In 2025, Li Ning will deliver a "stable and progressive" financial report.

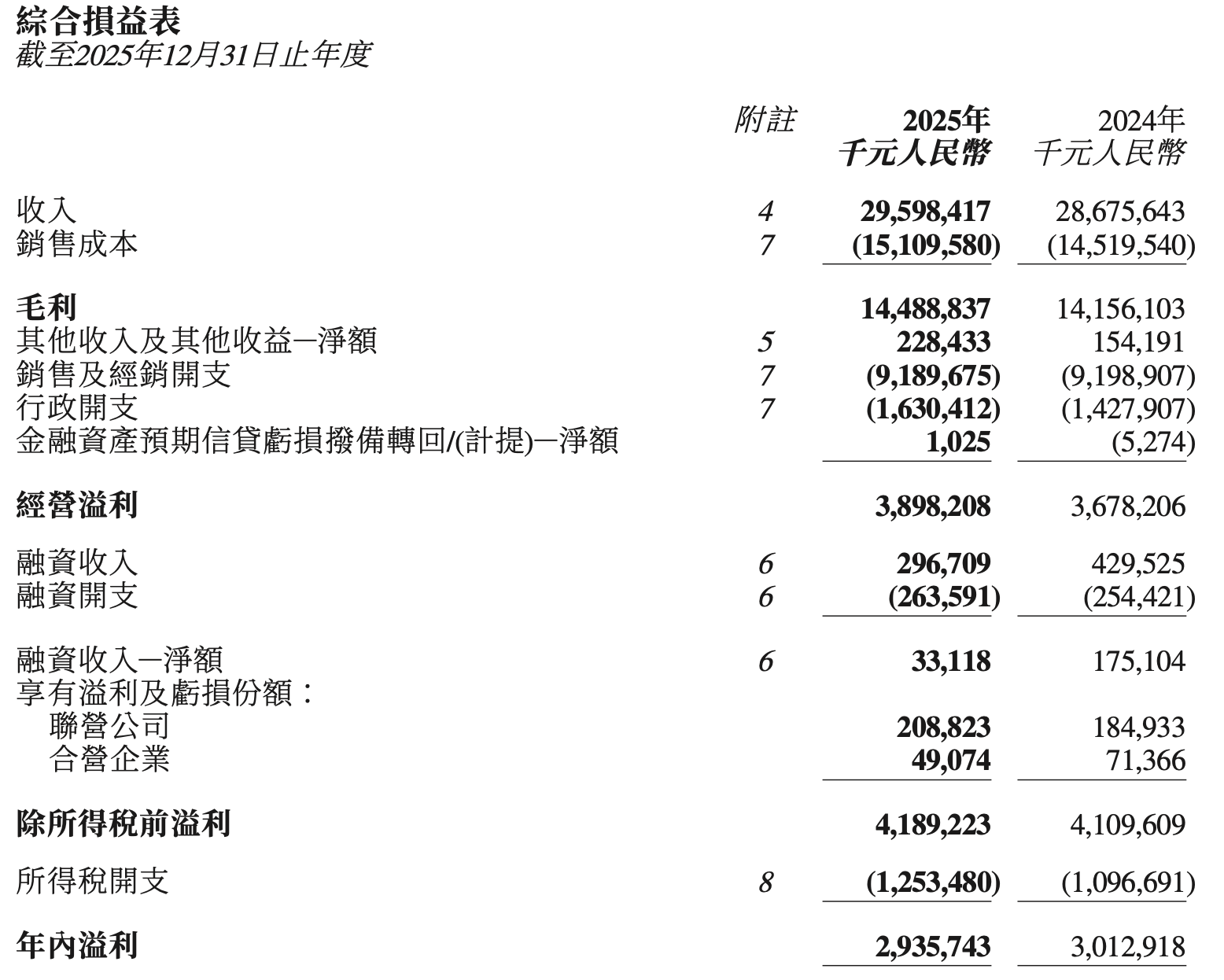

On March 19, Li Ning announced its 2025 financial report: full-year revenue was 29.60 billion yuan, a year-on-year increase of 3.2%, in line with market expectations; but more importantly, on the profit side, the operating profit margin increased to 13.2%, and the net profit rate reached 9.9%, which was better than expected.

In a cycle where consumption tends to be rational, this combination of "moderate growth + profit restoration" essentially means that the company is actively adjusting its growth structure, rather than passively enduring pressure.

