Why are the prices of different option contracts with the same subject matter and the same expiry date more expensive than others?

The reason lies mainly in intrinsic value.

1. What is intrinsic value?

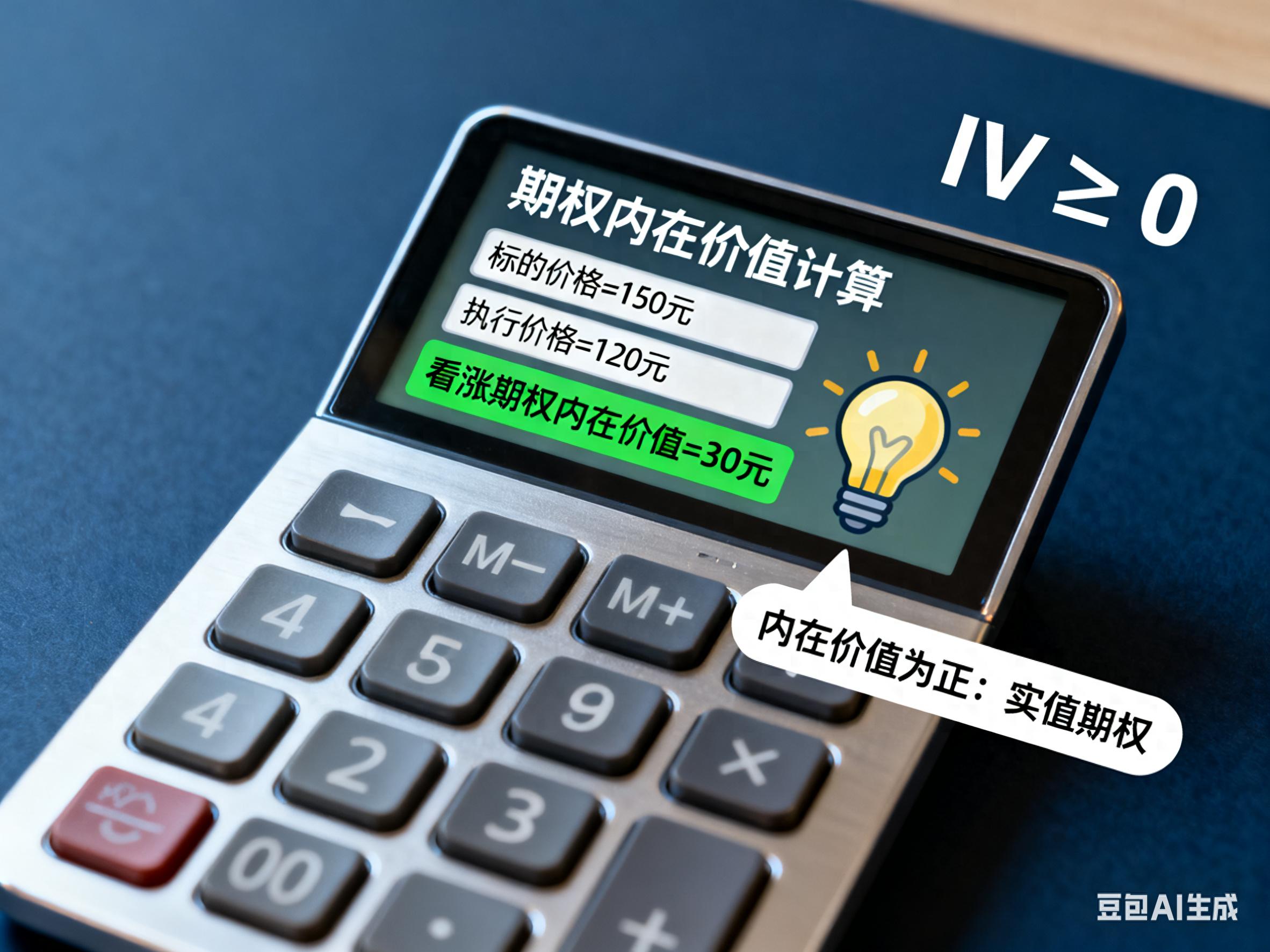

Intrinsic value refers to the income that the buyer can obtain if he exercises the option immediately, without considering option costs and transaction costs.

For example, there are two unexpired call options: A has an exercise price of 90 yuan, and B has an exercise price of 110 yuan. When the underlying asset price is 100 yuan:

If call option A with an exercise price of 90 yuan is exercised immediately, a profit of 10 yuan will be made, and this 10 yuan is the intrinsic value;

If call option B with an exercise price of 110 yuan is exercised immediately, it will lose 10 yuan, which means it has no intrinsic value.

2. How does intrinsic value affect option prices?

If the above call options A and B are on sale, which one do you think has a higher price?

Obviously A. Because it has an intrinsic value of 10 yuan and can bring 10 yuan of income to the buyer, it is more valuable. In fact, the intrinsic value of 10 yuan constitutes the "floor price" of option A and represents the "real" value part of the option.

Suppose another call option C comes with an exercise price of 80 yuan. When the underlying asset price is 100 yuan, who is more expensive, C or A?

The answer is C, because C has an intrinsic value of 20 yuan and can bring 20 yuan of income to the buyer, while A has an intrinsic value of 10 yuan and can bring 10 yuan of income to the buyer.

It can be seen that the greater the intrinsic value, the higher the benefits to the buyer and the more expensive the option price.

Intrinsic value is determined by the relationship between the exercise price and the price of the underlying asset. When the underlying asset price is constant, the lower the call option exercise price, the greater the intrinsic value and the more expensive the option price.

For example, as shown in the screenshot below, when the Shanghai Silver 2512 futures price is 11393, the exercise price of the call option decreases from 11400 to 10500, while the intrinsic value increases and the option price becomes more expensive.

If there is no intrinsic value, the option with a lower exercise price will be more expensive. This is because the lower exercise price is closer to the price of the underlying asset and is more likely to have intrinsic value. For example, in the screenshot, the option price with an exercise price of 11,400 is more expensive than the option with an exercise price of 11,500.

Screenshot from: Flush Futures

For puts, the opposite is true. The higher the strike price, the greater the intrinsic value (or the greater the likelihood of becoming intrinsically valuable), and the more expensive the option, as shown in the screenshot below.

Screenshot from: Flush Futures

3. Intrinsic value is dynamic

To understand intrinsic value, you should also pay attention to one thing: intrinsic value is not static, but changes with the price of the underlying asset. For example, for a call option with an exercise price of 100, as the underlying price fluctuates, the intrinsic value changes as follows:

That is, as the price of the underlying asset changes, the intrinsic value may increase or decrease. Therefore, an option that has intrinsic value when purchased may become intrinsically valuable, and an option that has no intrinsic value may become intrinsically valuable.