Under the sharp price reduction, lithium carbonate may take off the expensive hat of "white oil".

At present, lithium carbonate has started a "200,000 yuan defense battle." According to Wind data, the average price of domestic battery-grade lithium carbonate has dropped to 215,000 yuan/ton on April 6, down more than 60% from the high of 567,500 yuan/ton in November 2022.

As for the "bottom line" for lithium carbonate price reduction, there is still controversy in the market. Some people believe that the price of lithium carbonate is expected to fall to 100,000 yuan/ton and below, but some companies believe that 250,000 yuan/ton is the break-even line. According to The Paper, in the face of "continuously falling" lithium carbonate prices, half of the four major mica lithium extraction companies in Yichun, the "Lithium Capital of Asia", have chosen to suspend production.

Why do lithium carbonate prices continue to fall? What kind of disagreement does the market have on the bottom line of lithium carbonate price?

One of the reasons for price cuts: downstream demand is lower than expected

This is not the first time that the price of lithium carbonate has plummeted. According to Wind data, in July 2020, the price of domestic battery-grade lithium carbonate fell to a low of 40,000 yuan/ton. The sharp drop in the price of lithium carbonate back then had a similar reason to today's price drop of lithium carbonate – sluggish demand.

At the 7th Annual Lithium Battery & Electric Vehicle Industry Conference that reporters attended in March, Cui Dongshu, secretary-general of the Passenger Car Association, once said: "Why did the price of lithium carbonate fall in 2020? Because my country's new energy vehicle sales in 2017 and 2018 Volume grew rapidly and stagnated in 2019 and the first half of 2020. However, a large number of companies made high investments in 2018 and 2019, and there was an explosive oversupply and sluggish demand in 2020. "

According to data from the China Association of Automobile Manufacturers, sales of new energy vehicles in my country increased by 53.3% and 61.7% year-on-year respectively in 2017 and 2018, showing strong growth. In 2019 and 2020, my country's new energy vehicle sales fell by 4% and increased by 10.9% year-on-year respectively, almost stagnating.

If the sales of new energy vehicles are the support for the price of lithium carbonate, then the slowdown in the sales growth of new energy vehicles this year has "disrupted" the price of lithium carbonate. For the whole of 2022, my country's new energy vehicle sales were 6.887 million units, a year-on-year increase of 93.4%. On April 4, according to estimates from the Passenger Car Association, new energy vehicle manufacturers sold 1.48 million vehicles in the first quarter of this year, a year-on-year increase of only 25%.

Lin Shi, Secretary General of Intelligent Connected Vehicles and Automotive Analyst of the China-Europe Association, said in an interview with reporters: "Many lithium mining companies have miscalculated the growth rate of new energy vehicles. The cancellation of the new energy vehicle 'state subsidy' directly caused the new energy vehicle market this year not to continue last year's sales growth, with a growth rate of only 25% in the first quarter. Many lithium mining companies plan lithium ore production based on a 'double' growth rate, which leads to a mismatch between supply and demand."

It can be seen that the sales growth of new energy vehicles in my country has slowed down significantly since the beginning of this year, and the growth rate of downstream demand is lower than expected, which will inevitably lower the market's price expectations for lithium carbonate. This is one of the reasons for the decline in lithium carbonate prices.

The second reason for price reduction: The entire industry chain is facing overcapacity

"Supply and demand determine commodity prices." In addition to demand, the increased supply of lithium carbonate also "added fuel to the price decline."

Chen Jia, a researcher at the International Monetary Institute of Renmin University of China and an independent international strategy researcher, said in an interview with reporters: "The price of lithium carbonate has plummeted from the early peak of 600,000 yuan/ton to the current range of 200,000 yuan. The large drop and wide impact undoubtedly exceed the lithium carbonate industry's own expectations. Otherwise, in the past two years, many companies would have entered the upstream lithium resource industry chain, either crossing borders or increasing production."

