Promoting blunt words can "keep your card"

"Can anyone help me buy a ticket for the Spring Festival Gala, preferably one with a microphone and able to go on stage. I can go up and tell the story of my POS machine." At the end of 2022, Zhao Zhao (pseudonym), an acquiring and payment POS machine agent, posted such a circle of friends.

The story of Zhao Zhao and POS machines began in 2016. During this year, Zhao Zhao began to carry a bag and walk around the streets to sell goods, and gradually developed a deeper relationship with POS machines. Gag-style "jokes" are also advertisements issued by Zhao Zhao to promote POS machines. There are many such contents in his circle of friends.

The agent's main job is to sell POS machines to merchants through various channels, and can obtain corresponding profits based on the card transaction flow generated by the activated POS machines. In the seven years since Zhao Zhao entered the industry, with the adjustment of regulatory policies, the marketing model in the acquiring field has also been constantly changing.

A reporter from Beijing Business Daily learned that telemarketing is one of the main ways for individual users to come into contact with POS machine promotion. By briefly introducing the POS machine brand, card payment rates, machine fees and other information, the telephone customer service conducts a preliminary screening of interested customers. Zhao Zhao told a reporter from Beijing Business Daily that the POS promotion calls received by users are usually not made directly by agents. This type of model is called intra-city work orders in the industry, and on this basis, the off-site electronic sales model is derived.

"Professional telemarketing agencies obtain interested customers by making phone calls, and payment agents receive orders in the form of work order delivery for a fee. They contact customers based on the information provided by the telemarketing company and come to promote POS machines. After that, most agents directly promote POS machines to users in other places by mail." Zhao Zhao explained.

The aforementioned promotion method casts a wide net, which can help agents acquire more customers in a short period of time, and has become the choice of many agents. But Zhao Zhao was unwilling to poke his head into the tiger's mouth and engage in such a risky business. Zhao Zhao said frankly that the first step in intra-city work orders is to buy and sell user information. The user data held by telemarketing agencies is used repeatedly. While there are legal risks, the transaction cannot be maintained for a long time, and it is often deceptive in the nature of one shot for another.

Unable to find customers through shortcuts, Zhao Zhao, like many other agents, left his contact information on public social platforms to accumulate "friends" and constantly posted information about POS machines in his personal circle of friends. "Once someone sends a signal that they want to know about POS machines, agents will rush to them and get their contact information before making further introductions." Zhao Zhao pointed out.

A reporter from Beijing Business Daily further investigated and found that labels such as “card maintenance”, “cash out”, “low rates” and “capital turnover” are high-frequency words in agents’ circles of friends. In some agents’ circles of friends, POS machines are even labeled as “bad debt repair tools.” On public social platforms, due to platform restrictions, agents often use words such as "stable", "personal version" and "no price increase" when promoting.

There are also small advertisements for POS machine agents, which are posted in the elevator of the community where reader Liu Qin (pseudonym) lives in Beijing. They are clearly marked with words such as "You can apply for a POS machine by swiping your card at any time if you have a credit card" and "It's faster to raise your credit card if you have a card." According to Liu Qin, this advertisement is firmly pasted on the left side of the elevator floor button and can be seen by everyone who enters the elevator. "After all, it is illegal to cash out a credit card. I tried to take it off but failed. Some neighbors also used labels to block the QR code for contact, but it was torn off again within a few days." Liu Qin said.

“Strictly review the qualifications of special merchants and standardize the management of acceptance terminals,” this is the clear policy of the regulatory agency. According to the requirements, no unit or individual is allowed to buy or sell POS machines and other acceptance terminals online. Banks and payment institutions should conduct on-site inspections of all physical merchants and check the usage locations of their acceptance terminals one by one. However, judging from the current implementation situation, this provision is almost in name only.

Personal Internet access "lost"

Illegal matching transaction merchants

Business is not doing well.

According to data disclosed by the central bank, in 2022, there were 3.3754 million fewer connected POS machines than the previous year.

