such as the Financial Stability Board and the Basel Committee).

Overall, Singapore will view the U.S. pivot as a positive sign, cementing its position as Asia-Pacific’s crypto-finance hub.

2.4. Hong Kong follow-up strategy

Hong Kong has restarted its encryption hub strategy in 2023, and the new decree will undoubtedly add impetus to it.

The Hong Kong Monetary Authority (HKMA) sent a letter to banks in April 2023, clearly requiring support for the banking service needs of licensed crypto exchanges and not excessively raising the due diligence threshold.

At that time, banks such as Standard Chartered, HSBC, and Bank of China Hong Kong were cautious due to concerns about regulatory risks. In response, the HKMA emphasized that "do not let due diligence become an unnecessary obstacle." Now that the United States has lifted its implicit restrictions on banks, international banks will have less concerns about providing encryption services in Hong Kong. The previous efforts of Hong Kong regulators have been confirmed.

Since 2024, Hong Kong has issued the first batch of virtual asset exchange licenses and continues to promote the implementation of stable currency regulatory arrangements. It is expected that the Hong Kong Monetary Authority and the Securities Regulatory Commission (SFC) will take the opportunity to increase publicity to show that Hong Kong's regulatory environment is in line with the latest international trends, and encourage local and overseas banks and financial institutions to carry out compliant encryption businesses in Hong Kong.

In fact, Hong Kong is actively recruiting mainland and overseas crypto companies, and "seizing the opportunity of the U.S. shift" is expected to attract more trading volume and companies to Hong Kong. It is worth noting that the Hong Kong subsidiaries of Bank of China Hong Kong and China Construction Bank Asia with Chinese backgrounds have previously kept a low profile due to the mainland's attitude. However, as policies become clearer, these banks' participation in digital asset innovation in Hong Kong may accelerate.

In terms of regulatory response, Hong Kong government officials have repeatedly expressed in public recently that they welcome the world's balanced policy on encryption, emphasizing Hong Kong's institutional advantages.

It can be expected that Hong Kong will strengthen its "regulatory sandbox" and "firewall" mechanisms: on the one hand, it will maintain separation from mainland regulations and avoid cross-border risks; on the other hand, it will make full use of the increased confidence of U.S. and international capital in the compliant encryption market to consolidate and expand Hong Kong's influence as a bridgehead for the compliant encryption market.

Generally speaking, mainland China continues to use Hong Kong as a bridgehead for encrypted digital currencies, which can isolate risks without completely breaking away from new trends in the world, so as to maintain a situation in which it can advance, attack, and retreat.

2.5. Mainland China continues to exert high pressure

Mainland regulatory authorities still adopt a high-pressure ban on cryptocurrency transactions (digital currency transactions, mining and other activities are strictly prohibited). In the short term, U.S. deregulation will not directly change mainland China’s policy orientation.

Official media and regulatory agencies are likely to maintain their consistent tone, emphasizing the risks of crypto speculation, saying that previous strict supervision has effectively isolated external risks. This point can also be found in the warnings of some European officials (that the United States' vigorous development of cryptocurrency may cause crisis risks and adversely affect Europe), and the mainland may use this to support the necessity of its financial risk prevention policies.

However, some Chinese economists have begun to call for a review of global trends. Shen Jianguang, vice president of JD.com and an economist, wrote that the United States has shifted its focus to promoting responsible innovation and development, and the new framework is expected to attract more institutions and technological innovations and strengthen the United States' dominant position.

He specifically reminded that as the world's largest crypto market, the policy shift of the United States has a huge driving effect on other countries, including the European Union, the United Kingdom, Japan, Singapore, the United Arab Emirates, etc., which are all formulating regulations to support the development of stable coins and cryptography. It is recommended that China pay close attention to and conduct a comprehensive evaluation. This shows that domestic think tanks are beginning to worry that China will fall behind due to "one size fits all" in this round of financial technology competition.

It is expected that mainland officials will not relax the transaction ban in the short term, but may double investment in areas such as blockchain technology and digital renminbi to cope with the development of overseas crypto finance. At the same time, it is not ruled out that regulators may study and formulate new policies in a low-key manner: while insisting on prohibiting currency speculation, they will also provide certain guidance for domestic enterprises to participate in international digital financial cooperation (such as cross-border trade currency, overseas listed companies’ chain-related business).

