The payment circle has been particularly lively recently. Payment institutions have changed from usual and have spoken out, clearly stating that they will strictly implement Document No. 259 and implement "one machine, one code, one machine, one account".

It seems that the stubborn problem of code hopping and cashing out will be completely rectified. However, a reporter from Beijing Business Daily found that whether it is a street stall or a express delivery point, some agents have even opened stores to attract customers, teaching consumers how to use POS machines to cash out, and there are many ways to deal with the "one machine, one household" problem.

Payment institutions make "official announcements", agents make "detours", and a "cat-and-mouse game" is going on behind the scenes.

Newly opened POS terminal on the street

This is Wang Lin's (pseudonym) first attempt to open a store. Unlike other stores on the block, his store is neither a catering nor a retail store, but provides free gifts. While promoting POS machines to individual consumers, he also gives away gifts that come with the POS machines.

The store run by Wang Lin is a POS machine business hall. The word "free processing" is prominently displayed at the door. Various types of POS machines and code tags are placed in the glass window. In addition, a separate gift area is set up with dolls, cups, U-shaped pillows and other gifts.

Some consumers were attracted by the gift area and entered the store for consultation. Wang Lin was particularly enthusiastic. He told a Beijing Business Daily reporter that this store had just opened in early October. It can use POS machines for free to cash out, and can systematically match different surrounding merchants to avoid risks.

And this is also the way to make money according to Wang Lin. According to what he said, he has been a payment acquiring agent for several years, and this store also relied on the acquiring business. "You see how we make money? This month we have made more than 100 million in total, and there are more than 3,000 merchants in the background. As long as these merchants are swiping their cards and cashing out, we are making money every day, and what we earn is profit sharing. This year alone we have earned 300,000."

While giving a step-by-step introduction on how to use the POS machine to cash out, Wang Lin did not forget to sell it to customers, "If you don't have a POS machine, you can ask me to get one. The POS machine charges are high, so you can ask me to change it. If the POS machine jumps randomly and has credit card risk control, you can also ask me to change it. We also have stores here, which are reliable and safe. You can rest assured. The most important thing is that we always have after-sales service."

Wang Lin is not the only one who widely spreads the illegal cashing out of POS machines and treats it as his own career.

At a night market stall in Beijing, a stall offering "free credit cards and free POS machines" is particularly eye-catching. Along with the POS machines, there are also breakfast machines, egg steamers, woks and other gifts on display to individual consumers, attracting many consumers to stop. “This is what we do so that we can attract new customers.” Agent Wang Yue (pseudonym) told a Beijing Business Daily reporter.

In addition, there are POS machine agents who have "sneaked into" the Cainiao Station express delivery station in the community. On both sides and above the door to pick up the express delivery, they also boldly advertised that they can apply for free credit cards and receive free POS machines. When asked what the purpose is, they are also used to "cash out credit cards." They claim that the card will arrive in seconds, no deposit, and no tricks. They enthusiastically promote to individual consumers who come to pick up express delivery and introduce how to operate cash out and how to match surrounding merchants to avoid risk control.

Obtaining customers illegally through "one machine, one household"

In addition to illegal sales to individual consumers, another chaos is that the implementation of Document No. 259 of "one machine, one household" and "one machine, one code" has become a new marketing gimmick for agents to gain customers.

In the past, offline personal small and micro online POS machines provided by third-party payment companies often adopted the "one machine, multiple households" and "one machine, multiple codes" models. However, this was also accompanied by phenomena such as lax access to special merchants and prominent problems with fake merchants. Related business risks and hidden dangers were gradually exposed, and many POS machines even became tools used by black and gray industries to transfer funds. The issuance of Document No. 259 is precisely intended to comprehensively rectify this kind of chaos.

The so-called Document No. 259 is the "Notice on Strengthening the Management of Payment Acceptance Terminals and Related Businesses" issued by the People's Bank of China in 2021 (Yinfa [2021] No. 259). This policy strengthens the payment acceptance terminals in multiple dimensions. Business management and special merchant management clearly stipulate that one bank card acceptance terminal can only correspond to one acceptance terminal serial number, that is, "one machine, one code"; one bank card acceptance terminal can only correspond to one special merchant, that is, "one machine, one account."

