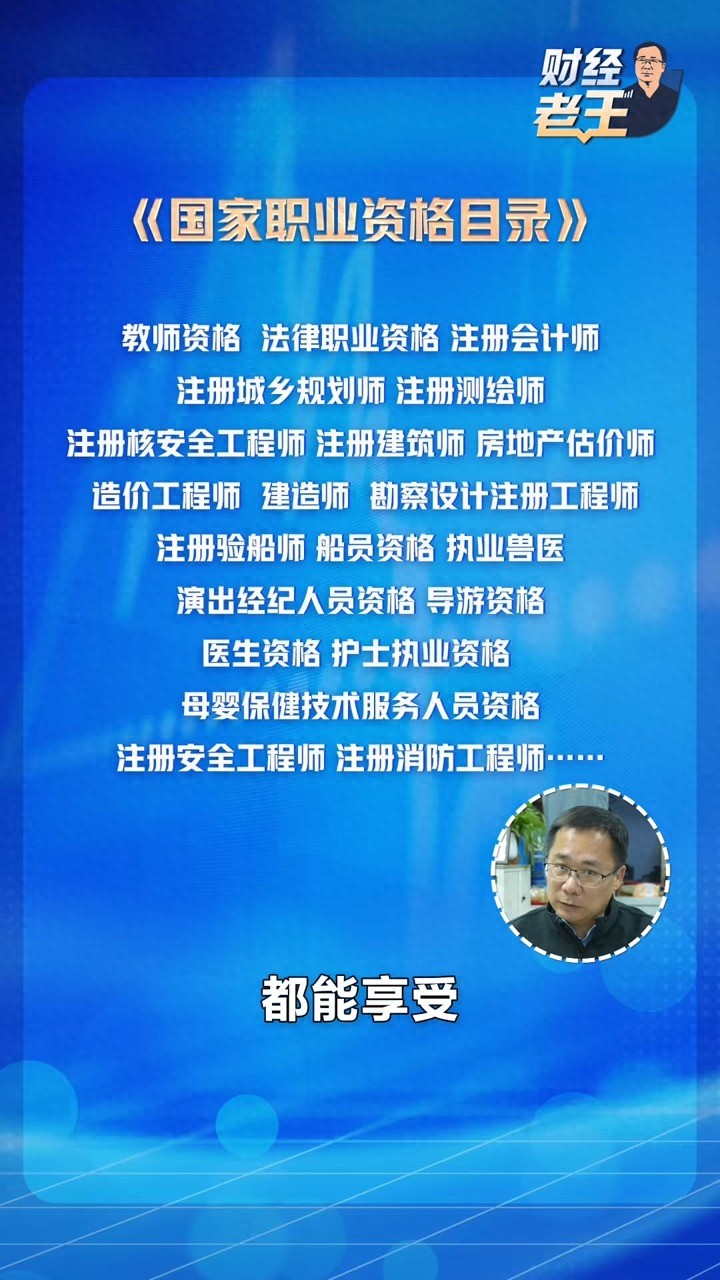

A quick overview of the New Deal

According to the "Guiding Opinions of the State Administration for Market Regulation, Ministry of Housing and Urban-Rural Development, Ministry of Housing and Urban-Rural Development, and the State Administration of Taxation on Promoting the Efficient Completion of Enterprise Relocation Registration "One Thing" (Guoshi Jianzhufa [2025] No. 48), optimize cross-regional tax relocation services. The migration service area provides a pre-check function for tax migration. Enterprises can independently check whether there are any outstanding tax-related matters before applying for migration. After the market supervision department completes the relocation registration, the relocation service area will push the change information such as the company's domicile (business location) to the tax department. For enterprises that have no outstanding matters, the tax department will immediately relocate them and provide "one-stop" relocation services for the enterprises at the place of relocation, and provide timely guidance to taxpayers in handling tax-related matters. For enterprises with outstanding matters, the tax department will provide feedback on the specific content and handling methods of the outstanding matters through the migration service area.

1. The processing time for the final settlement and settlement of comprehensive personal income tax in 2024 is from March 1 to June 30, 2025. Please take the time to apply.