In short, mainland China’s regulatory attitude is still mainly wait-and-see and risk warning in the short term, but in the long term, it does not rule out adjusting the regulatory framework for legal blockchain applications and tokenized asset transactions after evaluating global experience to avoid being at a disadvantage in digital economic competition.

3. Changes in investor sentiment and risk preferences

The release of new guidance from the FDIC and the overall shift in the U.S. regulatory environment have significantly boosted the confidence of market participants. Overall, investor sentiment has turned from wait-and-see to optimism, and risk appetite has increased. The specific manifestations are as follows:

Investor sentiment picked up and prices responded positively.

The United States clearly supports banks' participation in encryption, which is regarded as an important milestone in the further mainstreaming of cryptocurrency, and investors are therefore inclined to increase allocations. In fact, since the results of the US election were clear at the end of 2024, the price of Bitcoin has rebounded sharply. Although it has fallen back somewhat, it is still as high as $80,000. Industry analysts attribute this to the new administration making encryption policy a national priority and providing regulatory clarity.

After the release of the FDIC statement, although the prices of Bitcoin and Ethereum fluctuated in the short term, they generally remained at a high level, indicating that the market has factored in most of the positive regulatory benefits. Crypto-related stocks also performed strongly: Take the US Coinbase exchange as an example, its stock price has continued to rise since the first quarter in anticipation of an improvement in the regulatory environment. Bernstein and other institutions predict that Coinbase's stock price is expected to rise another 64% from the current level, on the grounds that clear U.S. regulatory clarity will push encryption deeper into the financial mainstream.

There are also signs of increased risk appetite in traditional financial markets. For example, some chain-related concept stocks (mining companies, blockchain companies) in the U.S. stock market outperformed the market after the news was released.

Overall, policy easing has swept away the cloud of uncertainty that has shrouded the market, with investor confidence rising and buying willingness increasing.

Market evaluation and media opinions diverge.

The crypto industry responded enthusiastically to the guidance, while the mainstream media was relatively rational and positive.

Rob Nichols, president of the American Bankers Association (ABA), publicly praised the FDIC’s new guidance, saying he “welcomes the FDIC’s decision to allow regulated institutions to conduct crypto-related businesses without prior approval,” noting that such regulatory clarity is critical to promoting innovation. This kind of endorsement from the top management of traditional finance has greatly enhanced the market's confidence in the durability of the policy.

Crypto media such as Decrypt and CoinDesk have described this move as a "major turning point", believing that this marks the end of the United States' "Operation Chokepoint 2.0"-style suppression. Many commentators compared it with the conservative approach of the previous government and believed that the current policy is friendly and open.

At the same time, some conservative voices also appeared in the media. Some financial commentators warn that the regulatory shift could lead to bubbles and accumulation of risks. ECB officials bluntly stated that the U.S. move may "sow the seeds of a financial crisis." Some traditional economists in China used Wall Street's bubble in the 1930s as a metaphor, joking that "the next Wall Street crash may make people miss the Great Depression." These voices have generated certain risk warning reports in the mainstream media.

But overall, the tone of the media is positive: when reporting on this matter, mainstream U.S. financial media (such as the Wall Street Journal, Reuters, etc.) focused on how the policy can lift the shackles of industry development and the positive reactions of all parties. For example, Reuters mentioned that the new regulations "completed a major shift in federal bank policy" and cited the views of market participants to affirm its significance. This kind of positive public opinion guidance has further consolidated investor confidence. New dynamics emerged in risk appetite and capital flows.

With regulatory endorsement, market participants’ risk appetite has significantly increased.

In the past few years, due to regulatory uncertainty, many institutional investors and commercial banks were cautious or even wait-and-see about getting involved in crypto. Now with clear policies, many institutions have begun to include crypto as a legal asset class in their strategic allocations. The CEO of DBS Bank Digital Exchange pointed out that professional investors are increasingly considering digital assets as a "legitimate part" of alternative investment portfolios.