However, despite the above-mentioned policies, the market has derived new "countermeasures". The acquiring market is still undercurrent, and there are many illegal businesses.

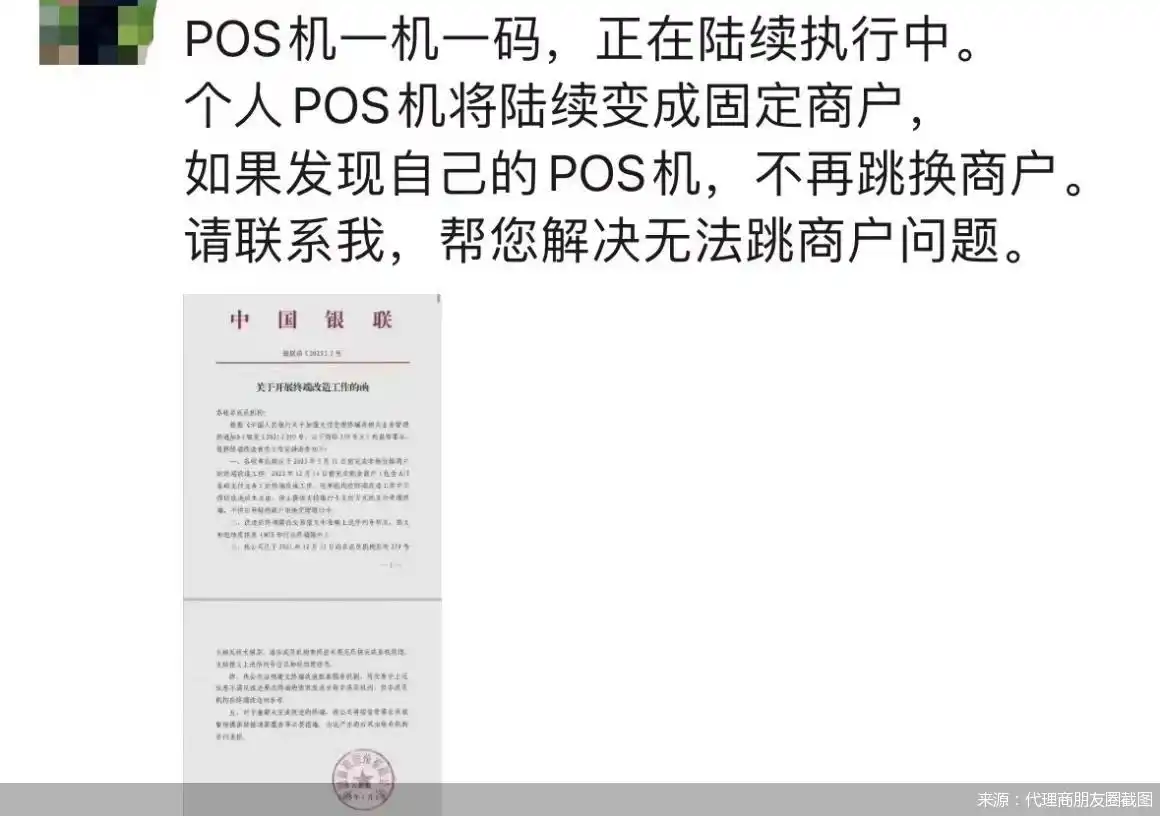

"One POS machine, one code, is being implemented one after another. Personal POS machines will gradually become fixed merchants. If you find that your POS machine no longer switches merchants, please contact me to help you solve the problem of being unable to jump to merchants." This is a marketing promotion that Wang Lin has released many times in his circle of friends.

A reporter from Beijing Business Daily asked Wang Lin for further information on the grounds of business consultation and learned that the corresponding measures he mentioned were to first replace new machines that have not yet implemented one machine, one code. "I can send you a POS machine with new products. New products change merchants every 4 hours."