2. If an enterprise enjoys corporate income tax preferential policies, it should collect and complete the retained information for inspection after completing the annual settlement and settlement for verification by the tax authorities.

To declare asset loss deductions to the tax authorities, enterprises only need to fill in the annual corporate income tax return form "Details of Pre-tax Deductions and Tax Adjustments for Asset Losses" and no longer need to submit information related to asset losses. Relevant information shall be retained by the enterprise for future reference.

3. If an employer that participates in social insurance premiums has an increase or decrease in employees, it should first go through the registration procedures for increase or decrease in employees with the human resources and social security and medical insurance departments. After completion, it can declare and pay through the electronic tax bureau and social insurance premium management client.

4. "High temperature allowance" VS "heatstroke prevention and cooling fee" corporate income tax pre-tax deduction policy

High temperature allowance: According to Article 34 of the "Regulations on the Implementation of the Enterprise Income Tax Law of the People's Republic of China", reasonable wage and salary expenses incurred by the enterprise are allowed to be deducted. The wages and salaries mentioned in the preceding paragraph refer to all cash or non-cash labor remuneration paid by an enterprise to employees who serve or are employed by the enterprise in each tax year, including basic wages, bonuses, allowances, subsidies, year-end salary increases, overtime wages, and other expenditures related to employees' employment or employment.

Therefore, the high-temperature subsidies paid by enterprises to workers according to the prescribed standards and included in the calculation of total wages can be directly deducted before corporate income tax.

Heatstroke prevention and cooling expenses: According to Article 40 of the "Regulations on the Implementation of the Enterprise Income Tax Law of the People's Republic of China", employee welfare expenses incurred by an enterprise shall be deducted if they do not exceed 14% of the total wages and salaries.

According to the provisions of Article 3, Paragraph 2 of the "Notice of the State Administration of Taxation on the Deduction of Enterprise Wages, Salaries and Employee Welfare Fees" (Guo Shui Han [2009] No. 3), various subsidies and non-monetary benefits issued for employees' health care, life, housing, transportation, etc. Expenses for medical treatment in other places on business, medical expenses for employees of enterprises that do not implement medical coordination, medical subsidies for employees’ immediate family members, heating subsidies, employee heatstroke prevention and cooling expenses, employee hardship subsidies, relief funds, employee canteen fund subsidies, employee transportation subsidies, etc. are within the scope of enterprise employee welfare deductions.

Therefore, the heatstroke prevention and cooling fees paid by an enterprise to employees cannot be directly deducted before corporate income tax. They should be deducted before tax in accordance with the employee welfare deduction limit standards. That is, the employee welfare expenses incurred by the enterprise shall not exceed 14% of the total wages and salaries. The deduction is allowed.

Hot questions and answers on special additional deductions

Let’s see together

↓↓↓

How to deduct the care of infants and young children under 3 years old? Deducted by whom?

Taxpayers' expenses related to caring for infants and young children under the age of 3 are deducted at a standard rate of 2,000 yuan per infant per month. Parents can choose to have one of them deduct 100% of the deduction standard, or they can choose to have both parties deduct 50% of the deduction standard. The specific deduction method cannot be changed within a tax year.

How to deduct children’s education? Deducted by whom?

Expenditures related to full-time academic education for taxpayers’ children will be deducted at a standard fixed amount of 2,000 yuan per child per month. Parents can choose to have one of them deduct 100% of the deduction standard, or they can choose to have both parties deduct 50% of the deduction standard. The specific deduction method cannot be changed within a tax year.

What does academic education include?

Academic education includes compulsory education (primary school, junior high school education), high school education (general high school, secondary vocational education, technical education), and higher education (college, undergraduate, master's, and doctoral education); children aged 3 years or older who are in preschool education before entering primary school can be deducted based on their children's education.

Can parents with multiple children choose different deduction methods for different children?

Can. Parents with multiple children can choose different deduction methods for different children. That is, for child A, one party can choose to deduct the care or education of infants and young children under 3 years old at the standard of 2,000 yuan per month. For child B, they can choose to have both parties deduct the care or education of infants and young children under 3 years old at the standard of 1,000 yuan per month.