Financial commentator Zhang Xuefeng also said in an interview with reporters: "The decline in lithium carbonate prices is mainly due to the increase in supply. In recent years, domestic lithium carbonate production capacity has continued to expand, coupled with the increase in foreign imports, resulting in excess supply."

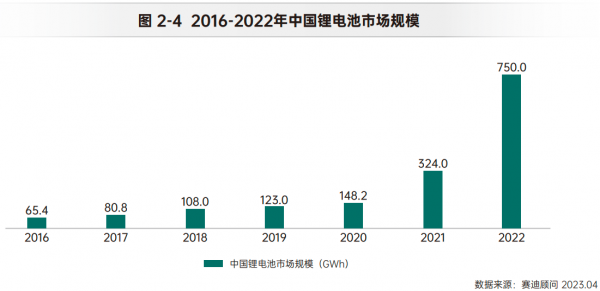

According to Huafu Securities Research Report, with the release of production capacity in South American salt lakes and Australian spodumene, global lithium supply will be 760,000 tons of lithium carbonate equivalent in 2022, will reach 1.047 million tons in 2023, an increase of 37.76%, and will reach 1.44 million tons in 2024, an increase of 37.53% year-on-year.

If the calculation is accurate, the increase in lithium resource supply this year may exceed the increase in new energy vehicle sales (only about 25% in the first quarter). As the penetration rate of new energy vehicles further increases, the release of lithium carbonate production capacity in 2024 may significantly exceed the sales growth of new energy vehicles. Simply put, "supply may rise faster than demand in the next few years," which casts a shadow over the price of lithium carbonate.

"I think the main reason (for the price reduction of lithium carbonate) is the disorderly expansion of the industry. Last year or the year before last, the price of lithium ore skyrocketed. Everyone was jealous when they saw that lithium mining companies could increase their net profits by hundreds of percent at every turn, and they all entered this industry. In addition, the threshold for the lithium ore mining industry is not high. , including vehicle companies and battery manufacturers, have invested in lithium mines, which has led to a large increase in lithium mining capacity this year and low demand, which has led to lithium mine prices having to come down, otherwise mining companies will not be able to ship and will increase inventory," Lin Shi told reporters.

In fact, the imbalance between supply and demand of lithium carbonate is just a microcosm of the overcapacity faced by the entire lithium battery industry. According to incomplete statistics from GGII, 268 new investment and expansion projects in China's lithium battery industry chain will be signed in 2022, including lithium batteries and materials. Based on the statistics of 247 projects with announced investment amounts, the total investment amount in China's lithium battery industry in 2022 will exceed 1.4 trillion yuan.

"If we broaden our horizons and jump out of the shackles of lithium carbonate prices and comprehensively examine the data of the entire lithium battery material industry chain, we will find that not only lithium carbonate, but other lithium battery materials including lithium phosphate have fallen even more sharply; comprehensive overcapacity of liquid battery basic materials such as cathode materials, anode materials, electrolytes, and separators has already begun to emerge in 2022, and the overcapacity at the entire industry chain level has been intensifying for a long time." Chen Jia said.

According to Wind data, the average price of domestic lithium iron phosphate electrolyte fell to 36,500 yuan/ton on April 6, and has continued to decline for the past year and a half. It has dropped 67.64% from the price high of 112,800 yuan/ton on October 13, 2021. The price of cathode materials also continues to decline. On April 6, the price of domestic lithium iron phosphate cathode materials fell to 88,500 yuan/ton, which was exactly "halved" from the price of 177,000 yuan/ton on November 8, 2022.

Overall, the entire lithium battery industry chain is facing a crisis of overcapacity. Zhang Jiujun, dean of the School of Materials Science and Engineering at Fuzhou University, said that it is predicted that the battery demand for new energy vehicles will exceed 1,200GWh by 2025. Although the prediction is not necessarily accurate, the current power battery production capacity planning of various manufacturers has exceeded 4,000GWh, which is much more.