According to reports, take the Shengfutong (Shanghai Shengfutong Electronic Payment Service Co., Ltd.) brand POS machine represented by Wang Lin as an example. The machine can be used for cashing out by scanning QR codes and cashing out with credit cards. The rate for scanning QR codes is 0.38%, while the rate for swiping credit cards is 0.6%. It can match different merchants in the surrounding area based on the cash amount and different addresses. So far, this model has not fully implemented "one machine, one code". Therefore, as long as the first transaction amount per day is greater than 7,000 yuan, the second transaction can start to jump to merchants, thereby supporting code jumping operations. When asked whether jumping the code to cash out would have adverse effects on individuals, he quickly explained, "The first payment of 7,000 yuan is stipulated by the payment company, so this operation will not cause risks."

When it comes to code hopping, Wang Lin further said, "Merchant is constantly changing. The bank will think that you are really spending money and recognize your high consumption level, so it will increase your credit limit and maintain the card. But in fact, all the money goes to your own account." In the "Credit Card Swiping Standards" he provided, each time period in the morning, noon and evening corresponds to different consumption scenarios, and there are also strict regulations on the time, amount, and number of credit card swiping. As for the risks, he didn't pay too much attention. "The policy will only become looser and looser, and after this period of time, it will probably be restored again."

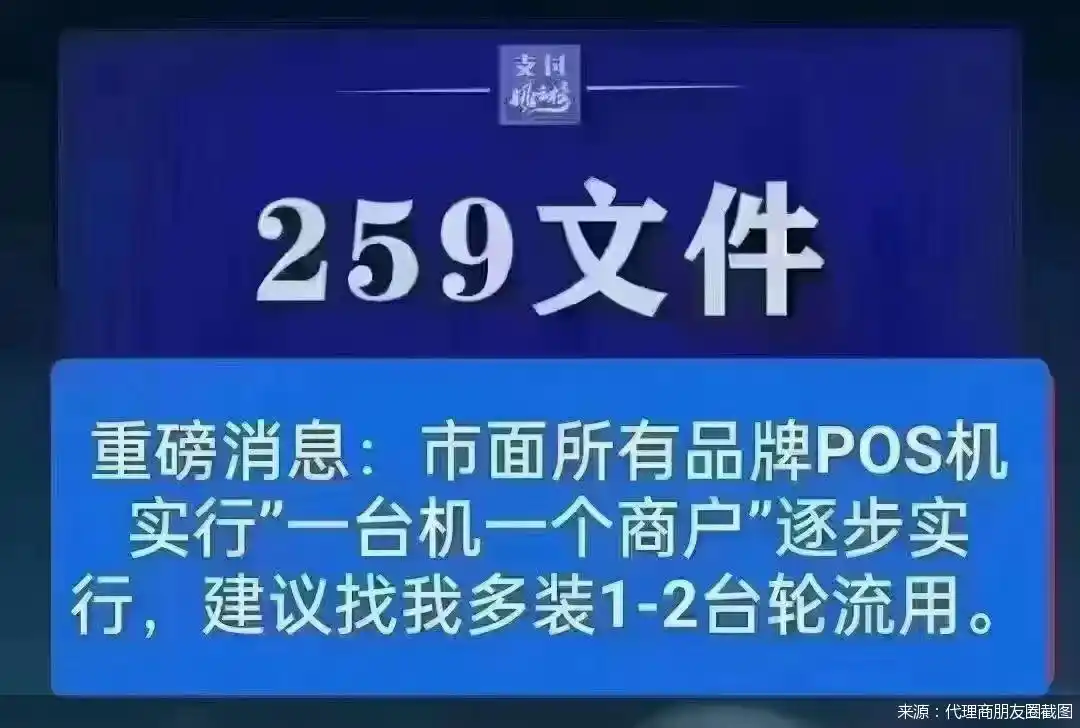

In addition to Wang Lin, another POS machine agent setting up a stall also shouted in the circle of friends, "The market's POS machines are gradually implemented as 'one machine for one merchant'. It is recommended that you ask me to install 1-2 more machines and use them in turn." She revealed to a reporter from Beijing Business Daily that she has acted as an agent for several POS products such as Zhongfu, Dianbank, and Hedabao, and currently supports jumping to multiple merchants when swiping a card. "Even if the policy comes out, banks and payment companies cannot prevent everyone from using it, and they are all trying to find ways."