How is continuing education deducted?

Answer: Taxpayers’ expenses for continuing academic (degree) education in China will be deducted at a fixed amount of 400 yuan per month during the academic (degree) education period. Taxpayers’ expenditures on continuing education for skilled personnel’s vocational qualifications and continuing education for professional and technical personnel’s vocational qualifications will be deducted at a fixed amount of 3,600 yuan in the year in which the relevant certificates are obtained.

*Warm reminder: Continuing education for professional qualifications that are not included in the "National Vocational Qualification Catalog" is not deductible.

How is the deduction time for continuing education determined?

Continuing education for academic qualifications (degrees) refers to the month from the month of admission to continuing education for academic qualifications (degrees) in China to the month when continuing education for academic qualifications (degrees) ends. The maximum deduction period for continuing education for the same academic qualifications (degree) shall not exceed 48 months. Continuing education for professional qualifications for skilled personnel and continuing education for professional qualifications for professional and technical personnel shall be the year in which the relevant certificates are obtained.

Can I report my parents’ medical expenses for serious illnesses?

Can't. Taxpayers can report eligible serious medical expenses incurred by themselves, their spouses, and their minor children. The deductions for medical expenses incurred by the taxpayer, their spouse, and their minor children can be calculated separately in accordance with regulations.

A couple has serious medical expenses at the same time and wants to deduct all of them from the husband. Is the deduction limit 160,000 yuan?

If both husband and wife have qualifying medical expenses for major illnesses at the same time during the year, they can choose to deduct them both from one of them. The deduction limits are calculated separately. The maximum deduction limit for each person is 80,000 yuan, and the total maximum deduction limit is 160,000 yuan.

How to understand the “first set” of housing loan interest?

The so-called first home loan refers to a home loan that enjoys the first home loan interest rate when purchasing a house. Note that taxpayers can only enjoy a one-time deduction for interest on their first home loan.

Can housing loan interest and housing rent deductions be enjoyed at the same time?

Can't. Taxpayers and their spouses cannot enjoy special additional deductions for housing loan interest and housing rent respectively within a tax year.

How to deduct housing rent?

The housing rental expenses incurred by taxpayers who do not own their own homes in their main cities of work can be deducted in accordance with fixed quotas. If the taxpayer's spouse owns his own house in the taxpayer's main city of work, it will be deemed that the taxpayer has his own house in the main city of work.

The taxpayer's company is located in location A, and he is sent to work in the branch in location B. Neither the taxpayer nor his spouse has a house in location B. They rent a house in location B due to work reasons. Can the taxpayer enjoy housing rent deductions? If so, which city's standard deduction should be used?

Eligible taxpayers can enjoy a housing rent deduction for their expenses on renting a house at their primary place of employment. The main place of work refers to the place where the taxpayer is employed. If the place of employment is inconsistent with the actual place of work, the actual place of work shall be the main city of work. In this question, the taxpayer's current actual place of work (main place of work) is place B, and he should enjoy housing rent deductions according to the standards of place B.

How to deduct the elderly support for non-only children?

If the taxpayer is not an only child, the monthly deduction limit of 3,000 yuan will be shared between him and his siblings, and the amount shared by each person cannot exceed 1,500 yuan per month. The support can be shared equally or by agreement, or the dependent can designate the share. If the apportionment is agreed or designated, a written apportionment agreement must be signed, and the designated apportionment takes precedence over the agreed apportionment. The specific allocation method and amount cannot be changed within a tax year.

The uncle has no children, and the taxpayer actually bears the obligation to support the uncle. Can the expenses for supporting the elderly be deducted?

Can't. Dependents refer to parents who are over 60 years old, and grandparents who are over 60 years old and whose children have died. Father-in-law, mother-in-law, father-in-law and mother-in-law, uncles and aunts, etc. do not meet the conditions for dependents stipulated in the "Interim Measures for Special Additional Deductions for Individual Income Tax".

Producer | Xiaodong Editor | Xiaolu

Editor-in-Chief丨Xiao Fei Editor丨Da Ming