According to incomplete statistics, as of the end of December 2022, the production capacity plans announced by battery factories, vehicle manufacturers and other cross-border enterprises have exceeded 4,800GWh, and most of the production capacity is planned to be launched in 2025 or before. In other words, if only the increase of new production capacity is considered and the elimination of old production capacity is not considered, the lithium battery industry may have serious overcapacity.

But Jia Hongtao, chief engineer of the power battery system at the Geely Automobile Group Research Institute, said: "With the development of the industry, all of our batteries are actually in the process of upgrading and iterating. This is not a simple upgrade. The past factories and production lines have to be eliminated and upgraded."

An industry insider told reporters: "Our entire equipment technology and product technology have been updated too fast. Now the technology from 5 years ago is already very backward." Therefore, if the elimination of old production capacity is included, the overcapacity in the lithium battery industry may not be too serious.

Mo Ke, chief analyst of True Lithium Research, also said in an interview with reporters that companies generally build production capacity moderately ahead of schedule, so there will be a bit of excess. However, the expansion of enterprise production is generally divided into many phases, of which the first phase will be realized. The construction of subsequent phases will depend on the utilization rate of the first phase to decide whether to maintain the original plan or adjust it, so overcapacity is not expected to be too much.

Despite this, most experts, scholars and industry insiders interviewed by reporters believe that overcapacity in the lithium battery industry will appear from 2023 to 2025. Regardless of whether this overcapacity is serious or not, it will have a certain negative impact on the price of lithium carbonate.

The third reason for price reduction: Car price war forces car companies to reduce costs

"From the perspective of direct causes, the prisoner's dilemma effect caused by a large number of companies in the upper reaches of the industry chain rushing to sprint for production capacity in the early stage, and the backlash effect caused by the price war in the automobile retail market triggered by Tesla's large price cuts in the lower reaches of the industry chain, are the 'culprits' of the rapid increase in lithium carbonate prices." Chen Jia said.

Specifically, the main factors that force the price reduction of upstream lithium mines are the price war between downstream car companies and CATL's "lithium mine rebate" plan. In February this year, when the price of lithium carbonate was still over 400,000 yuan/ton, CATL was exposed to have launched a "lithium rebate" plan. The core terms are: in the next three years, the price of lithium carbonate for some power batteries will be settled at 200,000 yuan/ton. At the same time, car companies that sign this cooperation need to commit to giving about 80% of their battery purchases to CATL.

At that time, Chen Jia said in an interview with reporters: "On the surface, the lithium ore rebate plan signed by battery companies and car companies was due to the external factor of high and volatile lithium carbonate prices. In fact, it was caused by the price war in the downstream new energy vehicle market that spread to the upstream. In order to compete with Tesla and other brands in production under the price war, many car companies must further reduce the cost of a single vehicle."

In January this year, Tesla’s Model 3 and Model Y saw price cuts of up to 48,000 yuan, marking the first shot in this year’s car price war. In March, Hubei teamed up with a number of car companies to launch a car purchase subsidy of up to 90,000 yuan, pushing the price war in the auto industry to a climax. According to incomplete statistics, more than 40 car brands have joined this price war in different forms.

On March 30, Volvo officially announced that its S90, XC90, S60, XC60 and XC40 (fuel version) and other models will have car purchase subsidies, with a total amount expected to be as high as 200 million yuan. The activity period will be from April 1 to April 30, 2023.

In April this year, Geely officially launched a limited-time purchase event for exclusive models, providing a comprehensive subsidy of up to 45,000 yuan for more than 10 models including the Xingyue LHi·P. The event lasted from April 1 to April 30.

To this day, the price war in the automobile industry has not ended, and the need to further lower automobile production costs will not stop. In turn, the price reduction of upstream lithium resources will also provide "ammunition" for the price war in the automobile industry. Since there is a transmission time of several months from the price reduction of lithium resources to the reduction of manufacturing costs of automobile companies, if the automobile companies expect that the price of lithium resources will further decrease, they may increase their participation in the price war and form a "price reduction cycle" for lithium carbonate prices.

