"Low-interest loan, approved instantly, no mortgage required, monthly interest rate 0.8%"…

Online loan advertisements can be seen everywhere, but the temptation of low-interest online loans may actually be a high-interest trap. Some lending institutions only advertise a monthly interest rate of 0.8%, but fail to mention that borrowers also have to pay numerous channel service fees, guarantee fees, and even mandatory bundled account insurance premiums.

The good news is that regulation is cracking down on high-interest online loans. On March 15, the State Administration of Financial Supervision and the People's Bank of China announced the official release of the "Regulations on Expressed Comprehensive Financing Costs for Personal Loan Business" (hereinafter referred to as the "Regulations"), which will come into effect on August 1, 2026. At the same time, many well-known loan assistance institutions were interviewed by the State Financial Supervision and Administration Bureau.

The online lending industry is ushering in the “strongest supervision”.

The online lending industry is ushering in institutional changes

Online loans, simply put, are borrowing money through mobile apps or websites. Compared with bank loans, online loans have lower thresholds, faster procedures and no mortgage required, but the interest rates are usually higher and the impact on credit inquiry records is more frequent.

At present, the mainstream model of online lending is a loan assistance model led by licensed financial institutions (such as consumer finance companies, online small loans) and Internet platforms – the platform uses traffic and technological advantages to be responsible for customer acquisition and risk control assistance, and licensed institutions such as banks provide funds and bear core credit risks.

However, while providing financing convenience, the online lending industry still faces high pressure from complaints due to continued chaos. The "Notice on Financial Consumption Complaints in 2025" released by the State Administration of Financial Supervision and Administration shows that the number of complaints related to online loans nationwide in 2025 will reach 1.236 million, of which complaints about collection of private numbers accounted for 68.7%, and complaints about high interest rates and cut-off interest accounted for 21.3%, becoming the two most prominent chaos.

Faced with long-standing industry problems, regulatory authorities took action.

The "Regulations" that came into effect on August 1 this year will implement a "comprehensive financing cost explicit system." The key point is that institutions must fully disclose the interest fee structure and charging standards, and uniformly disclose the annualized comprehensive costs; at the same time, it is strictly prohibited to charge any additional loan-related interest fees beyond the express items. This means that supervision has more detailed requirements for the front-end marketing and interest fee disclosure of the online lending industry.

This directly refers to the "split charging" routine of some online loans. China News Weekly searched for "decapitation interest" (interest deducted from the principal in advance) on the Black Cat complaint platform. The number of related complaints was nearly 219,000, and the total number of complaints related to "routine loans" reached 77,000.

After sorting through the complaints, China News Weekly found that the interest rate calculation systems of many online loan-related products are complex, making it difficult for ordinary users to accurately calculate the cost when borrowing, and often only notice abnormalities during the repayment process. For example, some lending institutions only advertise a monthly interest rate of 0.8%, but do not mention that in addition to this interest, borrowers also have to pay so-called channel service fees of 2% to 5%, a guarantee fee of 0.3%, and even mandatory bundled account insurance premiums.

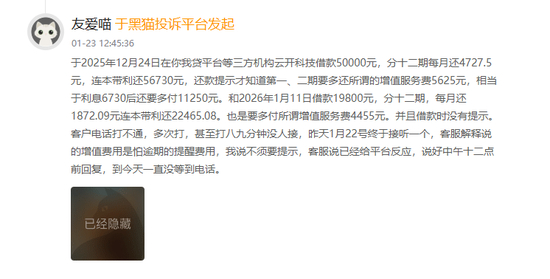

There were complaints on the Black Cat platform that users borrowed 50,000 yuan and 19,800 yuan from a certain platform respectively, and when they repaid the loans in 12 installments, they discovered that the platform had charged an additional high "value-added service fee" without notifying them in advance (a loan of 50,000 yuan was overcharged by 11,250 yuan, a loan of 19,800 yuan was overcharged by 4,455 yuan). If the complaint details are true, the combined annualized cost of the two transactions exceeds 40% when the charges are bundled.

The promulgation of the "Regulations" will effectively curb various illegal activities such as hidden charges, splitting of interest and fees, and disguised hikes in interest rates in the online lending industry at the institutional level.

Wang Pengbo, chief analyst of Broadcom Consulting, explained to China News Weekly that the "Regulations" introduced this time aim to build a full-chain supervision system. The "Regulations" require online loans to use "pop-up windows + mandatory reading + confirmation" and offline "signature confirmation" express forms. This is a very important step. It can force institutions to reduce the problem of consumers handling loans without knowing and being charged extra fees from the processing link, and strengthen financial consumers' right to know and independent decision-making.

This undoubtedly shattered the "calculations" of some online lending companies.

A person in the loan assistance industry told China News Weekly that in the past, credit enhancement service fees and guarantee fees were often collected separately by cooperative institutions and were not included in the public interest rates. They have long been a relatively hidden charging method in the industry, but this supervision has clearly blocked this path.

Profit margins have been significantly compressed

In fact, since 2025, regulatory authorities have continuously strengthened their efforts to rectify high-interest loan assistance businesses. Especially since the implementation of the "Notice on Strengthening the Management of Internet Loan Assistance Business of Commercial Banks to Improve the Quality and Efficiency of Financial Services" (referred to as the "New Loan Assistance Regulations") in October 2025, the industry has undergone fundamental changes.

