"Selected summary: The index has rebounded from the previous week to 80.83%, which is also the first rebound in the past two months. 4. ETF product performance: From January 13, 2025 to January 17, 2025, the market fluctuated and rose. "

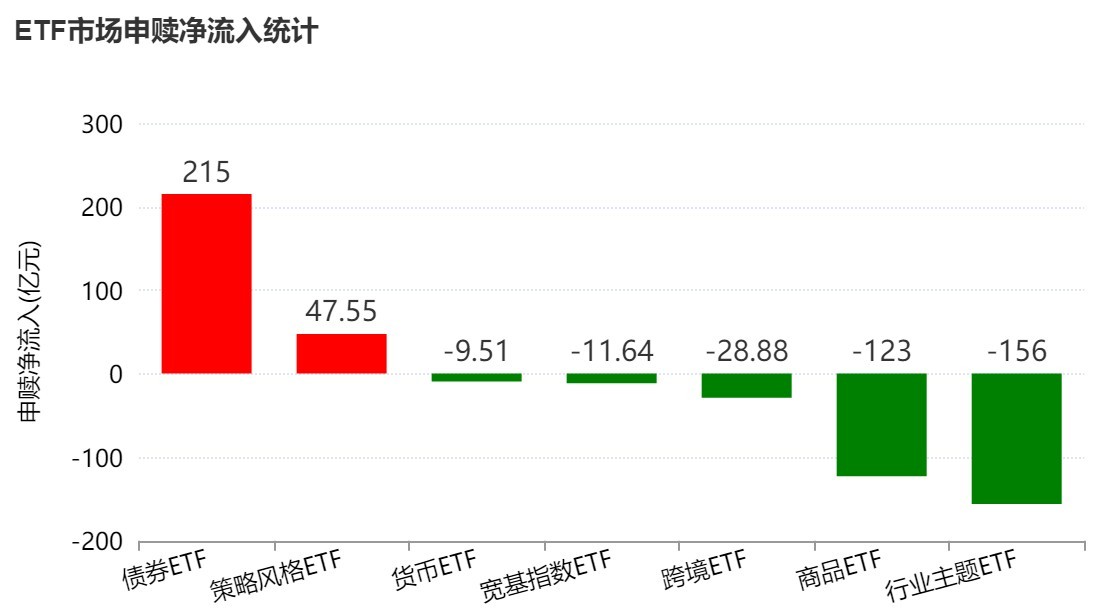

1. Core conclusions 1. Overview of hot topics: 1. Capital sentiment turned positive, with A-share products obviously being bought back. The capital inflow of CSI 300 products once again led the broad-based products. Funds have increased allocations to CSI A500 products for fourteen consecutive weeks, but the intensity has become smaller. In terms of industry themes, dividends from Hong Kong stocks have been increased, and capital outflows from non-bank products top the list.

2. 2. In terms of product performance, the performance of cross-border products was divided. Cross-border ETFs such as S&P Oil & Gas, Nikkei, Asia Pacific Select, Germany, and France led the gains. Many cross-border targets showed large premiums. Products such as S&P Consumer and Southeast Asia Technology were among the top decliners.

3. 3. Last week, 15 products were applied for, and the first batch of 12 Science and Technology Innovation Composite Index ETFs received intensive applications.

4. 2. Ranking of ETF manager scale: China Asset Management and E Fund still occupy the top two in non-cargo ETF management scale; in terms of broad-based ETFs, China Asset Management ranks first, with a management scale of 505.606 billion yuan; in terms of industry ETFs, China Asset Management and E Fund occupy the top two, with management scales of 115.993 billion yuan and 102.626 billion yuan respectively.

5. 3. Concentration ratio of managers: After the second quarter of 2023, the concentration ratio of top ETF managers has shown an overall upward trend, and has continued to fall from a high level after October 2024. As of January 17, 2025, the concentration ratio of the top 10 managers has rebounded from the previous week to 80.83%, which is also the first rebound in the past two months.

6. 4. ETF product performance: From January 13, 2025 to January 17, 2025, the market fluctuated upward, with the Shanghai Composite Index rising by 2.31%; the performance of cross-border products was divided, with S&P Oil & Gas, Nikkei, Asia Pacific Select, and Deutsche Cross-border ETFs such as China and France led the gains, and many cross-border targets saw large premiums. Products such as S&P Consumer and Southeast Asian Technology were among the top losers. In addition, technology growth sectors such as financial technology, GEM artificial intelligence, and software were also relatively active.

7. 5. Larger-scale ETF products: The total size of ETFs in the market is currently 3.70 trillion yuan, of which 5 have exceeded the 100 billion yuan mark, and the number is the same as last week, including Huatai-Berry CSI 300 ETF (510300), Yifang CSI 300 ETF (510310) and ChinaAMC 300 ETF (510330) occupy the top three in the market, with product scales of 354.509 billion yuan, 241.804 billion yuan, and 161.078 billion yuan respectively.

8. In addition, the product scale of Harvest 300 and Huaxia 50 both exceeds 100 billion yuan.

9. 6. Fund sentiment has turned positive, with A-share products obviously being bought back. The capital inflow of CSI 300 products once again led the broad-based products. Funds have increased their allocation to CSI A500 products for fourteen consecutive weeks, but the intensity has become smaller; in terms of industry themes, Hong Kong stocks Dividends have been increased, and non-bank product capital outflows top the list: Observing the sector capital flows in the past week, we can see that in terms of major asset classes, capital sentiment was relatively positive last week, with a large inflow of 9.4 billion yuan in A-share products. The top commodity inflow last week There has been a significant outflow of currency and bond products; among A-share broad-based products, funds have increased their allocation to CSI A500 products for fourteen consecutive weeks, but the intensity has become smaller, with another inflow of 1.2 billion yuan, and the recent cumulative inflow has exceeded 220 billion yuan; CSI 300, CSI 1 000, CSI 500, GEM Index, Science and Technology Innovation 50 and other broad-based product funds have all flowed back, of which the Shanghai and Shenzhen 300 has the largest inflow, reaching 4.9 billion yuan; in terms of industry themes, Hong Kong stock dividends have been increased, and non-bank product capital outflows top the list.

10. 7. Weekly ETF product declaration status: 15 products were declared last week.

11. Among them, 12 companies including China Universal and Bosera have applied for the Science and Technology Innovation Composite Index ETF, Wanjia Fund has applied for the National Securities Aerospace Industry ETF, Bosera Fund has applied for the CSI A100 ETF, and Xinhua Fund has applied for the CSI A50 ETF.