The fourth reason for price reduction: sodium batteries are on the way to "grabbing jobs"

From a deeper perspective, the plummeting price of lithium carbonate is also affected by the "substitution effect" triggered by technological advancements in the industrial chain. Sodium battery and semi-solid/solid-state battery technologies are now booming.

"Take sodium-ion batteries as an example. As early as when the price of lithium carbonate soared to 600,000 yuan/ton, the country launched a sodium battery replacement strategy from the perspective of resource security. All major domestic new energy battery manufacturers have basically made sufficient technical reserves for it. Preliminary estimates show that even if the price of sodium batteries drops to the 100,000 yuan/ton range, the cost of mature sodium batteries will be 30% to 40% lower than that of lithium batteries on average." Chen Jia said.

It is understood that sodium batteries and lithium batteries are both "rocking chair batteries". They are different from lithium batteries in the selection of positive electrode materials, negative electrode materials, electrolytes, etc. For example, the common form of sodium resources is salt, which is much cheaper than the "white petroleum" lithium carbonate that relies heavily on imports.

Compared with lithium batteries, the outstanding advantage of sodium batteries is low cost, but the disadvantage is insufficient energy density, which makes it difficult to effectively replace lithium batteries in the field of new energy vehicles. According to Caitong Securities research report, the energy density of sodium-ion batteries is generally between 100Wh/kg-150Wh/kg, and lithium-ion batteries can reach 150Wh/kg-250Wh/kg.

Qi Haishen, president of Beijing Teyi Sunshine New Energy Technology Co., Ltd., said in an interview with reporters that sodium batteries can replace lithium batteries in low-speed electric vehicles, communication base stations, electric bicycles, electric energy storage, solar street lights and other fields that have relatively low energy density requirements.

According to previous disclosures from companies such as CATL and Zhongke Haina, 2023 will officially become the first year of mass production of sodium batteries. Qidian Research CEO Li Zhenqiang believes that the development of sodium batteries is a national strategy and will help solve the problem of lithium resources being controlled by others. The cost advantage of sodium batteries will be reflected in 2-3 years. He said: "Sodium batteries are not a supplement to the lithium battery industry, but a substitute. They will benchmark lithium iron phosphate and lithium manganate batteries upwards and replace lead-acid batteries downwards. If the old forces of lithium batteries and lead-acid batteries do not go all out, they will be cut off by the new forces of sodium electricity."

Taken together, the emergence of sodium batteries will seize the market share of lithium batteries in many fields such as energy storage, thus affecting the demand and price of lithium carbonate. In the more distant future, the development of technical routes such as hydrogen fuel cells may also touch the "dominance" of lithium batteries.

How far will it fall? Disagreement over price "bottom line"

If the price drop of lithium carbonate is not caused by an isolated factor, but the result of the combined influence of multiple factors. So where is the bottom line of lithium carbonate price, and to what price will it drop?

In March this year, Li Xiang, founder, chairman and CEO of Li Auto, predicted that the price of lithium carbonate would be stable at 200,000-300,000 yuan per ton in the long term. NIO founder, chairman and CEO Li Bin predicts that the price of lithium carbonate is expected to drop to 200,000 yuan/ton in the fourth quarter. These two heads of new car-making forces are "conservatives" in predicting lithium carbonate prices.

There are even more "radical" ones. During the two sessions in early March, Li Liangbin, chairman of Ganfeng Lithium Industry, told the media: "The price of lithium salt was 600,000 yuan/ton yesterday, and it may be 100,000 yuan/ton tomorrow." At the recently held China Electric Vehicle 100 Forum (2023), Wang Yu, chairman of Funeng Technology, said that it is not impossible for the price of lithium carbonate to drop below 100,000 yuan per ton in the future.