U.S. hedge funds and family office funds reportedly returned to the Bitcoin market in large numbers in the first quarter, partly in response to the policy shift.

At the same time, the increase in market risk appetite is also reflected in the decline in volatility: after the introduction of good news, the volatility index of Bitcoin and others fell for a time, indicating that investors have weakened their expectations for downside risks and are more willing to hold them for the long term.

From the perspective of capital flows, the net inflow of stablecoins has increased, and investors are more confident about entering the market through stablecoins such as USDC and USDT, because the United States allows banks to hold stablecoin reserves, which is interpreted as official recognition of mainstream stablecoins. USDC issued by Circle received capital inflows in late March and returned to 1:1 anchoring. The shadow of trust that had previously plagued its development (such as the brief de-anchoring caused by bank failure) has obviously dissipated.

Generally speaking, the policy shift has made venture capital more willing to invest in crypto start-up projects, institutional investors have become more bold in allocating assets other than Bitcoin (such as Ethereum, Solana, etc.), and the sentiment of the entire market has changed from defensive to aggressive. Under this positive feedback mechanism, market confidence has improved significantly, laying the foundation for subsequent trading activity and market value growth.

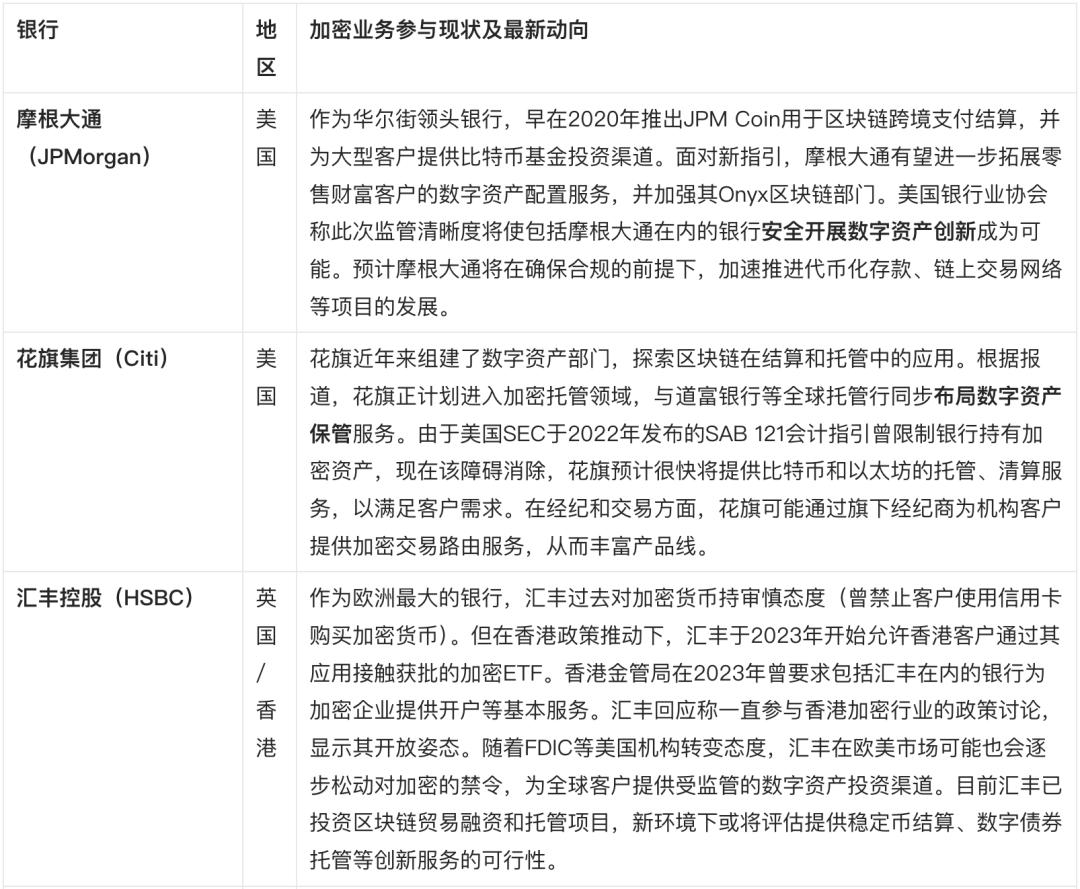

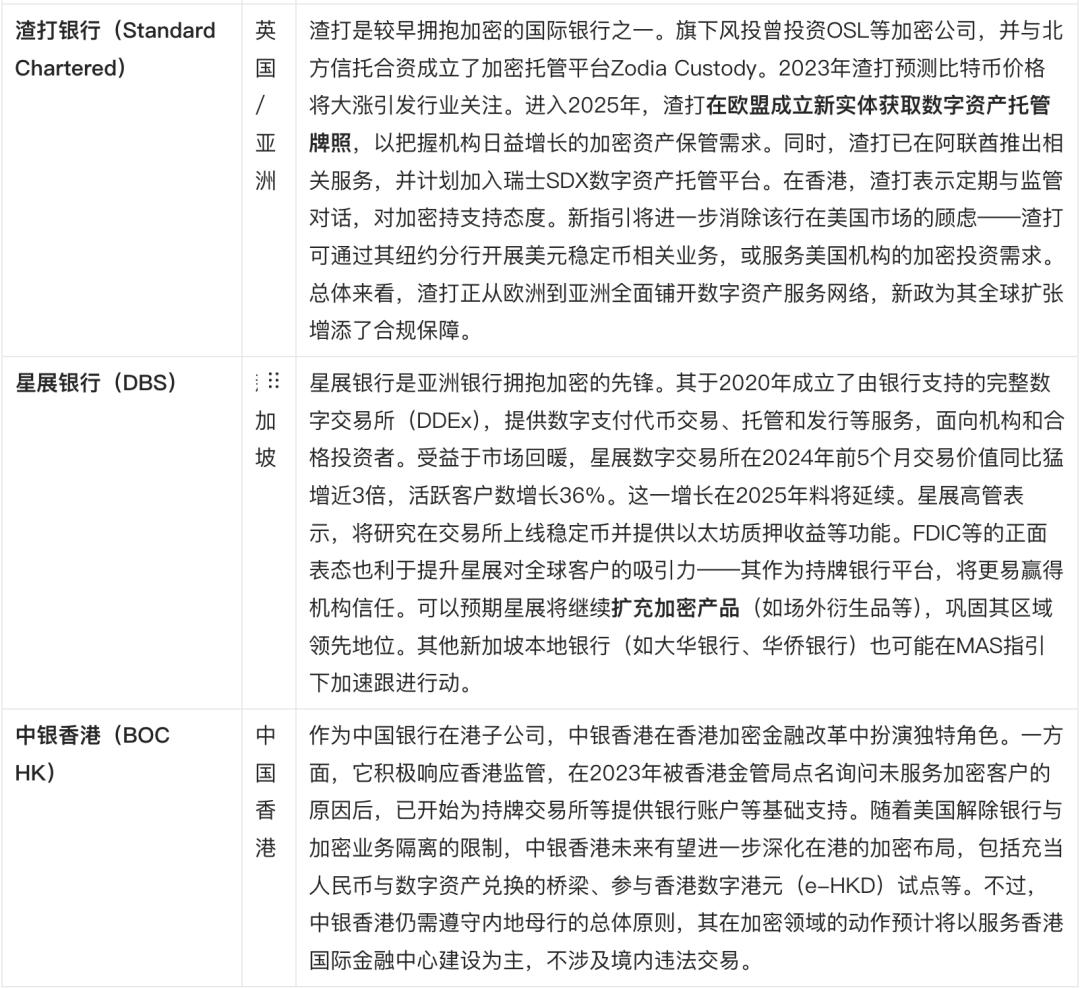

4. Boost from traditional banks getting involved in crypto business

The new FDIC guidelines have undoubtedly lowered the threshold for traditional banks to enter the crypto field and are expected to significantly affect the participation of major banks in crypto asset-related businesses. In general, this move will encourage more banks to try services such as custody, payment, DeFi and trading, but the responses of different banks may vary depending on their geographical strategies.

In the context of deregulated regulation, all types of banks in the United States, from community banks to large banks, have shown a higher willingness to participate.