China News Weekly combed through the business models disclosed in the past financial reports of leading loan assistance platforms and found that loan assistance companies in the past mainly used a business model of loan assistance and self-operated lending in parallel – under the joint loan model, its licensed institutions and banks jointly contribute capital and share risks; the self-operated model obtains interest income through the issuance of on-balance sheet loans with its own and borrowed funds.

However, the "New Loan Assistance Regulations" clearly require banks to conduct independent risk control, prohibit loan assistance institutions from taking full responsibility for repayment, and comprehensively regulate the upper limit of comprehensive financing costs.

Under the new regulations, "whoever lends money is responsible" and banks must conduct independent risk control. At the same time, loan-assisted platforms’ evasive behavior is prohibited, and the upper limit of comprehensive financing costs is fully regulated. This makes the past "low interest, high service fee" online loan routine completely out of order, and the actual burden of the borrower is locked within a reasonable range.

More importantly, according to this requirement, the annual interest rate corresponding to the comprehensive financing cost of the loan assistance business (loan interest + credit enhancement service fee + loan-related service fee) will not exceed 24%. High-interest customers with interest rates higher than 24% are precisely a very important source of profit for the platform.

Ji Shaofeng, an expert in the field of small and micro finance, analyzed China News Weekly. It is estimated that the capital cost of most consumer finance and loan assistance platforms is 3% to 5%, the traffic cost is 4% to 5%, the risk cost is 7% to 9%, and the operating cost is 4% to 6%. At an annualized interest rate of 24%, the profit margin is very limited.

Ji Shaofeng further pointed out that from the perspective of industry structure, among the current online loan balance of about 5 trillion yuan, the 24%-36% high interest rate range is about 800 billion yuan, accounting for 16%, and is mainly concentrated in the middle waist and below platforms. These high-interest businesses now have only two options: adjust to meet compliance standards or withdraw from the market.

"This means that under the new loan assistance regulations, the business model of mid-level loan assistance institutions that rely on underwriting, joint lending, and capital-heavy profit sharing is rapidly collapsing. A large number of them will exit within a year, and financing guarantee companies will be liquidated in batches." Ji Shaofeng pointed out.

Another loan assistance company insider revealed to China News Weekly that since the implementation of the new regulations in August, high-interest loan assistance business with annualized interest rates exceeding 24% has completely disappeared. Previously, the interest rate ceiling generally implemented in the industry was 36%, and profit margins have been significantly compressed. "Not only is profit margins compressed, but some products require compliance transformation, which directly leads to general pressure on industry performance in the fourth quarter of 2025."

Looking at the leading companies in the loan assistance industry listed on the US stock market, the operating pain of the loan assistance industry is very obvious.

Qifu Technology's fourth quarter financial report for 2025 shows that the current revenue was 4.093 billion yuan, a year-on-year decrease of 8.7%, and the net profit was 1.016 billion yuan, a year-on-year decrease of 46.8%. Among them, the core platform service net income was only 661 million yuan, a year-on-year decrease of 58.5%. Both light capital loan matching service fees and referral service fees experienced deep declines.

Lexin's total operating income for 2025 was 13.152 billion yuan, a year-on-year decrease of 7.4%. In the fourth quarter, the amount of loan origination was 50 billion yuan, a year-on-year decrease of 3.8%. Traditional credit facility service income was significantly affected by pricing compliance and model transformation.

Xinye Technology’s transaction volume in the fourth quarter of 2025 was only 42.8 billion yuan, a year-on-year decrease of 24.8%. The loan balance at the end of the reporting period was 70.9 billion yuan, a decrease of 6.2 billion yuan from 77.1 billion yuan at the end of the third quarter. Correspondingly, the company's revenue in the fourth quarter was 3.024 billion yuan, a year-on-year decrease of 12.5%; net profit was only 416 million yuan, a 44% drop from the year's high of 750 million yuan in the second quarter.

In the third quarter of 2025, Xiaoying Technology's revenue and net profit both declined quarter-on-quarter, with single-quarter net profit falling 20.2% quarter-on-quarter. At the same time, the 31-60 day overdue rate increased from 1.02% in the same period last year to 1.85%, and the 91-180 day overdue rate rose to 3.52%. Risk provisions and asset impairment pressures increased simultaneously.

The shuffle continues

This time, the strongest regulatory package for online lending is still continuing.

Since the beginning of 2026, multiple departments have issued a number of policy documents one after another, forming a policy package. The new regulations cover the entire industry including collection behavior, interest rate ceilings, platform qualifications, debt negotiation, etc., delineate rigid red lines, and clarify regulatory standards, aiming to thoroughly rectify industry chaos and promote the compliance transformation of the online lending industry.

On March 13, the State Administration of Financial Supervision issued a notice saying that in response to the issue of Internet loan assistance business, the State Administration of Financial Supervision was conducting interviews with the operating agencies of five platforms, including Fenqile, Qifu IOU, Youwodai, Yixianghua, and Credit Fei. The operating entities behind them are Lexin, Qifu Technology, Jiayin Technology, Yirenzhike, Xinfei Technology, etc.