Drawing red envelopes, applying for loans, recruiting partners… Nowadays, private banks that lack offline branches are also racking their brains and constantly using tricks to attract new customers and enhance user stickiness. On May 31, WeBank’s wild cash red envelopes attracted attention: According to the rules of the event, users only need to follow the WeBank official account and if their total assets at the end of the day on May 29 are greater than 1,000 yuan, they can participate in a cash red envelope lottery of up to 516 yuan. A reporter from Beijing Business Daily noticed that marketing activities similar to those of WeBank are not uncommon. They currently include Xinwang Bank, Suning Bank and other institutions, which have recently launched activities such as "recruiting partners" and "upgrading loan grouping". From the perspective of the industry, fancy ways of attracting new customers reflect the Internet traffic anxiety and operating bottlenecks of many private banks. However, how to clarify marketing boundaries and control the risks of attracting new customers is also a question that many private banks need to think about.

Fancy new promotions

On May 31, WeBank’s official WeChat released news about the “Financial Management Carnival and Red Packet Rain” event, claiming that “100% prizes will be given, up to 516 yuan.” Judging from the specific operating rules, users need to pay attention to the WeBank official account. If the total assets at the end of the day on May 29 are greater than 1,000 yuan, they can click on the bank's WeChat official account to participate in the lottery on May 31.

On June 1, a reporter from Beijing Business Daily tried to experience the event. After clicking to follow, the page displayed "This event has ended." However, the reporter noticed that such marketing activities of WeBank are not uncommon. In addition to the red envelope activities, WeBank has also launched a number of wool benefits such as "earning phone bills" and "receiving 60 yuan". Among them, "earning phone bills" can be participated in by purchasing financial products. The qualification to participate is only for users who have never bought a current deposit+. "Receive 60 yuan" requires users to repay the bound credit card through WeBank Card/current deposit+, and only the first credit card repayment will be rewarded every month.

In response to this activity, the relevant person in charge of WeBank said in an interview with a Beijing Business Daily reporter, "This activity is mainly to give back to our bank's loyal customers, invite loyal customers to experience our bank's new products and use our bank's new functions, and establish stronger connections with customers."

However, because the qualifications to participate in some activities are only open to new users, WeBank marketing is also regarded by industry insiders as a need to attract new users. Although it helps to increase business traffic, this type of customer acquisition method also pushes up the bank's operating costs, which will inevitably lead to the phenomenon of users "grabbing wool".

In this regard, the relevant person in charge of WeBank added, "The delivery channels of our activities are all through our own App and mini-program channels, and are not released to the outside world, so it does not involve external new acquisitions. Since the customers are all known customers of our bank, it does not involve 'wool'. We do not agree with the method of acquiring new customers regardless of cost, and we do not agree with the use of 'wool' to activate customers."

In fact, not only WeBank, but also Beijing Business Daily reporters noticed that Xinwang Bank, Suning Bank, etc. have launched various marketing activities to attract new customers and promote activity.

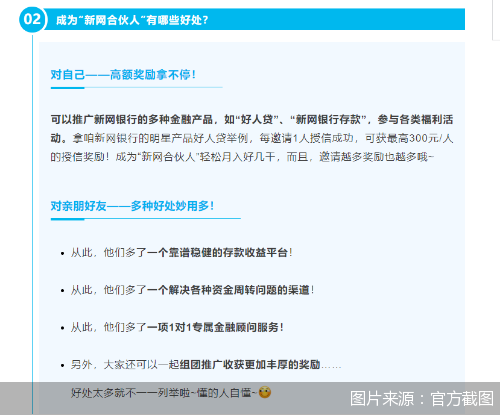

Recently, Xinwang Bank has been recruiting "Xinwang Partners". Applying for "Partner" can promote Xinwang Bank's various financial products, such as "Haoren Loan", "Xinwang Bank Deposit", etc. It is said that "every time you invite a friend and successfully apply for credit Haoren Loan, you can earn up to 300 yuan."

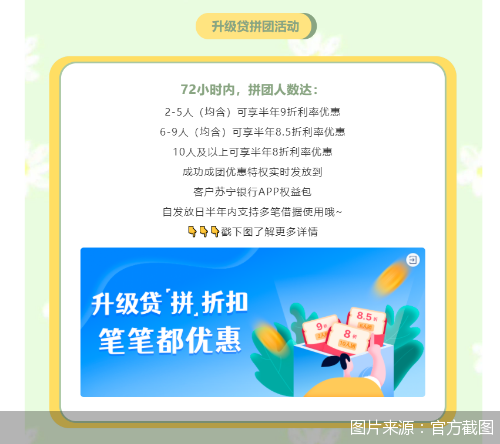

In addition, Suning Bank has also launched an upgraded group loan activity. Within 72 hours, group members with 2-5 people can enjoy a half-year 10% interest rate discount, 6-9 people can enjoy a half-year 15% interest rate discount, and 10 or more people can enjoy a half-year 20% interest rate discount. Multiple IOUs can be used within half a year from the issuance date.

In response to various issues such as the transformation of the effectiveness of relevant marketing activities and risk control, reporters from Beijing Business Daily conducted interviews with Xinwang Bank and Suning Bank, but did not receive a response from the latter as of press time.

