China's automobile industry is completing a silent and profound "coming of age ceremony."

In the past few years, China's auto market has used electrification as a spear to pierce the technical barriers of traditional giants; with intelligence as a wing, it has achieved a dimensional leap in user experience; and with astonishing market efficiency, it has pushed the penetration rate of new energy from single digits to more than half of the country, establishing its "status" as the home of global automobile revolution.

As the first half of the industrial revolution comes to an end with a surge in scale and penetration, the whistle of the second half has also quietly sounded. In the entire domestic automobile industry in 2025, increasing revenue without increasing profits should be a common dilemma that everyone is experiencing. This is also like a mirror, reflecting that the extensive growth model that relies on policy incentives and market expansion has gradually reached its ceiling.

2026 may become the year of acceptance for the domestic auto market’s “coming-of-age ceremony”. China’s auto industry will shift from pursuing quantitative miracles to systematically shifting towards building qualitative resilience. This is by no means a simple shift in growth rate, but a deep restructuring involving development logic, competitive landscape and global role. In this context, the focus of the industry will switch from how to occupy the market faster to how to create value more tenaciously and define the future.

Facing the new year of 2026, Gasgoo Automobile has made a prediction for the new development direction of the automobile market for the automobile industry. Next, based on the survey results and the Gasgoo Automotive Research Institute’s prediction of the automobile market, we will take a look at the three dimensions of macro pressure, technological bifurcation and global competition to see where the Chinese automobile market will be in the new year.

Market adjustment accelerates

The primary proposition for China's passenger car market in 2026 is to learn to survive and develop in the post-policy stimulus era.

Gasgoo Automotive Research Institute predicts that the domestic passenger car market will experience a year-on-year decline of approximately 3.3% in 2026, and the overall market will enter a moderate negative growth range. Of course, this judgment does not herald the regression of the industry, but reveals that the market is returning from an abnormally high growth driven by strong external policies (purchase tax exemption, trade-in, scrapping and renewal, etc.) to a normal rhythm driven by endogenous demand, economic boom cycles and endogenous industry innovation.

Survey results of overall performance trends of China's automobile market in 2026, picture source: Gasgoo

Our industry survey results also confirm this trend. When answering questions about the overall development trend of China's auto market in 2026, although moderate growth (0-5% growth) is still the mainstream expectation (38.46%), the total number of respondents who believe that the market will be flat or declining exceeds 57%, reflecting the industry's clear understanding that high-speed growth will be unsustainable.

The underlying reason for this cyclical correction lies in the switching of growth momentum and the emergence of the overdraft effect.

First of all, as the key to promoting the continued growth of the market, there is currently a significant momentum shift on the demand side of the domestic new energy vehicle market. The early pioneer consumer groups driven by policy incentives and early adopter psychology have basically completed car purchases. The focus of market growth has shifted to mainstream household users who are larger, but also more rational and picky.

In our survey results, more than half of the participants (57.69%) showed a clear intention to delay car purchase. Their decision-making relies more on confidence in the economic prospects, the true value of the product and the comprehensive consideration of long-term use costs, rather than temporary policy dividends.

Survey results on the likelihood of individuals or families purchasing or replacing a new car in 2026. Image source: Gasgoo

Secondly, 2025 is the year when many preferential policies are about to expire. The resulting demand front-end effect also leaves a demand "depression" that must be filled in 2026. In other words, it is not that demand suddenly disappears, but that the consumption rhythm has been disturbed before.

The macro market in 2026 may undergo an in-depth stress test. What is being tested is not only the operational resilience of car companies amid slowing sales growth, but also whether the entire industry chain can establish healthy profitability based on market-oriented efficiency after saying goodbye to subsidy dependence.

The price system will evolve from a disordered "volume" to an orderly value return.