But if you look at it from another perspective, the most worthy of revaluation in this financial report is not growth or profits, but a role that has been repeatedly "weakened" in the industry narrative – dealers.

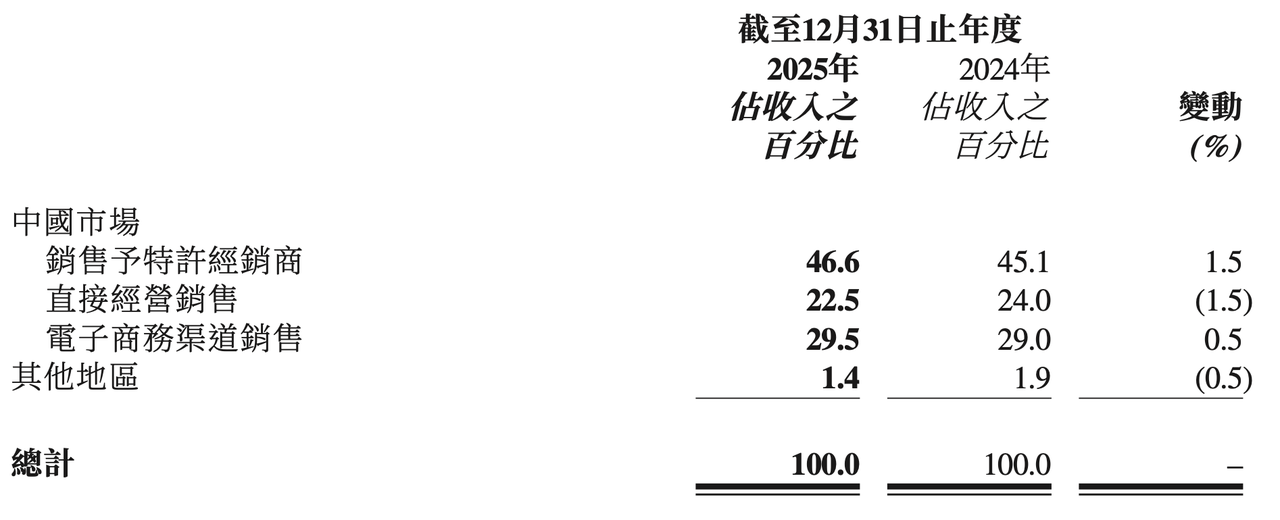

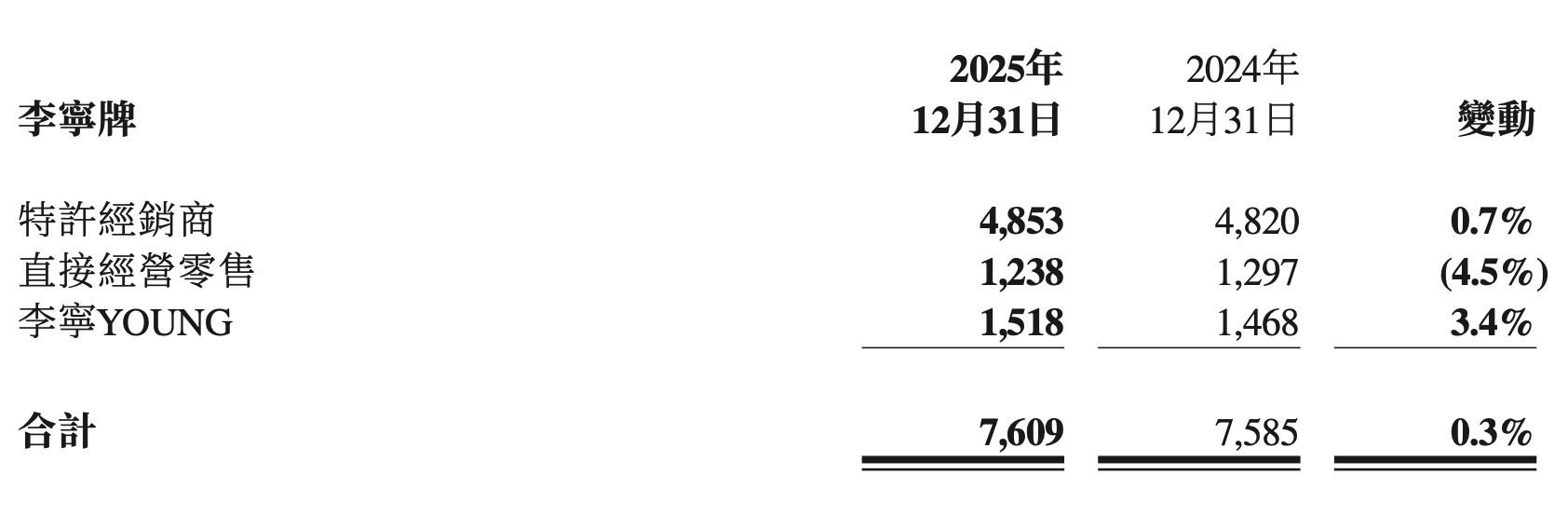

At a time when almost all leading sports brands are holding high the banner of DTC (Direct-to-Consumer), Li-Ning has handed over an answer sheet that "the distribution system is still operating efficiently": in 2025, the proportion of revenue from franchised dealer channels will increase from 45.1% to 46.6%, not only firmly ranking the largest channel, but also becoming the most important source of growth contribution.

This in itself is an anti-consensus signal. It deserves to be taken seriously.

Numbers speak first: Dealers are still ballast

It has to be said that compared to brands such as Nike, Adidas, Anta, and Angpa, Li Ning's channel structure is relatively "traditional."

From the perspective of the overall structure, the group's franchised dealer channel's annual revenue will increase by 6.3% year-on-year in 2025, firmly ranking as the largest channel; the annual revenue of the e-commerce channel will increase by 5.3% year-on-year; the direct-sales channel will experience a phased decline due to actions such as closing inefficient stores, promoting offline store experience upgrades, and optimizing the store matrix.

In Li Ning's channel structure, direct sales, wholesale, and e-commerce account for 22.5%, 46.6%, and 29.5% respectively. There is no absolute dominance among the three, but a pattern of mutual checks and balances and complementary positions has been formed.

This is not the result of natural formation, but a "balanced structure" that is consciously maintained.

In this system, direct sales play more of a role as the anchor of brand image and experience, e-commerce is the traffic portal and conversion tool, and dealers form the base for scale, efficiency and risk sharing.

Especially in 2025, when the direct sales channel is under periodic pressure due to store optimization and discount pressure, the dealer channel will show positive growth and become a key force supporting the stability of overall revenue.