So, where is the "breakeven line" for lithium mining companies? Lin Shi told reporters: "Based on the current mining costs, if the price of lithium carbonate is 100,000 yuan/ton, most companies will still make money. If it is less than 100,000 yuan/ton, they will lose money."

Zhang Xuefeng said: "The bottom line of lithium carbonate price is difficult to determine. Affected by various factors, the overall cost of the industry is about 150,000 yuan/ton, but the specific price must also consider market supply and demand and domestic and foreign policy environments."

However, the related costs of lithium carbonate may increase in the future, further raising the "break-even line". According to calculations by Huafu Securities, due to high energy prices, the increase in resource-end production capacity has led to an increase in related auxiliary materials and other expenses. It is assumed that the cost of salt lake lithium in 2024 will increase by 5% compared with 2022, the cost of lithium extraction from spodumene will increase by 10%, and the cost of lithium extraction from lepidolite will increase by 15%. Then when the price of lithium carbonate (tax included) drops to 240,000 yuan/ton, the Guoxuan Hi-Tech lepidolite project will stop production due to high production costs. When the price of lithium carbonate (tax included) drops to 100,000 yuan/ton, mica lithium extraction companies will cease production except for Yongxing Materials and Jiangxi Tungsten Industry.

According to GGII's forecast, based on the current price decline of lithium carbonate, the original market expected price to fall to 200,000 yuan/ton by the end of the year may arrive in the second quarter of this year.

However, Chen Jia believes that the price reduction of lithium carbonate is actually a "double-edged sword." Although it will reduce the costs of battery manufacturers and car companies, if this price collapse cannot be stopped in time, it will have an impact on the upgrading of China's new energy industry chain.

"Let's take sodium-ion batteries, a relatively mature technology alternative, as an example. Assuming that there is no major breakthrough in the production technology of sodium-ion batteries in the short term, once the price of lithium carbonate drops to the break-even point of 100,000 yuan/ton, the overall price of lithium batteries will be basically the same as that of sodium batteries. Some are extremely sensitive to market prices. Battery manufacturers will be faced with the dilemma of whether to continue to invest in sodium batteries. Our competitor Japan is continuing to develop similar technical solutions. Once China's new energy industry chain stops its rapid growth, it is likely to be overtaken by it in this field from 2030 to 2035," Chen Jia said.

Although China currently leads the world in lithium battery technology, Japanese and Korean companies have already made in-depth efforts in the field of "solid-state batteries" with higher energy density and representing the future development direction of the lithium battery industry. According to a research report from Huaan Securities, Japan is currently in a leading position in technology globally due to its earlier planning and layout of solid-state battery industrialization. South Korea's three major battery companies with leading technologies have also chosen to jointly develop solid-state batteries. Major European and American car companies are trying to gain technological reserves by investing in start-up companies such as Solid Power, Solid Energy Systems, Ionic Materials, and Quantum Scape, and seek to make a comeback in the field of solid-state batteries.

In order to maintain my country's dominant position in the new energy field, it is also necessary for the price fluctuations of the entire new energy vehicle industry chain to be more stable. Lin Shi said: "If the price of lithium ore drops particularly sharply, many lithium mining companies will stop working, which will lead to insufficient supply of lithium ore. Just like pork, the price will skyrocket and then plummet. What the new energy industry is most afraid of is the sudden rise and fall of raw material prices. In this case, what new energy vehicle companies want to see is the stability of lithium ore prices, not the cheaper the better."

"Taking comprehensive consideration of the current domestic production capacity balance and upstream and downstream market demand, a red line will be formed when the price of lithium carbonate enters the range of 100,000 yuan per ton. Once the red line is exceeded, it will cause a series of supply chain, industrial chain disorders and market chaos. At this moment, it is necessary for the regulatory authorities and the industrial chain to work together to jointly maintain the sustainable development of all ends of the new energy industry chain." Chen Jia said.