Investigating the reason, Wang Pengbo, chief analyst of Broadcom Consulting, said that due to the impact of the epidemic in recent years, the overall economic growth has slowed down, and the demand for POS machines in physical businesses has declined. At the same time, innovation and changes in payment products continue. Alternative products to traditional POS machines are increasing, including direct transfers, mobile payment tags, etc., and new products are more convenient and lower-cost, gradually eroding the usage scenarios of traditional POS machines, and the promotion of POS machines has encountered bottlenecks.

Rampant advertising and marketing also targets a wider group of individual users. It has almost become an open secret in the acquiring field for individual users to cash out at POS machines.

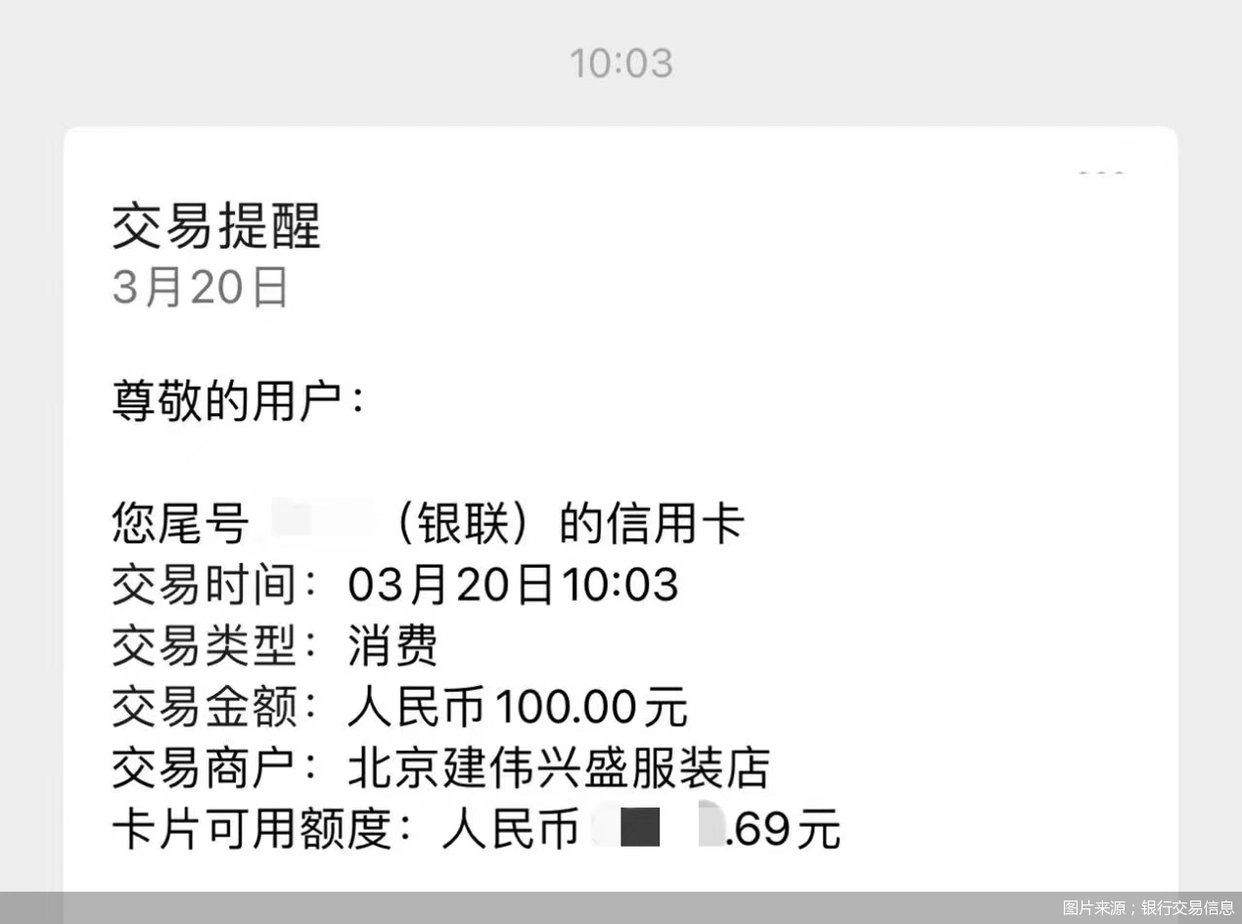

According to information released on public social platforms, a reporter from Beijing Business Daily obtained a Lakala (300773) POS machine from agent Li Yu (pseudonym) without any hindrance at a price of 59 yuan with free shipping, and further tested its activation process. Based on Li Yu's reminder, the reporter registered as a "small and micro merchant" and independently selected the merchant type and name. Store information such as door photos and cashier photos are not required. In the end, with the help of real personal information and false merchant information, the reporter quickly passed Lakala's review and registered as a merchant with a single credit card credit limit of up to 300,000 yuan, with a credit card fee rate of 0.6%.

After completing the registration and activation, the Beijing Business Daily reporter used his own credit card to swipe the card on the POS machine. However, bank transaction details showed that the payee was Beijing Jianwei Xingsheng Clothing Store. The system automatically matched the new transaction information, and the card amount reached the bound account immediately after deducting the handling fee.

During this test, Beijing Business Daily reporters never encountered the widely criticized situation of free POS machines charging deposits. However, based on the interview content, the melee around POS machines also occurred between different agents of the same payment institution.

Li Yu is engaged in Lakala POS machine agency, charging 59 yuan for the machine, which can be refunded after the cumulative transaction reaches 5,000. For the same machine, Zhang Hua (pseudonym), an agent who posted advertisements in Liu Qin Community, asked to pay a deposit of 299 yuan, and said that the charging standards for the POS machines he represents are uniformly between 299 yuan and 300 yuan, and the deposit will be returned after a total of 20,000 yuan is swiped every month for 12 months.

