The longer Iran delays, the more the market favors short-term investments

The current situation has made market participation more difficult than ever, and downside risks currently outweigh upside risks.

Tony Pasquariello, head of hedge fund coverage at Goldman Sachs, pointed out in the latest report that the geopolitical conflict caused by the situation in Iran has become the main source of noise in the market, and the intensity of gaming in various trading strategies has increased significantly.

He warned that downward pressure is still greater than upward pressure and suggested that investors simplify risk exposures and increase their cash holdings appropriately to prepare for adding positions at any time when the situation becomes clearer.

Pasquariello said that the conflict is one of the largest oil supply shocks in history, but the decline in the U.S. stock market has been limited so far, which itself is alarming.

He quoted a colleague as saying that "markets are increasingly betting against time" – the longer the conflict drags out, the easier it is for markets to turn into a true growth scare rather than just a supply-driven inflationary shock.

Tactical long and short cases coexist, but risks are still biased to the downside

Pasquariello also laid out the tactical long and short logic of the current market.

The basis for long positions include:

Nearly everyone in the professional trading community with whom he interacts is bearish, and market sentiment indicators have plummeted;

The CTA systematic strategy has significantly reduced long positions;

Large index shorts have been established;

The RSI of the S&P 500 and Nasdaq 100 fell to its lowest level since April last year;

The outlines of the Iran negotiation framework are beginning to emerge.

Short selling grounds include:

There has been no real capitulation selling outside of short-term funds;

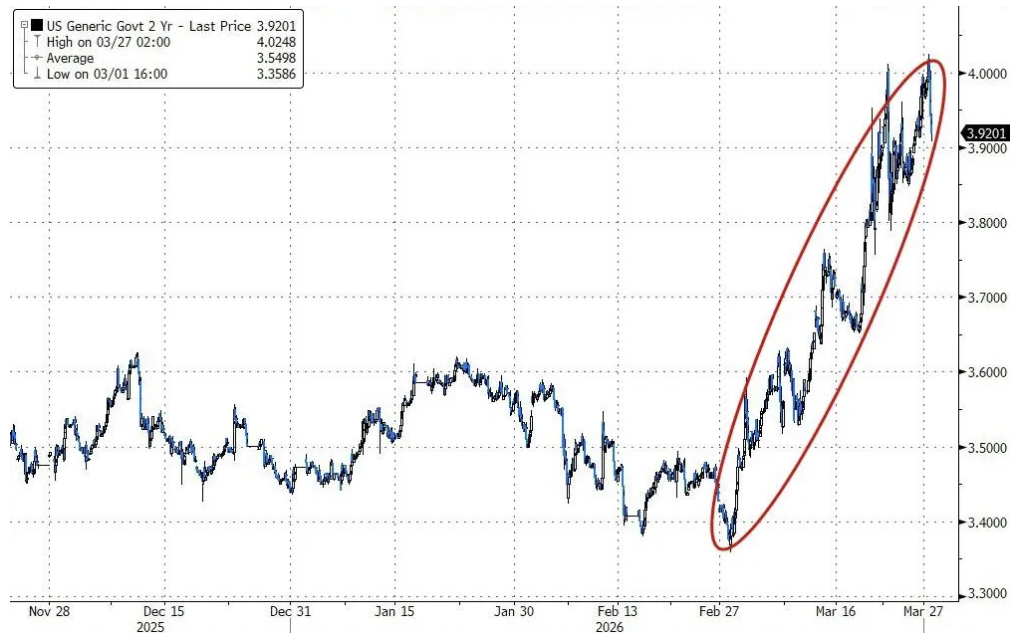

Global bond market trends are also troubling;

The intensity of the conflict has not eased in the critical 48-72 hour window;

Practitioners in the spot commodity market sent a more pessimistic signal.

Pasquariello's comprehensive judgment is that the technical aspects tend to be balanced, but the broader risk set is still biased towards negative results, gap jumps and jumps will continue, the risk-return ratio is still unclear, but the intuitive upward and downward asymmetry still dominates.

Spot commodity practitioners are more worried

Pasquariello's cautious stance was reinforced by observations made during a business trip in Europe. He noticed that those who knew the most about physical commodities were more worried than generalized investors.