The chairman of the American Banking Association's statement has conveyed a unified voice: the banking industry welcomes regulatory clarity and actively evaluates how to "compete safely and responsibly." This means that plans previously put on hold due to uncertainty will be restarted. For example, there are reports that more than 20 U.S. banks have received informal letters from regulators asking them to suspend their encryption business attempts, and now these institutions are expected to resume related projects.

On Wall Street, large investment banks and custodian banks are also moving quickly – Wells Fargo, Bank of America and others have established internal working groups to study the risk control requirements for crypto custody; asset management giant Fidelity has already been involved in digital assets and is expected to expand its service scope.

It is foreseeable that the U.S. banking industry will gradually move from marginal involvement (such as providing channels for customers to invest in Bitcoin funds) to directly providing encryption services (self-operated custody, trading, etc.), and the boundaries between traditional finance and digital asset ecology will become increasingly blurred.

The following lists the trends of some well-known banks to reflect the changes in bank participation in different regions:

The above-mentioned bank cases show that the interest of global banks in participating in encryption has increased significantly. Major American banks have begun to regard encryption as one of their legitimate business lines; European and Asian banks have been gradually piloting and expanding related services. It is foreseeable that more traditional banks will announce their entry into this field in the medium term: US custodian banks such as State Street Bank and Wells Fargo are planning to launch digital asset custody services as early as 2026 to meet strong customer demand.

These developments suggest that banks recognize that missing out on the crypto wave could mean losing future market position.

The new guidance serves as a “positive demonstration”: global banking regulators will pay close attention to the U.S. experience to remove obstacles or provide guidance and coordination for banks to participate in encryption in their respective jurisdictions. Of course, banks’ large-scale foray into crypto also depends on supporting policies (such as capital adequacy requirements). The Basel Committee has developed a framework for capital provisions for banks’ holdings of crypto-assets, and these prudential regulatory requirements remain a boundary condition for bank participation.

But overall, the FDIC's new policy has greatly raised the upper limit of bank participation: it sends a clear signal – compliant encryption business is no longer prohibited "one size fits all", but is recognized by supervision and will receive further guidance support. This will undoubtedly accelerate the integration of traditional finance and encryption markets, bringing more institutional funds, professional talents and reliable infrastructure to the encryption market.

5. Short-term fluctuations and mid- and long-term trend predictions 5.1. Short-term trading volume trends after the news is released

After the announcement of the FDIC guidance, the trading volume of major crypto assets showed obvious signs of amplification. The market interpreted the favorable regulations as a bullish signal, and buying activity increased. On the day the news was released and in the days that followed:

Bitcoin (BTC) and Ethereum (ETH): As a market benchmark, Bitcoin’s trading volume increased at the end of March. According to statistics, the 24-hour transaction volume of Bitcoin on March 29 was approximately US$27.06 billion. This level is somewhat higher than the average weekly level of the week before the news (Bitcoin’s average daily trading volume in mid-March was about 20-25 billion US dollars), indicating that a large number of funds quickly entered the market or adjusted positions after the news came out.

The futures market was also quite active during the same period, with CME Bitcoin futures positions reaching a new annual high, indicating that institutional investors also participated in the market reaction. In terms of Ethereum, the price is relatively sluggish but the trading volume has increased simultaneously – on March 27, the single-day trading volume of ETH exceeded US$20 billion, which was the first time in several months. This may reflect that investors expect Bitcoin to be more directly driven by favorable policies, and at the same time they also adjust some funds to mainstream currencies such as ETH during high prices, resulting in an increase in ETH volume and a stable price.

Overall, the total transaction volume of BTC and ETH increased by 10-20% month-on-month in the week after the policy was announced, indicating ample market liquidity.

Stablecoins (USDT, USDC, etc.): As a trading medium, stablecoins’ transaction and circulation scale has also increased simultaneously. In the week when the news was announced, USDT’s on-site trading volume on major exchanges once accounted for more than 60% of the total market trading volume, which shows that a large amount of funds poured into the digital dollar system from legal currency.

