The war between the United States and Israel to attack Iran is still continuing. The stock price of China National Offshore Oilfield Services (601808.SH, 02883.HK), the leading domestic oil services company, has fallen below the stock price before the war began.

At the beginning of the war between the United States and Israel, one of the most hotly discussed sectors in the market was oil and gas services. Industry insiders believe that the US-Israel war has boosted oil prices. If high oil prices are maintained, the performance of the oil services sector will continue to improve.

Some people in the industry also said that high oil prices may not necessarily be better passed on to the oil and gas equipment and services sector. The beneficiaries are upstream oil companies. Investors should also take into account the uncertainty of oil supply and demand. Because the outcome of the war is uncertain, oil companies are more cautious about expanding production.

When the war began, it was once a hot investment

After the war started on February 28, the oilfield services sector was enthusiastically sought after by funds. However, recent trends have caused concerns among investors.

From March 2 to 3, COSL rose by the daily limit for two consecutive days, peaking at 21.85 yuan on March 4 (the third trading day after the war began), and then fell for three consecutive weeks. It once fell below 16 yuan on March 25, and closed up 0.37% at 16.42 yuan, completely falling below the closing price of 16.87 yuan on February 27 before the war began.

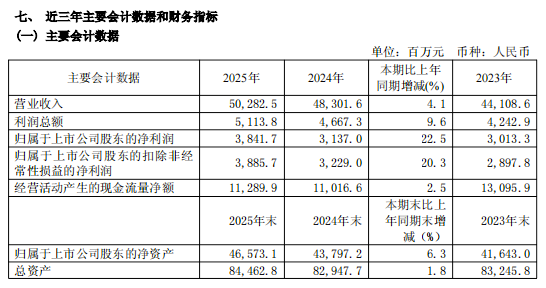

The annual report disclosed on March 24 showed that the company achieved total operating income of 50.282 billion yuan in 2025, a year-on-year increase of 4.1%; realized a net profit of 3.842 billion yuan, a year-on-year increase of 22.5%, a gross profit margin of 17.39% (a year-on-year increase of 1.7 percentage points), and a net profit margin of 8.07% (a year-on-year increase of 1.03 percentage points).

Although performance is still growing, COSL's operating income growth has slowed down for three consecutive years. The year-on-year growth rates in 2023 and 2025 are 23.7%, 9.51%, and 4.1% respectively.

The company stated in its annual report that in 2026, the global oil and gas industry will be in a stage of deep overlapping of cyclical repair and structural transformation. Geopolitical conflicts will continue to intensify global energy security demands. The tight balance between supply and demand will be compounded by complex geopolitical disturbances. Oil prices will maintain medium-to-high fluctuations, laying a solid foundation for the steady development of the oilfield services industry.

Guosen Securities analyzed that as the company's domestic leader in the oilfield services industry, its business structure has been continuously optimized, and its gross profit margin is expected to gradually increase. Against the background of continued tensions in the Middle East, international oil prices continue to rise, and upstream oil and gas exploration and development capital expenditures are expected to increase. Risks that need attention are significant fluctuations in crude oil prices, geopolitical risks, policy risks, etc.

What are the prospects?

As tensions in the Middle East may tend to ease, investors also have certain doubts about the trend of the oilfield services sector.

Xinhua News Agency reported that U.S. President Trump said on the 24th that the war against Iran "has been won" and that Iran is ready to "reach a deal." According to US media reports, the United States has handed over to Iran a 15-point plan aimed at ending the conflict.

Li Qian, an investment consultant at Huiyan Intelligent Investment, believes that the impact of rising oil prices on China Oilfield Services is strong and elastic. The core driver is the rise in drilling volume and price and the resonance of domestic orders, which is the core benefit logic of the leading offshore oilfield services company. The recent fall in stock prices is more a result of short-term expectation revisions and capital games rather than weakening fundamentals. The current valuation is in a reasonably low range, and there is no market overvaluation. Instead, it has a double margin of safety in performance and valuation. Judging from the historical trend of the stock, it has been operating in a large box state. The events in the Middle East have promoted a wave of rise, which is obviously a short-term event and the pursuit of short-term funds. Closing when good times are also a consistent operating characteristic of short-term hot spots. The recent decline in stock prices is a normal phenomenon.

Li Zeming, chief investment officer of Blue Water Capital Management Limited, said that COSL’s stock price has continued to fall since early March, and the market may believe that the war in the Middle East will do more harm than good to it, for various reasons. First of all, the war directly affected COSL's business development in the Middle East. Although it is currently impossible to accurately calculate the proportion of COSL's assets or revenue in the Middle East, judging from the revenue structure, the company's overseas revenue accounts for more than 20%. During the war, the Strait of Hormuz was partially closed, crude oil from the Middle East was difficult to transport, and many oil fields in some countries and other places were suspended. COSL's revenue may be affected to a certain extent during the conflict.

Li Zeming said that the main beneficiaries of the short-term surge in oil prices are oil companies. Because the costs of oil companies have not increased significantly, but the selling price has increased, profits have directly increased. Oilfield services companies have no real benefits during this period. The good news for oilfield service companies is that oil companies outside the Middle East judge that oil prices will remain high for a long time and are willing to invest more capital expenditures to develop new oil fields. Only oilfield service companies can benefit from this.

However, oil companies face an embarrassing situation: it is difficult to judge whether oil prices are at long-term highs or short-term fluctuations. If it is short-term, there is no need to increase production. If it is long-term, it is necessary to increase production capacity cautiously. At present, there are not many signs that oil companies will increase the speed of extraction or investment, so the benefits to oil service companies are still relatively limited.

The annual report shows that of COSL’s revenue of 50.3 billion yuan last year, approximately 38.8 billion yuan came from domestic sources and 11.5 billion yuan came from international sources. International business accounted for nearly 23%.