During the communication process, Li Yu "intimately" provided some tips on how to increase the credit limit and maintain the card, and emphatically recommended not to use debit cards at POS machines, as this could easily be judged as money laundering by the system; Zhang Hua emphasized several times that "regular UnionPay registration machines have deposits" and "without a deposit, it is not an official product."

In fact, in the past two years, disputes over POS machine deposits have been reported frequently, and a large number of agents have even used free services as a gimmick to deduct deposits without users' knowledge. In Zhao Zhao's view, these are "cautious tricks" used by agents for their own profits. Agents who swipe debit cards receive less profit, and it is nonsense to say that regular products require deposits.

When it comes to POS machine deposits, Zhao Zhao pointed out that the statement "regular products have deposits" is actually just a way for agents to obtain profits. This is also part of the decentralized authority of payment institutions. Whether POS machines will collect deposits depends entirely on whether the agents have set up deposit deductions. This function is indeed a "livelihood" set aside by payment institutions for agents.

"If some users mind the deposit, then the agent can recommend machines without deposit; if some users don't care about the money, the agent will naturally make more profits. As for the transaction turnover threshold set for refunding the deposit, it is essentially to encourage users to use more POS machines to swipe their cards." Zhao Zhao added.

Regarding the issue of selling POS machines to individual users, Zhao Zhao even admitted frankly that agents are looking for profits, and the demand of real merchants to use POS machines is limited after all. After the POS machines are promoted, how to use them and who will use them are not issues that agents will consider.

Wang Peng, a researcher at the Beijing Academy of Social Sciences and the Intelligent Social Governance Research Center of Renmin University of China, said that cashing out on credit cards is essentially creating false transactions and illegally applying credit card credit limits. Such behavior is separated from the supervision of financial institutions and can easily lead to the transmission of financial risks.

Wang Pengbo pointed out that in principle, individuals, that is, natural persons with no other attributes, cannot handle POS machines where users swipe their bank cards. Only merchants with business activities and consumption scenarios can handle POS machines. However, due to competition and profit considerations, some offline acquirers have relaxed the management of their own or franchised service providers.