USDC market sentiment has also improved: the proportion of USDC transactions in many trading pairs has increased, indicating that investors’ trust in USDC is recovering (in contrast to the banking crisis in March 2023). According to blockchain data, the total amount of on-chain transfers of stablecoins jumped between 2024 and 2025: monthly transfer volume has increased from US$1.9 trillion in February 2024 to US$4.1 trillion in February 2025, an increase of 115%.

The growth rate during this year is quite astonishing, partly due to the policy shift in the first quarter of 2025 to attract large amounts of funds in and out through stablecoins, which accelerated circulation. As Reuters analysis stated, stablecoins are now a key cog in the multi-trillion-dollar crypto trading market, undertaking the function of moving funds between different currencies and legal currencies. The United States' statement of allowing banks to hold stablecoin reserves will further consolidate the status of USDT, USDC, etc. as trading infrastructure. In the short term, their trading volume and issuance market value have shown an upward trend. It is worth mentioning that World Liberty Financial, supported by former U.S. President Trump, plans to launch a new U.S. dollar stable currency "USD1" and says it will be fully supported by reserves such as U.S. Treasury bonds and cash. This news attracted market attention in late March. The addition of new stablecoins may lead to a battle for the market share of existing stablecoins. However, in the short term, USDT and USDC still firmly dominate, ranking among the top in terms of trading volume.

Mainstream trading platforms: The trading volume of major crypto exchanges in the United States, Europe and Asia increased overall under the influence of the news. Among them, in the U.S. market, compliant exchanges such as Coinbase and Kraken have benefited significantly – favorable regulations have prompted some platform funds that had previously moved offshore to return to the country. Coinbase's single-day spot trading volume at the end of March increased by about 20% from the beginning of the month, and the rise in its stock price also reflected the increase in trading activity. Kraken’s volume on USD trading pairs also amplified.

In comparison, global platforms such as Binance and OKX are still ahead in terms of size. Binance’s 24-hour global spot trading volume in the week of the announcement was stable at tens of billions of dollars, more than twice that of the second largest exchange. This shows that despite regulatory changes in the United States, Binance and others have a large user base in Asia Pacific and Europe and still occupy the leading position in transaction volume in the short term.

However, it is worth noting that changes in U.S. policies may push Binance US and others to adjust their strategies and even seek closer cooperation with U.S. regulations in terms of compliance to retain local users.

In the Asian market, exchanges such as OKX and Huobi maintain high popularity among Chinese-speaking and Southeast Asian users, and their BTC and ETH trading volumes increased by double digits at the end of March.

In addition, the Korean market has always responded quickly to regulatory and market changes. The day after Upbit, South Korea's largest exchange, announced good news in the United States, the trading volume of the Bitcoin Korean Won pair surged, and its ranking once jumped to second place in the world, second only to Binance. This reflects that Asian retail investors are encouraged by international policy signals and actively enter the market. In Hong Kong, the trading volume of newly licensed exchanges (such as OSL and HashKey) is still at a small start, but favorable regulations have attracted more local investors to try to open accounts, which has also laid the foundation for the future growth of these platforms.

5.2. Mid- to long-term trend outlook

Looking to the mid-to-long term, crypto market trading volume is expected to maintain growth and undergo structural changes under the new regulatory environment:

Overall transaction volume continues to rise.

As traditional financial institutions enter the market and more investors participate, the depth and breadth of the crypto market will expand. The participation of institutional investors will bring huge incremental funds, making the market's average daily trading volume expected to reach a higher level than the current level. Some analysts predict that if the macro environment cooperates and supervision remains friendly, the price of Bitcoin may hit a new high in 2025, and its global daily transaction volume may reach hundreds of billions of dollars by then. The daily trading volume center of the entire crypto market will also increase with the increase in market capitalization.

Although there is still a gap between the average daily volume of the foreign exchange market of US$7.5 trillion, the encryption market, as an emerging asset, is growing much faster than the traditional market – the annual growth rate of transaction volume is expected to remain at double digits, higher than the growth rate of the stock and foreign exchange markets. Especially considering the transactions of derivatives and on-chain DEX (decentralized exchanges), these parts that are not fully reflected in traditional statistical calibers are also expanding rapidly.

The regional market is changing, and the share of compliance platforms is increasing.

