There are more and more bizarre operations in the fund industry.

“The fund manager ran away first”

In the past few days, the fund has attracted a lot of attention.

Some Christians complained that they had been investing in their own medical funds for several years, and when they saw some hope of getting their money back, the fund manager ran away first. The anxiety and anger can be felt across the screen.

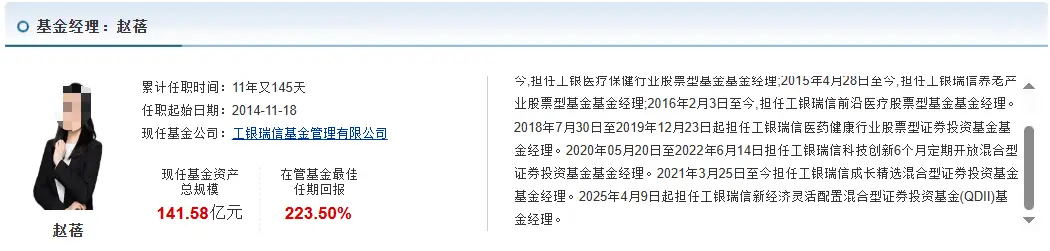

The fund he bought was ICBC Credit Suisse Frontier Medical Stock. The fund manager in charge of this fund is Zhao Bei, the "goddess of medicine" who was once held on a pedestal by Christians.

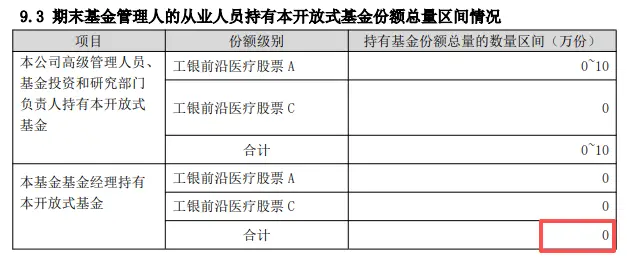

The source of the news is the 2025 fund annual report. In the column "Holds of the Fund by Employees of the Fund Manager at the End of the Period", Zhao Bei's personal holdings are shown as 0.

And when the mid-term report is released in 2025, the data in this column will still be 100,000 to 500,000. Based on the net worth at the time, this share was worth about 4.7 million. 4.7 million, just gone—oh no, it was redeemed by her.

What’s even more intriguing is that this redemption is likely to occur in the second half of 2025, which happens to hit the small high point of the pharmaceutical sector’s rebound. You know, around September 2025, the innovative drug index will rebound by about 30%, driven by warm policies and recovery in market sentiment. Before that, the pharmaceutical sector had just survived a three-year bear market.

What is this like? Just like your neighbor's stock trading, every time he goes in at a low point and comes out at a high point, no matter how you look at it, you feel that this person is really lucky. But when you find that the fund you bought suffered a huge loss and the fund manager accurately retreated at a high point, your mood is not just "envy".

And this isn't the first time she's done this.

Looking at the historical track of Zhao Bei's holding of this fund, she bought 500,000 to 1 million shares for the first time in 2019, and redeemed them until only 0 to 100,000 shares were left in 2020. In 2023, she felt that the valuation was low and bought back 100,000 to 500,000 shares, and finally cleared all her positions in the second half of 2025.

In other words, from 2019 to 2025, her operations on this fund were to increase positions at low points and reduce positions at high points almost every time.

She is worthy of being the "goddess of medicine" and her operation is quite precise.

According to regulatory regulations, fund managers must use at least 40% of their performance bonuses for the year to buy funds they manage. These shares must be locked for at least one year and cannot be sold. Zhao Bei's operation is indeed in compliance with the regulations, and there is nothing wrong with redeeming it after the lock-in period expires.

But compliance is one thing, being reasonable is another. There is an even more disturbing number. Data shows that the ICBC Credit Suisse Frontier Medical Fund has collected a total of 655 million yuan in net management fees alone for 10 years since its establishment.

All this money comes from the pockets of Christians. And most of the Christian people have not yet recouped their money.

Christian people pay management fees every year, and fund companies make a lot of money, but Christian people's accounts are still green. Who can bear the gap?

"Goddess of Medicine"

As a "medical goddess" of the generation, why did Zhao Bei end up like this?

Zhao Bei is indeed very capable in the fund circle. She joined ICBC Credit Suisse in 2010 and is currently the co-general manager of the research department. Together with Gulen of China Europe Fund, she is known as the two top players in the pharmaceutical field. She studied pharmacy as an undergraduate and later obtained a master's degree in finance. She is one of the few fund managers in the industry with dual backgrounds in both pharmacy and finance.

This kind of composite background is quite rare among pharmaceutical fund managers. When others look at pharmaceutical companies, they may only look at financial reports. She can see the company's valuation model from the drug's R&D pipeline and clinical trial data. The professional barriers are indeed high.

Her playing style is also very unique. The average fund manager selects stocks from the bottom up and digs out companies one by one. Zhao Bei's idea is to start from the top down, first determine which subdivisions of the entire pharmaceutical industry have great opportunities, and then select core companies there. She compared the pharmaceutical industry to a pond, saying that a macro perspective allows you to know where there are more fish, and then invest more heavily in it.

