Financial News Agency, February 21 (Editor Zhao Hao) An executive from Apollo Global Management said that the private equity industry is facing a long period of pain in software investment because the industry failed to realize in time that new technologies such as artificial intelligence will subvert this long-term favorite track for private equity.

David Sambur, partner and co-head of private equity at Apollo, said in an interview, "People are only now starting to realize that there is going to be a multi-car pileup on the software investment highway. In fact, all the signs are there in 2022."

Sambur noted that the launch of OpenAI’s artificial intelligence (AI) chatbot ChatGPT about three years ago, along with a higher interest rate environment, were the initiators of the sell-off in technology stocks that has roiled the market in recent weeks.

Wall Street has been selling off software stocks recently, as investors worry that a new generation of AI tools from companies like Anthropic could eventually make existing software-as-a-service (SaaS) providers obsolete.

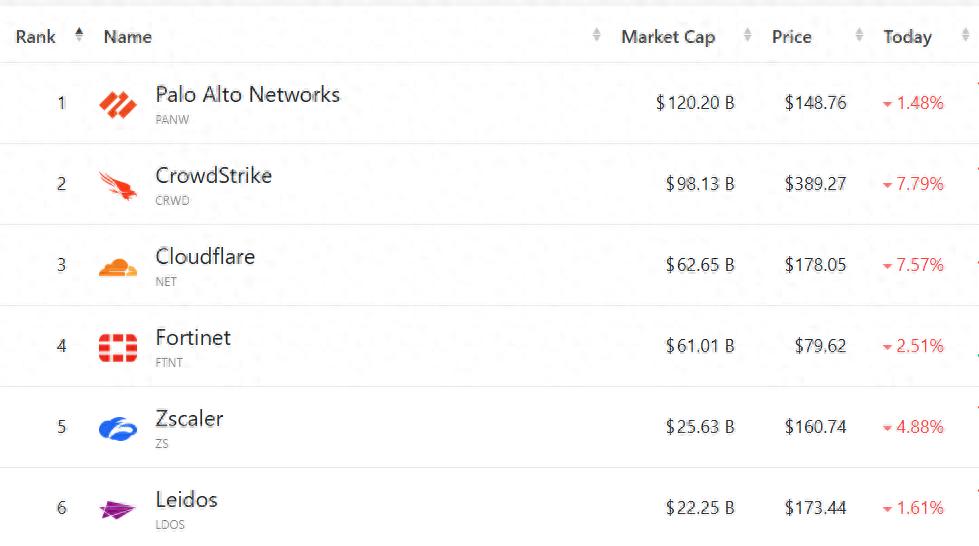

Earlier in the day, Anthropic introduced a new feature in its AI model that can scan the code base for security vulnerabilities. Affected by the news, CrowdStrike and Cloudflare both fell by more than 7%.

The private equity industry has greater exposure to SaaS because they value these software companies' stable, predictable revenue models that rely on a loyal customer base. Private equity firms have invested heavily in this area over the past few years, setting a record of $348 billion in 2021.

Sambur said, "Did we fall into groupthink, like 30% to 40% of M&A transactions are concentrated in the software field? In hindsight, this is actually a pretty big red flag. When people look back at this stage, they will see that this was a failure of risk management."

As many pandemic-era software investments near the end of traditional private equity holding cycles, concerns are growing about whether these companies can sell assets at desirable prices and realize returns. It could also harm private equity firms' fundraising plans and their ability to pursue new deals.

Sambur said the industry needs to prepare for a "much needed reset" in valuations as investors reassess software companies' economic models and future growth rates. "When you actually sell these businesses, you'll see the results, and that process will take time to fully unfold."

As of December 31 last year, Apollo had approximately US$938 billion in assets under management. According to Sambur, the company's private equity business has "zero exposure" to the software sector, and its exposure at the group level is less than 2%.

But even so, Apollo's stock price is still dragged down by the industry, and has fallen by more than 14% this year.

Apollo Private Equity management, which includes Sambur, said in a letter sent to clients this week that the company's decision to "avoid this area was based on investment and risk management considerations rather than a blanket rejection of the entire industry."

There are winners and losers in the software industry, but "among leveraged equity funds, we believe the potential returns are insufficient to match the risk," they wrote. The letter also stated that Apollo will continue to look for new opportunities brought about by market turbulence.

Other well-known M&A institutions have also recently reassured investors, emphasizing that their exposure to the software field is limited or controllable. Sources say Thoma Bravo and Vista Equity Partners have met with investors to allay concerns.

(Zhao Hao, Financial Associated Press)