In the long term, as regulatory frameworks in various regions improve, global transaction volumes may become more geographically dispersed and balanced. Currently, Asia (including transactions by North American users on offshore platforms) accounts for about half of the global volume, while Europe lags behind. In the future, Europe has the potential to increase the proportion of European time zone trading volume after MiCA is implemented and the trading platform obtains compliance status. At the same time, the domestic market share of the United States is expected to rebound: over time, U.S.-compliant exchanges (such as Coinbase) and Wall Street’s traditional market makers will occupy a larger proportion of the trading volume list. Once the United States approves spot ETFs such as Bitcoin, a large amount of trading volume will flow between exchanges and traditional markets through ETF arbitrage and other forms, which will also significantly increase the trading volume during the daytime period in the United States. Accordingly, the market share of giants such as Binance may be gradually eroded, and the market will move from "one super and many strong" to "multi-polar competition." However, since Binance and OKX already have a large user base and liquidity network, it is expected that they will still maintain the lead in Asia and emerging markets, but their share will decrease relatively. In addition, exchange compliance will lead to healthier volumes: as false wash volume and the like are curbed, the quality of reported trading volumes increases.

In the long term, the rise of compliance platforms in various countries will help put an end to the "wash sales" criticized in the industry and allow true supply and demand to be reflected in transaction data.

Trading varieties and structures evolve.

In the medium to long term, the composition of transaction volume may change—the proportion of Bitcoin and mainstream currencies decreases, and the proportion of other assets increases. As the market matures, investors will not only trade "blue-chip" coins such as Bitcoin and Ethereum, but will also participate more in the transactions of new varieties such as tokenized physical assets and central bank digital currency (CBDC). For example, if the United States launches a Bitcoin ETF or a new type of treasury bond token backed by government-held Bitcoin reserves, its transactions may divert some transactions of traditional crypto assets. In addition, if CBDC issued by central banks of various countries can be interoperable, they may also enter the market through trading pairs similar to stable currencies. The transaction volume in the DeFi field is also expected to increase and occupy a place – after banks enter DeFi, they may launch compliant decentralized trading platforms or liquidity pools, allowing some transactions to be migrated to the chain for completion. Although these changes will be limited in scale in the short term, in the long run, the "crypto market" will no longer refer only to Bitcoin, but will include a wider range of digital financial products, and its transaction volume statistics will also need to keep pace with the times. It can be expected that in the medium to long term, the trading ecology of the crypto market will be more diverse and the distribution of volume and energy will be more balanced.

Improved liquidity and reduced volatility.

Increased trading volume usually means greater market liquidity and thicker buying and selling orders. In the medium to long term, this should help reduce price volatility and reduce the possibility of a single large player manipulating the market. Especially when banks and licensed institutions participate in market making, the market depth is greatly increased and can absorb larger transactions without impacting prices. However, it should be noted that new entry of funds may also bring risks such as increased leverage transactions. If excessive leverage accumulates, it may amplify short-term fluctuations. Therefore, we expect the overall volatility of crypto assets to trend downward (gradually approaching the levels of traditional assets) in the medium to long term, but may still experience severe oscillations under specific events (such as negative macro or changes in regulatory winds). The continued improvement of supervision and the development of risk management tools (such as options, futures and other derivatives markets) will be important factors in calming volatility.

6. Conclusion

In summary, the new guidelines issued by the FDIC not only have an immediate impact on the U.S. banking industry's participation in the crypto market, but also enhance global market confidence through the regulatory "demonstration effect" and promote the injection of traditional financial forces into this emerging field.

In the short term, the trading volume of major crypto assets and trading platforms has increased significantly, and market sentiment is optimistic. In the medium to long term, under the dual effects of regulatory support and the influx of institutions, the crypto market is expected to usher in a new stage of steady expansion in transaction volume and optimization of the participant structure.

Of course, easing supervision does not mean laissez-faire – how local supervision refines rules and harmonizes international standards will determine how far this “encryption trend” can go.

Overall, the FDIC's new policy sends a positive signal: as long as risks are controllable and compliance is in place, the development space of the cryptocurrency market will be further opened up, and its trading activity and integration with traditional finance will increase significantly in the next few years.

(over)