In addition, in response to the aforementioned issues related to the direct registration of Lakala POS machines, on March 20, a reporter from Beijing Business Daily also conducted an interview with Lakala. Lakala only responded that the company has strict requirements for merchants to access the network, especially for agents to expand merchant access to the network, and strictly implements the real-name management of merchants to access the network. If cash out, fraud and related risky transactions are discovered, early warning and interception or settlement delay will be adopted to ensure the safety of payments and funds. Regarding the issue of deposits collected by some agents, agents will be urged to return them promptly after the merchants meet the standards.

Wang Pengbo further analyzed and pointed out that illegal matching of merchants is a common method for pure personal cash-out. The fictitious transactions and illegal cash-out behaviors of payment institutions during the use of POS machines are obviously non-compliant.

Intense attack and defense

Rate adjustment involves many parties

"No telemarketing, no cheating, and no cashing out" are the "three no's policies" Zhao Zhao has set for his career. Specifically, they do not promote POS machines through phone calls, text messages, etc., do not use "free" as a gimmick to defraud users of deposits, and do not directly handle cash-out services for customers through their own POS machines.

Each of the "three no's policies" basically points to the chronic diseases of the POS machine industry, but it is also difficult to fully operate within the regulatory red lines. Zhao Zhao said that the competition in the existing POS machine agency market is too fierce. Agents of the same payment institution can provide users with "price lists" of varying amounts. Agents of different payment institutions will also use methods such as switching machines to persuade customers to use their own POS machines.

Switching, in the field of bank card acquiring, mainly refers to agents actively using another brand of POS machine to replace the user's original machine. In the past few years, Zhao Zhao has carried out POS machine promotion services for many payment institutions. Zhao Zhao said: "Changes in agencies will definitely take away all the customers that can be taken away. However, due to factors such as customer usage habits and changes in contact information, this step is not easy."

In the limited market, in order to pursue new customers, agents have also turned their attention to customers on other platforms. This has also caused many payment institutions to complain, and they have to resort to methods such as refuting rumors and issuing risk warnings. On the one hand, they want to retain their own users, and on the other hand, they also prevent users from being deceived by criminals during the phone switching process. On the Lakara POS machine registered by a reporter from Beijing Business Daily, the startup page prompts "Lakara will not ask for equipment change, please be vigilant and beware of being deceived."

Among the commonly used methods of machine cutting, it is more effective to send users information about the deactivation of the original machine, rate increase information, and free replacement of updated POS machines. Among them, the rate increase attracts more attention.

Since the second half of 2022, there has been a lot of news about the increase in card swiping rates at POS machines of payment institutions, and many agents are releasing corresponding information. Advertisements on agents’ WeChat Moments also focus on increasing POS machine rates, prompting users to switch to machines with lower card payment rates. Zhao Zhao pointed out, "For users, as long as it is a formal payment institution, the lower the fee, the better. When other payment institutions raise their interest rates, everyone will rush to promote their own agents' machines."

A practitioner in the payment industry told a Beijing Business Daily reporter that competition in the acquiring field is not only reflected among payment institutions, but also concentrated among agents. Rate adjustments involve many parties, including payment institutions, agents, and users, and are also sensitive to users. Payment institutions should adjust their rates based on the actual conditions of their business development, and should also prevent any impact on existing merchants. In addition, it cannot be ruled out that in the market competition, some agents fabricate information such as rate increases to maliciously cut off opportunities.

In Zhao Zhao's circle of friends, there was a lot of news about the price increase of Lakala POS machines. In response to this situation, Lakala responded that the company's card swiping rate has remained stable as a whole, and the company's overall card swiping rate is still at the level of 6‰ (six thousandths).

Wang Pengbo analyzed that cutting opportunities is vicious competition, which may not only cause market turmoil and damage the overall image of the industry, but may even allow merchants to become accomplices of criminals, causing damage to user funds. In recent years, costs in the acquiring industry have gradually increased, but interest rates have not increased. Overlay market demand has always existed, so even though competition in the industry is fierce, rates are still generally rising.