Increase operating costs in disguised form

Constrained by the restrictions on offline outlets, private banks have come up with new ideas and launched customer marketing wars. According to industry insiders, this move is mainly to acquire customers, attract deposits, and enhance the brand awareness of the institution.

As Zhou Maohua, an analyst at the financial markets department of China Everbright Bank (601818, Stock Bar), pointed out, for banks, this type of marketing can help enhance bank brand awareness and increase business flow, but at the same time, it should be noted that the customer stability brought by these various marketing methods is not necessarily good, and it also pushes up bank operating costs to a certain extent. Banks may transfer liability costs to the asset side, further pushing up the financing costs of small and micro and private enterprises.

"Due to network restrictions, private banks rely more on online channels to acquire new users and promote products. Especially after regulatory policies stipulate that deposits and financial management products cannot be sold through Internet platforms, the necessity for private banks to carry out marketing activities through their own channels has further increased." Yu Baicheng, president of Lingyi Research Institute, told the Beijing Business Daily reporter that lottery draws, cash rebates, group purchases, and partner promotions are conventional marketing methods to acquire customers and increase activity. Not only private banks, but also other banks and Internet companies have used them.

However, it should be noted that many private banks have encountered many hiccups in their exploration of attracting new customers. For example, Suning Bank has previously promoted the upgrading loan partner game, but industry insiders bluntly stated that this online new model has multiple marketing risks. In addition, many local banks have launched a "Pinduoduo" type group loan marketing model, and this type of marketing model has also attracted regulatory attention.

From the perspective of the industry, through the means of partners, fission-type recruitment can be quickly carried out, but this model also hides multiple marketing risks.

Zhou Maohua said that the potential risks of this type of marketing method are: first, it will lead to an increase in the bank's operating costs; second, there may be induced lending, pushing up residents' debt leverage, which is not conducive to protecting the legitimate rights and interests of consumers; third, this method of customer acquisition may weaken the bank's risk control effect, which is not conducive to the bank's stable operation.

Banks themselves are operating risk institutions, and risk control is their lifeline. Zhou Maohua said that institutions need to pay attention to whether these marketing methods lead to a reduction in risk control requirements, whether they affect the institution's sound and sustainable operations, whether they significantly increase the operating costs of financial institutions, etc. Institutions need to remain in awe of financial risks and regulatory systems, and the bottom line is to prevent local systemic risks from occurring.

Su Xiaorui, a senior observer in the banking industry, also said that on the one hand, institutions' recruitment activities are to develop new users and obtain business scale growth, and on the other hand, they are also to resist fierce external market competition, enhance brand awareness, and consolidate their industry position. However, institutions need to pay attention to the fact that financial marketing promotions need to comply with relevant regulatory norms. In addition, the choice of relying on self-owned channels or external third-party channels is also worthy of further consideration.

Be wary of multiple red lines

Recently, a reporter from the Beijing Business Daily learned from a bank practitioner that on the one hand, banks cannot absorb deposits through non-self-operated channels. In addition, they also face many constraints in cooperation with Internet companies on the loan side. Under the multiple impacts of limited scale, single qualifications, geographical restrictions, etc., small and medium-sized banks have increasingly smaller development space and increasing operating pressure.

It has to be said that there is indeed a certain pressure on private banks at present, mainly due to fierce competition among domestic peers and changes in the domestic regulatory environment. Private banks' liabilities and operating pressure have increased. However, Zhou Maohua also pointed out that it is also important to note that private banks are small in scale, have no corresponding outlets, and have low operating costs; market-oriented operating mechanisms and services, high awareness, and high operating efficiency during the period; clear domestic equity structures, flexible incentive mechanisms, and relatively active innovation; at the same time, the domestic economy is gradually getting rid of the impact of the epidemic, and support policies are not making sharp turns. The economy and corporate operations are steadily recovering, the vitality of micro entities is gradually released, and the operating prospects of private banks are gradually improving.

"For us, it is more about maintaining insights into the industry or customers and responding quickly. This is also the starting point for maintaining our survival soil or moat." said the aforementioned bank practitioner.

However, as the cost of online marketing continues to rise, banks, as financial institutions that need to operate stably, must also consider more issues in marketing. When it comes to marketing red lines, Yu Baicheng told a reporter from Beijing Business Daily that banks should first consider the business conversion rate of investment and not invest too much to affect the financial situation. The discount rate should also be reasonable and not over-subsidize; second, banks should pay attention to marketing compliance and consider marketing plans. The adaptability and rationality of the product should be recommended to the right people, and promotion should not be exaggerated. Pay attention to the supervision of partner behavior in partner marketing; third, pay attention to the risks of Internet marketing, do a good job in product and risk control of activities, and be careful of being ripped off by professional groups.

Regarding the subsequent development of private banks, Su Xiaorui suggested that licensed financial institutions need to establish and improve internal control systems for financial marketing and publicity, strengthen behavioral supervision of business partners, and improve customer service mechanisms related to the protection of financial consumers' rights and interests.

Beijing Business Daily reporter Yue Pinyu Liu Sihong