The great pharmaceutical bull market from 2019 to 2021 was the highlight of her style of play. At that time, she keenly captured the explosive opportunities in the CXO (pharmaceutical R&D outsourcing) track, and her position increased from less than 5% at the end of 2018 to about 40% in 2019.

The net worth of ICBC Frontier Medical soared from 1.12 yuan to 5.04 yuan, an increase of almost 350%. At its peak in 2021, the scale of this fund reached 21.1 billion, and Zhao Bei’s total personal management scale exceeded 30 billion, making her a veritable “goddess of medicine.”

But all track-type fund managers have an inescapable problem: when the track is good, you are a god, but when the track is not good, you are a trap.

Starting in the second half of 2021, the pharmaceutical sector will enter a three-year bear market. Centralized purchasing policies come one after another, the valuation bubble of innovative drugs bursts, and CXOs have overcapacity… Every piece of news is hitting pharmaceutical funds. ICBC Frontier Medical has retreated all the way from its high point, and now it still has a 36% decline from its 2021 high.

What's even more terrible is that most of the holders of this fund rushed in at the high price from 2020 to 2021. In other words, they missed the rise perfectly, experienced the fall completely, and are still lying in the pit.

Looking at the performance data, data from Tiantian Fund Network shows that as of now, ICBC Frontier Medical A’s return rate in the past year is 18.09%, ranking 514th among 671 similar funds.

None of the other funds she manages are ranked high, and some are even lagging behind.

A few years ago, who would have thought that the “Medical Goddess”’s fund ranking would drop to the bottom third?

As for her ICBC Growth Select Mix A, it is even more difficult to describe. Since this fund was established in 2021, it has experienced a cumulative retracement of 26.18%, with a return of -3.40% in the past three years.

So the current situation is very embarrassing. In the annual report, Zhao Bei continued to shout that he was optimistic about the overseas expansion of innovative drugs, CXOs, and devices, saying that he continued to "conform to the allocation ideas of the industry and the development direction of the times." But when Jimin looked at the losses in her account, and then saw that she had liquidated all her shares, she would inevitably think: You said you were optimistic, so why are you running?

Actions speak louder than words, and this is especially true in the investment community.

Who is making money and who is losing money?

After talking about Zhao Bei, let’s talk about ICBC Credit Suisse Fund.

It is the first banking fund company in China. Its major shareholder is Industrial and Commercial Bank of China. It was established in 2005. Relying on ICBC's nationwide branches and huge customer base, ICBC Credit Suisse has a natural advantage in fixed income products. Data shows that as of the end of 2025, it manages 272 public funds, 653 annuities, special accounts, and special portfolios, and the total asset management scale reaches 2.37 trillion yuan.

And its money-making ability is pretty amazing. According to the 2025 annual report of ICBC, ICBC Credit Suisse’s full-year net profit reached 3.007 billion yuan, a year-on-year increase of 42.5%. This number has set a record high since the company was founded, ranking among the highest among all fund companies that have disclosed data.

Seeing this, you may ask: Isn’t it great that the company is making so much money? Aren’t Christians supposed to make money?

The problem lies here.

ICBC Credit Suisse's net profit has surged in the past two years, which is mainly supported by two revenue sources. One is the management fee, and we rely on our huge scale advantage to collect money steadily. The other part is that the company used its own funds to buy a lot of equity funds when the market was low, and made a lot of money after the market picked up. But the money earned from self-operated investment has nothing to do with the Christian people.

More importantly, from the perspective of scale and structure, ICBC Credit Suisse has actually fallen into a rather embarrassing situation. As of the end of 2025, its public management scale is approximately more than 870 billion, but more than 70% of it are bond and currency funds, and equity funds account for less than a quarter.

Fixed-income funds are its basic market, but the growth of this basic market is actually slow. The management scale of monetary funds has only increased by less than 80 billion from 2021 to now. Against the background of the surge in the overall scale of the industry, this speed can be said to be standing still.

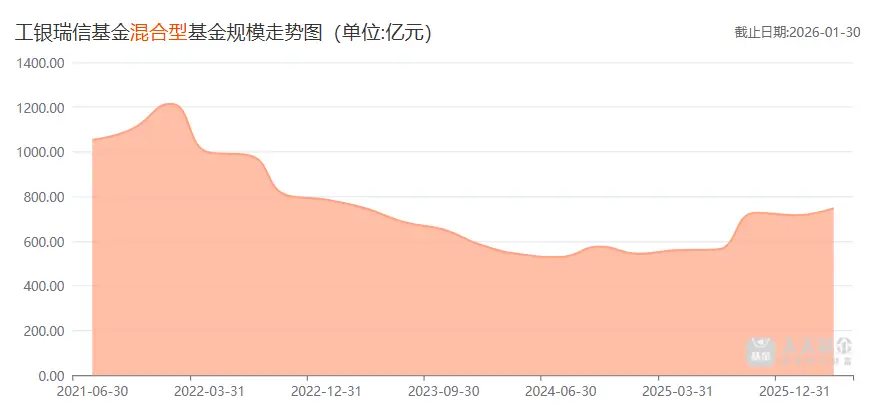

Looking at equity funds, it is even more difficult to describe. In 2021, the scale of ICBC Credit Suisse's hybrid funds will still be 120.5 billion, but by the end of 2024 it will only be 73.5 billion, a drop of nearly 40% in four years. Moreover, in 2022 and 2023, ICBC Credit Suisse’s funds suffered a total loss of 45 billion for two consecutive years.