The method described by the agent is a self-developed technology of her company. According to the introduction, her company is an aggregation service platform for the national acquiring industry, with its headquarters located in Beijing. After the implementation of the "one machine, one code" policy, the company has a self-developed technology that allows users to manually add 15 merchants on the POS machine, and then switch merchants when swiping their cards to achieve code hopping operations.

In addition to replacing new machines and installing more machines, mobile online POS has also become a channel for many agents to "take advantage of loopholes". According to the "solutions" provided by many other POS agents, the main thing is to download the "Kaiyuntong" App. After successful registration, you can also use UnionPay Cloud QuickPass to scan the code, and the rate is 0.38%. It is said that "each transaction will be transferred to the merchant and will not be affected, and can be used for personal cash out." However, this method can only swipe your own credit card, and other people will not be able to scan the code in seconds.

In addition, another POS machine marketer recommended the mobile POS "Quick Payment App" to reporters and also said that "you can jump to merchants normally and are not affected by the one-machine-one-code policy for the time being." A Beijing Business Daily reporter discovered that "Kaiyuntong" is a product of Kaidianbao, while the developer of "Quick Payment" is Shanghai Hanyin Information Technology Co., Ltd., a payment institution that focuses on mobile payments and Internet payments.

In response to the situations mentioned by many of the aforementioned agents, reporters from Beijing Business Daily interviewed Shengfutong, China Pay, Electronic Banking, Helibao, Kaidianbao, Hanyin Technology and other companies for verification. As of the time of publication, no response from the latter had been received.

What is the difficulty in implementing “one machine, one household”?

According to the "Letter on Carrying out Terminal Transformation Work" officially issued by China UnionPay at the beginning of this year, each acquiring agency should complete the terminal transformation work for non-standard price merchants before May 31, 2023, and complete the terminal transformation work for the remaining merchants before December 14, 2023.

The deadline is approaching. In this rectification of "one machine, one code" and "one machine, one household", in addition to agents, acquiring and payment institutions play an important role.

Just recently, many payment institutions, including Lakala (300773), Jialian Payment, Helibao, Leshu Payment, etc., have strictly standardized their business development requirements and fully implemented "one machine, one code".

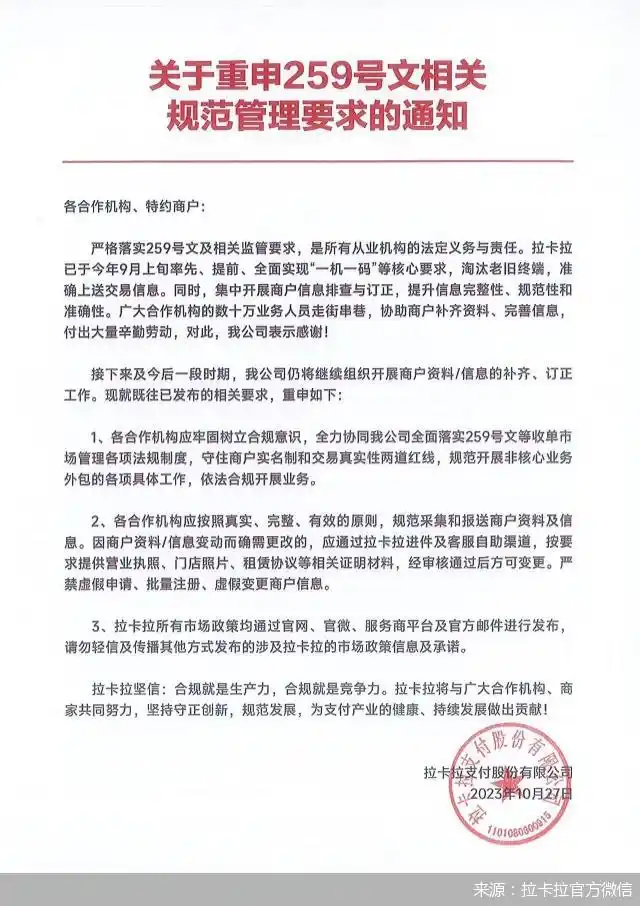

Judging from the "Notice on Reaffirming the Relevant Standards and Management Requirements of Document No. 259" recently issued by Lakala, the notice states that strict implementation of Document No. 259 and related regulatory requirements is the legal obligation and responsibility of all practitioners. Lakala has taken the lead in early September this year to fully realize the core requirements of "one machine, one code" in advance, eliminate old terminals, and accurately submit transaction information. At the same time, we will focus on checking and correcting merchant information to improve the completeness, standardization and accuracy of information. In the future, the company will continue to organize the completion and correction of merchant information/information.