Expansion and chaos go hand in hand

Agent management cannot be relaxed

The seven years that Zhao Zhao has been engaged in POS machine agent promotion have also been seven years of changes in the payment industry. Regulators continue to draw prohibitive red lines and strictly supervise third-party payments, including POS machines; the five-year license renewal test, coupled with the impact of market competition, continues to reshuffle the payment industry.

Refined to the field of bank card acquiring business, the profit sharing mechanism promoted by POS machines has generated considerable profit margins, attracting more agents to participate, expanding the business territory and making the market more chaotic. Zhao Zhao revealed to a reporter from Beijing Business Daily that during the peak period, his monthly income could reach a maximum of 80,000-100,000 yuan, but now it has dropped significantly and has basically stabilized at 20,000-30,000 yuan.

When it comes to the reasons for the decline in income, Zhao Zhao is also well aware of it. "The threshold for entry into the industry is too low. When there are more people, it becomes chaotic," Zhao Zhao mentioned. "Agents who handle the promotion of POS machines are also very uncertain. They may be handling POS machines this month and promoting credit cards or selling houses next month. Agents only want to make 'quick money', and there is no way to guarantee customer after-sales service."

Wang Peng’s analysis pointed out that judging from the actual operation situation in the bank card acquiring field, different participants such as payment institutions, agents, and users are actually stakeholders, and they have not strictly implemented regulatory requirements, and they have acquiesced to relevant illegal activities to a certain extent. This further promotes the occurrence of POS mechanical sales, cash out and other behaviors.

Various problems caused by agents in promotion also point the finger at the licensed payment institutions behind them. While payment institutions are decentralizing their authority and obtaining benefits, they are also required to bear corresponding review responsibilities for agents and merchant access. A reporter from Beijing Business Daily learned from practitioners in the payment industry that in the second half of 2022, some institutions have begun to restrict some merchants by raising rates, and the adjustment targets are mainly merchants that cannot provide true business information. The purpose of this operation is still to standardize merchant transactions.

Lakala also mentioned in the reply that it has formulated strict agent management measures in accordance with regulatory requirements and industry norms, requiring them to conduct business in compliance, and standardizing agent behavior through daily inspections and compliance training. Once an agent is found to have violated laws and regulations, punitive measures will be taken and its business will be closed immediately, and false propaganda content will be required to be removed from the shelves, and its legal responsibility will be held.

Regarding the current problem of individual users accessing the Internet through the status of "small and micro merchants", Wang Pengbo further explained that in order to meet the business needs of small and micro merchants, regulatory regulations stipulate that merchant types include not only special merchants who have business premises and have gone through industrial and commercial registration, but also include entity special merchants among small and micro merchants who are exempt from industrial and commercial registration in accordance with laws, regulations and relevant regulatory provisions. However, small and micro merchants without a business license must obtain a personal identity document, plus some auxiliary certification materials such as his business location, in order to develop into a small and micro merchant acquiring orders. Only the acquiring agency can provide collection services for basic daily sales operations.

"The convenient payment path provided by regulatory agencies for small and micro merchants should not become a channel for payment institutions to make profits and individual users to cash out. Payment institutions cannot relax their management of agents." Wang Pengbo emphasized.

What should be done to rectify the chronic problems in the bank card acquiring field? Wang Peng gave the following suggestions: First, increase the intensity of investigation and punishment by regulatory authorities and establish diversified reporting methods to maintain market order; second, consolidate the main responsibilities of payment institutions, strictly regulate relevant rules and develop business, and form a standardized way of business development; third, strengthen publicity to the public and emphasize the dangers of using cards to maintain cards and cash out.

"In addition to strengthening management and punishment, the most fundamental issue is how to help third-party payment institutions find new profit growth points and win in the digital transformation." Wang Pengbo added.

Beijing Business Daily Financial Investigation Team