On the one hand, the company's net profit hit a record high, and on the other hand, the basic people suffered large losses. The sense of dislocation in the middle makes me feel awkward just thinking about it.

Veteran leaves

If it is an old problem to charge too much management fees and cause miserable losses to the public, then the most worrying thing about ICBC Credit Suisse in recent years is actually the problem of personnel loss.

In the past few years, ICBC Credit Suisse has experienced a fierce wave of veteran departures. Just list a few names: Yuan Fang, Jiang Huaan, Zhang Yufan… Which of these people is not the leader of all lines of ICBC Credit Suisse?

Yuan Fang, known as ICBC Credit Suisse’s “Equity Sister”, managed ICBC’s cultural and sports industry stocks for ten years, and her performance was quite impressive. She suddenly resigned in 2022.

Jiang Hua'an, a leader in FOF investment in the industry, is known as the "First Brother of FOF". After his resignation in 2025, ICBC Credit Suisse's successor in the FOF business has been replaced by a newcomer with less than 30 days of management experience.

Zhang Yufan, one of the heads of equity investment research, directly canceled his qualifications and left the public offering industry completely.

Wind data shows that since 2022, 18 fund managers from ICBC Credit Suisse have resigned, covering equity, FOF, fixed income, QDII and other fields. This makes people have to wonder: Is this a normal flow of talents, or is there a systemic problem in the investment research system?

Some people point the finger at the company's incentive mechanism – banking fund companies are inherently more conservative than private fund companies in terms of equity incentives and business unit systems. In addition, in the past two years, they have made great efforts to reduce costs and increase efficiency, and the remuneration advantages of outstanding fund managers have been chipped away little by little.

There is also a deeper problem, which is ICBC Credit Suisse’s risk control system. Some reports mentioned that Zhao Bei’s team was unable to deploy some innovative targets in time due to risk control restrictions, and missed the opportunity of medical technology transformation.

You said that a fund manager who is known for his "keen capture of industry trends" is stuck and unable to move due to risk control. What does it feel like? It's like a racing driver driving a car with a limited speed. He can clearly see the curve and overtake, but he just can't press the accelerator.

When a fund company's investment research system continuously loses core talents, and the remaining fund managers are restricted by various restrictions, how can the performance improve?

end

Objectively speaking, ICBC Credit Suisse is not without its own advantages.

For example, in its pension business, the total investment management scale has exceeded 1.2 trillion. This business is not only a stabilizer of revenue, but also an important support for the brand. Another example is that it holds full license qualifications for public offerings, special accounts, social security, pensions, etc., and its business structure is more diversified than many fund companies.

But back to Zhao Bei’s liquidation of self-managed funds, no matter how he explains it, the psychological impact on Christians is real.

Some people say that fund managers are also ordinary people. They have the need to stop profits and have personal financial plans. It is reasonable and reasonable to redeem self-purchased shares after meeting the lock-in period. This is indeed true in terms of laws and regulations. But from an emotional perspective, when the net value of a fund is still 36% lower than its high point, and a large number of holders are deeply involved, but the fund manager himself redeems all the self-purchased shares at the high point, this feeling is really difficult to rationalize.

For ICBC Credit Suisse, Zhao Bei’s incident may just be a public opinion crisis. If you handle it well and issue a statement to explain it, everyone will forget about it after a while. But the deeper problem is that when the profit model of fund companies and fund managers is decoupled from the profit experience of basic citizens for a long time, this rift in trust cannot be repaired by a few nice words from officials.

The entire public fund industry is thinking about a question: How to truly tie the interests of fund managers and citizens? Relying on the mandatory self-purchase required by regulatory requirements and being able to sell after one year of lock-in is obviously not enough. Relying on the moral consciousness of fund managers seems too fragile in front of the market.

In the final analysis, the management fees of fund companies are taken out of the pockets of the Christians, who are the real bread and butter. When a fund company makes a net profit of 3 billion, if most citizens are still losing money, the halo of 3 billion will be a bit dazzling.

Zhao Bei's liquidation of self-managed funds is, on the surface, a personal operation of the fund manager, but when taken apart, it exposes the long-standing interest mismatch problem in the fund industry.

I hope this incident can sound a wake-up call to the industry, and that ICBC Credit Suisse can get out of the quagmire of brain drain and truly return to the main line of "making money for investors."

After all, no matter how big a sign is, if only the company itself is full and the citizens are still hungry, the sign will be smashed sooner or later.