Coincidentally, Helibao also issued a notice stating that "the company has fully completed the implementation of the relevant requirements of Document No. 259, that is, fully realizing the core requirements of 'one machine, one code' and accurately submitting transaction information." It also requires all service providers to collect and submit merchant data and information in a standardized manner on the premise of complying with laws and regulations.

In addition, the relevant person in charge of Jialian Payment responded to a Beijing Business Daily reporter that the current merchant registration rate and core element upload rate have reached 100%, and core requirements such as "one machine, one code" have been fully implemented, and the terminal serial number and geographical location information are accurately uploaded. In the future, we will continue to conduct merchant information investigation work to improve the completeness, standardization and accuracy of merchant information to ensure that the transformation work related to Document No. 259 is fully completed as scheduled.

However, not long after Lakala’s official announcement, on October 31, a Beijing Business Daily reporter received a “pickup notice” message in his QQ mailbox, claiming that “your repayment behavior in 2023 exceeds expectations, and I will send you a UnionPay certified card swiping machine as a gift. Please Check it as soon as possible.” Judging from the details, the product to be shipped is called “Mobile Intelligent Credit Increase Artifact” and is a Lakala UnionPay-certified POS machine. The rate is as low as 0.38%. It supports WeChat/Alipay/UnionPay/Cloud QuickPass, etc., and it will arrive in your account very quickly and will be shipped immediately upon receipt. The content of the email also states that the machine is only available for credit card users to apply for free.

In response to the online sales of POS machines to individual users, a reporter from Beijing Business Daily further sought confirmation from Lakala, who said, "After investigation, it was not our company's behavior. And our company has always required partners to strictly abide by relevant national laws, regulations and regulatory regulations, and conduct business in compliance with laws and regulations." To ensure the authenticity of merchants, it is strictly prohibited to sell bank card acceptance terminals, barcode payment acceptance terminals, collection codes and other products with payment functions through telephone, Internet and other media. Any illegal activities in the name of our company will be reported to the competent authorities."

On the one hand, there are repeated orders from institutions to regulate the exhibition industry, but on the other hand, there are "loopholes" in the actual exhibition industry. It is not difficult to see that the intricate outsourcing relationships behind the acquiring industry, the difficulty of monitoring and management of huge quantities, and entangled interests are still hindering the eradication of the chaos in the acquiring market.

As Su Xiaorui, a senior consultant in the financial industry analyzed by Analysys, said, "Despite the multi-faceted containment by institutions, chaos still occurs. There are two main factors. From the perspective of POS machine agents, they hope to continue to use code hopping and other means to attract groups who use POS machines to cash out or collect points; from the perspective of acquirers, their poor management and control also led to this situation."

The deeper layer behind this is the conflict between market interests and compliance. According to Wang Pengbo, chief analyst at Broadcom Consulting, the fundamental reason for this situation is that the market "demand" for cash out still exists in a short period of time. There are many merchants and fierce market competition. During the process of inventory transformation, agents affiliated to various acquiring agencies may also cause certain confusion due to conflicts of interest.

"In addition, in the management of outsourced service providers at all levels, payment institutions play more of a channel role. However, outsourced service providers have a large number of merchants and complex interest relationships, which poses certain difficulties to merchant management." Wang Pengbo said frankly.

The large number of POS machine agents and their geographical dispersion have also become a management difficulty for payment institutions. The above-mentioned person in charge of Jialian Payment also pointed out the difficulties in details: During the merchant information investigation process, due to the characteristics of large number, wide range and lack of concentration of merchants, it requires a lot of manpower. Currently, during the terminal transformation process, some old terminals need to be replaced. In addition, the terminal program uses third-party companies such as AutoNavi and Baidu to convert the base station information into longitude and latitude. However, the conversion rate of the base stations by the third-party companies cannot reach 100%, so there is a certain probability that a small number of transactions will fail to upload the longitude and latitude. The upgrade needs to be completed as soon as possible without affecting the merchant's normal cashier operations.