The current conflict has caused severe and ongoing disruptions to the physical flow of oil, natural gas and refined products, and triggered a series of policy restrictions, including export bans, fuel rationing and mandatory work-from-home requirements. This means rising inflationary pressures for business operations and an increasingly negative impact on economic growth.

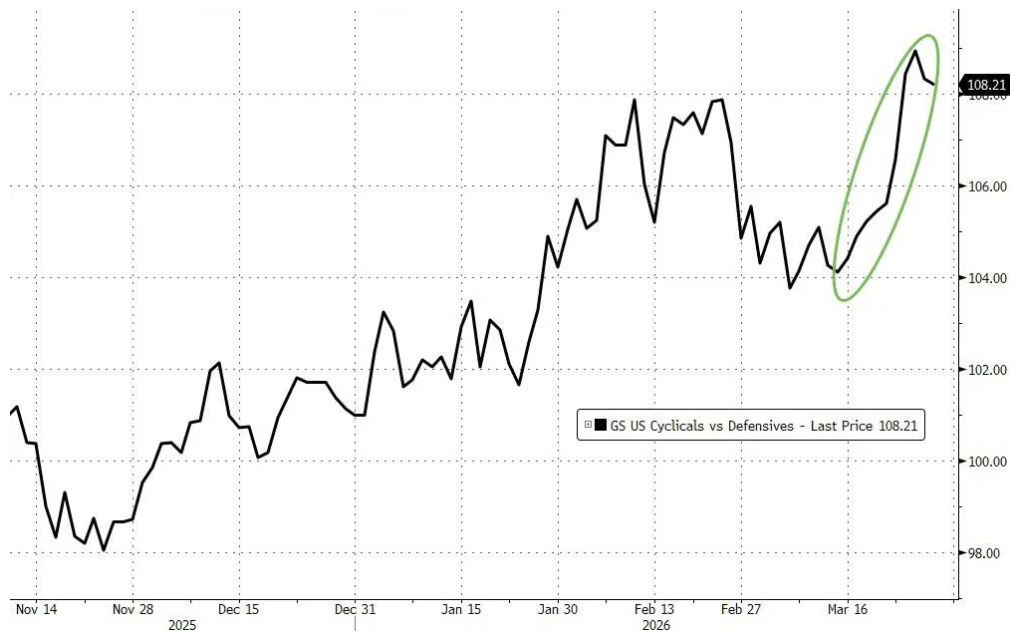

The current mainstream pricing logic in the market is to view this situation as a supply-driven inflationary shock rather than a major growth shock. This judgment is reflected in the sharp decline in global front-end interest rates and the relative outperformance of cyclical stocks over defensive stocks.

Looking back at history, he pointed out that the S&P 500 fell 19% from the high in February 2024 to the low in April, the VIX once soared above 65 in the summer of 2024, the BKX index plummeted 35% during the SVB crisis, and the Nasdaq 100 fell 33% throughout 2022.

"The damage caused by this round of impact has not yet reached a similar magnitude," he believes, which does not mean that the risk has been released.

European stocks suffered capital withdrawals, but Asian stocks performed relatively resiliently

In Europe, Goldman Sachs prime brokerage data showed that long positions in European stocks accumulated over the past year were being liquidated rapidly. Goldman Sachs has lowered its 2026 GDP forecast for the euro zone to about half of its pre-conflict level and expects the European Central Bank to raise interest rates once in April and once in June.

Asian markets have shown significant resilience. Taking South Korea as an example, despite continued selling by foreign investors and a sudden correction in U.S. memory chip stocks, KOSPI still rose by about 29% during the year.

The Japanese market is under pressure from high commodity exposure, with the Topix still recording a gain of about 1% this week. Pasquariello said that judging from customer feedback, South Korea and Japan are the two markets where investors have the most confidence in the medium term among all current options.

Tail risks are still high, it is recommended to increase cash holdings

Pasquariello summed up all the above judgments in four words: tail risk is high.

He cited the close proximity of the forward price-to-earnings ratio trends of Nvidia (NVDA.US) and Exxon Mobil (XOM.US) as a footnote of the times, believing that this signal itself illustrates the deep changes in the current market structure.

"I still see no reason not to simplify risks, moderately increase cash holdings, and be prepared to quickly increase investment on the bright side – I know this is easier said than done," Pasquariello wrote.