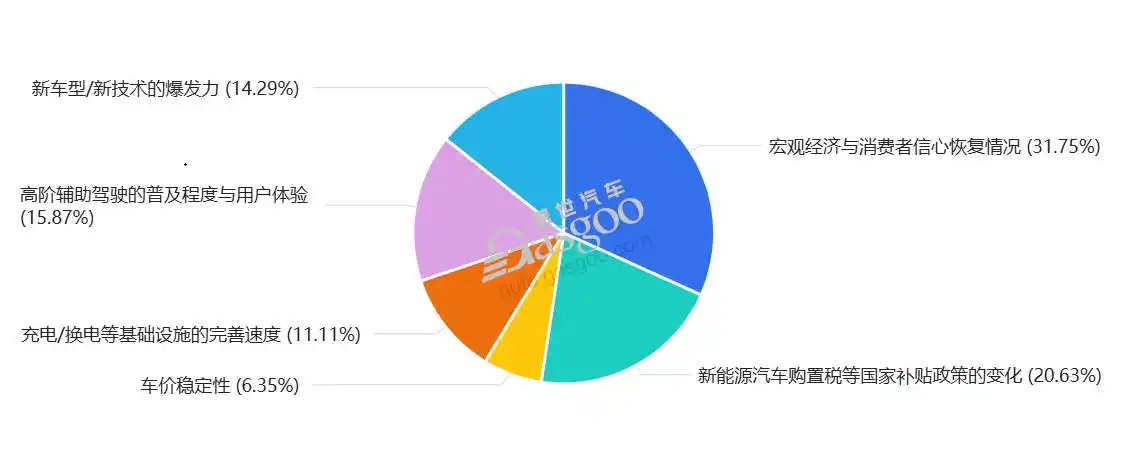

Although the ongoing price war stimulates sales in the short term, it will damage brand value and consumers' trust in price stability in the long term. Only 6.35% of the participants in the survey believed that "car price stability" is a key variable affecting the trend of the auto market in 2026. This is exactly a dangerous signal: when the market generally believes that prices will continue to fluctuate or decline, holding money to buy will become the most rational choice. This actually creates a self-reinforcing cycle: from anticipating a price drop to delaying purchases, car companies further reduce prices for promotions, thus once again reinforcing expectations of a price drop.

Survey results of key variables affecting the direction of the auto market in 2026. Image source: Gasgoo

To break this cycle, the industry needs to shift from a price war to a true value war, and behind this will be a contest of comprehensive strength such as scale effects and technology cost reduction.

What is the core concept of future market competition? The space for pure price reduction has become increasingly narrow. The real competitiveness lies in providing significantly upgraded product experience and full life cycle value at the same or even lower price. Although this process may be accompanied by pain, it is the only way for the industry to mature and shift from scale to profit and quality.

The market will complete a new round of brutal reshuffling during this process, and companies that lack cost control and technology premium capabilities will be eliminated at an accelerated pace.

The battle for technological dominance

When the market moves from rapid growth to a period of steady development, structural growth stories will become even more interesting.

Forecast data released by Gasgoo Automotive Research Institute shows that China's new energy passenger vehicle market is expected to reach 16.9 million units in 2026, a year-on-year increase of 8%, and the market penetration rate will increase to 56%.

As the new energy market continues to accelerate its expansion, the battle for dominance between different technical routes will also become increasingly fierce. Moreover, the essence of this competition is no longer a simple debate on the merits of technical routes, but a competition for the adaptability of different power solutions to the complex Chinese market.

Our survey results also provide a clear public opinion footnote for this competition.

Survey results on which market segment you are most looking forward to in 2026, picture source: Gasgoo Auto

The pure electric (BEV) market is regarded as the market segment with the strongest growth momentum in 2026, with a vote rate of 46.15%, followed by plug-in hybrids (including PHEV and EREV) with a vote rate of 42.31%. Together, they account for nearly 90% of the expected share. This set of data is very revealing, further clarifying the market consensus that electrification (whether pure electric, plug-in hybrid or extended range) is the absolute mainstream. The only 11.54% vote rate for traditional fuel vehicles (including HEV) also confirms its continued marginalization trend.

Obviously, in the foreseeable future, the Chinese market will continue to present a diversified power structure of "pure electric dominance, hybrid hybridization", and it is difficult for any single technical route to conquer the world. This diversified pattern is not a transitional state, but a stable structure that may exist for a long time under China's national conditions of vast territory, complex car usage scenarios, uneven infrastructure development, and obvious stratification of consumer demand.

The pure electric vehicle (BEV) market will enter a new stage of high consolidation and structural deepening.

Analysts from the Gasgoo Automotive Research Institute pointed out that in the first 11 months of 2025, the explosion of the pure electric vehicle market will contribute as much as 88% to the overall increase in passenger cars. Entering 2026, based on the high base, the overall growth rate of the pure electric vehicle market is expected to slow down, but the potential for further expansion of the market scale still exists. The driving force for growth will mainly come from the following aspects: continued penetration and share grabbing of mainstream price ranges; improvement in experience brought about by the improvement of charging infrastructure, especially ultra-fast charging networks; vehicle cost optimization and price exploration space brought about by the decline in battery material costs.

The domestic BEV market in 2026 will most likely shift from inclusive growth to lean growth relying on breakthroughs in specific market segments (such as high-end smart electric vehicles, high-quality mobility vehicles) and highlighting full life cycle cost advantages. The key to its success lies in whether it can transform the anxiety of energy replenishment into the perception of energy replenishment convenience.

In fact, it was under the background that energy replenishment anxiety was still widespread that the PHEV/EREV market ushered in its own highlight moment. In the survey, as many as 42.31% of the respondents were optimistic about the subsequent development of the PHEV/EREV market. This confidence is not groundless. Entering 2026, the domestic plug-in hybrid market, especially the extended-range hybrid track, will usher in an unprecedented product year. Many technology companies and leading new power brands, including Hongmeng Zhixing, Xiaomi, and Xpeng, have planned intensive new product launch plans with extended range. The influx of these new products will greatly enrich consumers' options and promote rapid technology iteration, cost optimization, and experience upgrades through fierce competition.