In Wang Pengbo’s view, in order to eradicate the problems existing in the implementation of “one machine, one household”, the follow-up core lies in the entanglement in the distribution of interests between outsourcing agents and merchants; the second is that it will take some time for the market to digest the policy; in addition, it is necessary to insist on reclassifying the management of outsourcing agents, setting up entry barriers, and compliance also requires continuous supervision and promotion.

How will the “cat-and-mouse game” end?

Looking back at the symbiotic relationship between payment institutions and agents over the years, in offline acquiring, payment institutions and outsourcing agents have always been called "symbiotic interests" in the industry. On the one hand, agents work hard to promote products for payment institutions and "contribute their efforts" to the latter's business development; but on the other hand, there are also agents who go astray in pursuit of profits, causing many payment institutions to "consecutively receive fines."

On October 30, the administrative penalty information released by the Tianjin Branch of the People's Bank of China showed that Zhonghui Electronic Payment Co., Ltd. was severely punished for three violations of laws and regulations, including failure to handle fund settlement for special merchants as required, failure to implement the real-name management of special merchants as required, and failure to set up an acquiring bank settlement account as required. The People's Bank of China issued a warning, confiscated illegal gains of 13.2811 million yuan, and fined 67.6255 million yuan.

Although in recent years, supervision has heavily rectified the acquiring business and huge payment fines have appeared frequently… Judging from the aforementioned market chaos, the current implementation of "one machine, one account" and the rectification of cash-out code hopping are still in a "cat-and-mouse game".

In addition to night market stalls, express delivery outlets, and business stores, there are also many outsourcing service providers that use personal WeChat, group mailboxes, sweeps of buildings, hospitals, and even supervisory sites to market POS machines to many individual consumers on the pretext of cashing out credit cards. In addition to improper marketing and lax risk control by merchants, the latter even subcontracted to seek profits.

According to many industry insiders, POS machine cash-out violations have repeatedly occurred, agents continue to operate illegally, and payment institutions are also responsible.

As Su Xiaorui pointed out, payment institutions should not take any chances. They need to implement the new regulations in a down-to-earth manner, check for and fill in the shortcomings in the previous acquiring field, and at the same time strictly enforce merchant access conditions, use technology to strengthen the payment protection network, strengthen daily inspections of merchants, and plug code hopping loopholes from the source.

At the regulatory level, in September this year, the People's Bank of China held a meeting to strengthen the management of payment acceptance terminals and related businesses and also emphasized that it will continue to promote the transformation of acceptance terminals, verification of merchant information, improvement of transaction messages, and optimization of transaction monitoring. Various measures are also further promoting the implementation of Document No. 259.

"The attitude of supervision has been very clear. It is the overall trend of the bank card acquiring industry to reduce illegal and gray businesses." Wang Pengbo mentioned that as the cost of cashing out increases in the future, users who cash out may slowly lose, and the cashing out market may shrink. After the regulatory transition period, returning to real merchants and providing enterprise digital services will be the future direction of transformation for acquirers.

Looking forward to the future, on the one hand, the effective regulation of cooperative agents will become a key task for each payment institution to implement policies. In addition, how to collect and verify merchant information and how to establish a platform to conduct risk monitoring of their business have become the key "keys" to promote compliance.

Some payment institutions are already exploring new ways out under strict supervision. "The red line of supervision is becoming more and more stringent, and our corresponding business must gradually shrink, mainly transforming to digital business, and restarting the company's second growth curve." An employee of a payment company in East China revealed that the company has now shifted its overall strategic focus to industrial digital payment services, and has already carried out digital transformation and upgrading of corresponding technology and operations very early. The follow-up focus will be on exploring the empowerment of B-side through payment digitization.

Beijing Business Daily reporter Liu Sihong and Dong Hanxuan

As a member of Linghexun Plus, you can watch more exclusive content for free: 8 major financial columns, exclusive market interpretations of the latest and hottest information, and quickly grasp the market investment trends.