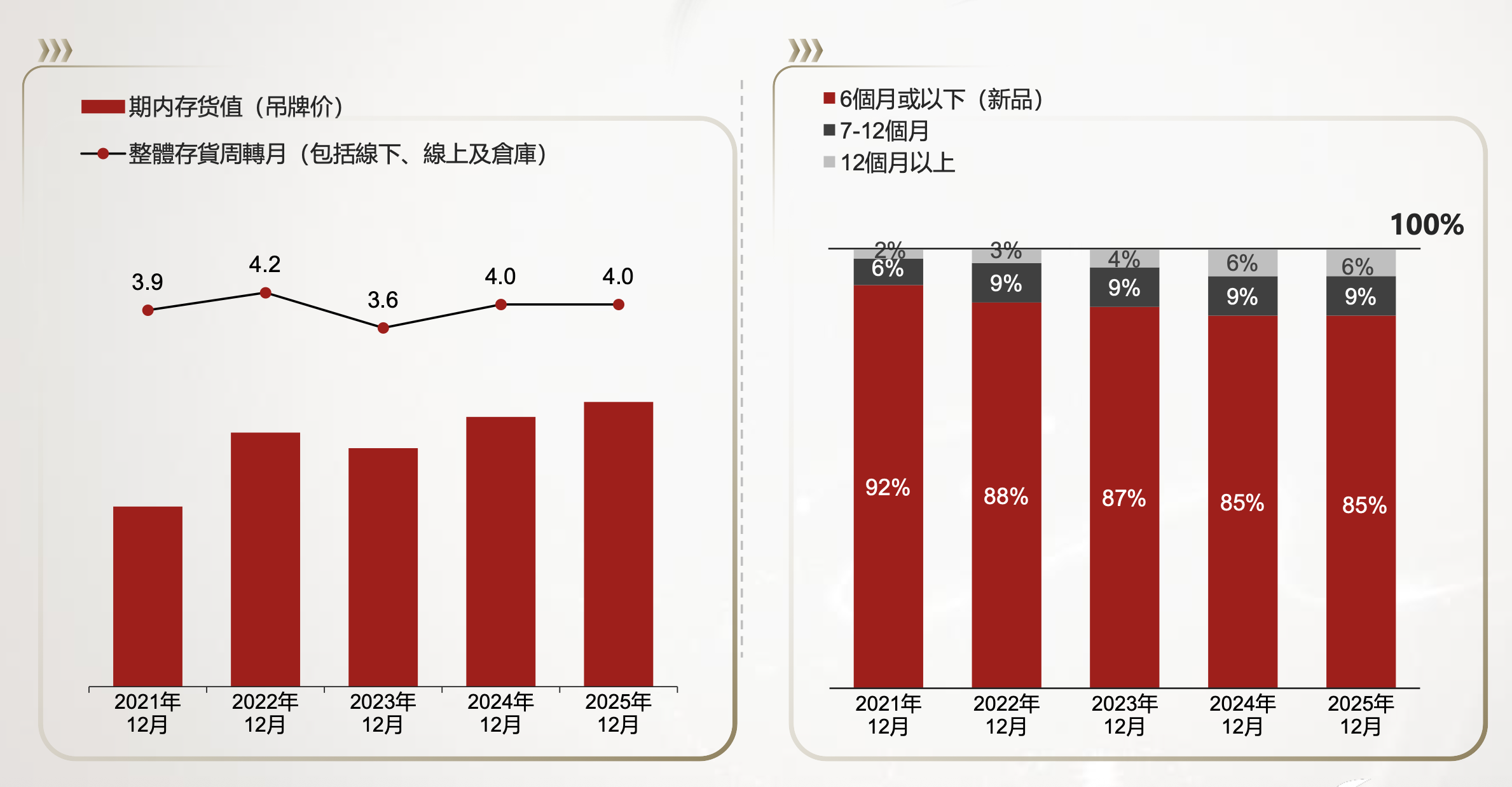

From a financial back-end perspective, Li Ning's profit margin recovery is highly related to this balanced structure: omni-channel inventory turnover is maintained at 4 months, the inventory age structure is healthy, and the ratio of new and old products is balanced; the number of days receivable and payable has remained at the leading level in the industry for many years.

This also explains a deeper question: why Li Ning did not choose to radically transform, but retained such a high proportion of the distribution system despite the entire industry strengthening DTC.

In the past few years, major sports brands have been strengthening DTC.

The DTC expansion of Nike and Adidas has indeed promoted the systematic improvement of brand premium and profitability. Anta Group has also improved its overall profit quality in recent years by continuing to increase the proportion of direct sales. Yao Jian, the former president of Amer Sports Greater China and current president of Wolf Claw, once said in an interview that DTC is an important operating path for Anta Group to "revitalize" many overseas brands.

The benefits of DTC transformation are clear. Brands directly control terminal pricing, reduce the profit diversion of middlemen, obtain more complete consumer data links, and increase gross profit margins.

This logic holds true in first-tier cities and mature markets. But the problem is that the Chinese market is not a homogeneous market, but a highly stratified market with great regional differences. In the broader sinking market, DTC's marginal efficiency is declining rapidly, and high rent, high labor and high management complexity are rigid expenses. Once passenger flow fluctuates, it will be amplified into pressure on the profit side.

Many discussions will interpret "whether to vigorously develop DTC" as the level of operational capabilities. At a stage when consumption is becoming more rational and demand fluctuations are increasing, the risks of the single channel model are being amplified. Li Ning's structure appears to be more resilient.

With a financial base of nearly 20 billion yuan in net cash, the company is not incapable of promoting larger-scale direct operation expansion, but has proactively retained the "buffer layer" of the distribution system. Fluctuating costs such as inventory, rent, and labor are partially moved out into the dealer system, allowing the brand to maintain higher profit certainty in an environment of unstable demand.

What's more, dealers themselves are changing. The channel system in the past, which relied on buyouts and was easily out of control, is being reconstructed by digitalization and refined management.

Li Ning's weekly inventory monitoring, distribution system and warehousing system mentioned in the financial report are essentially achieving "penetrating management" of dealer inventory and sales. This means that dealers are no longer variables outside the brand’s control, but distributed nodes included in a unified operating system.

At the same time, channel quality is also being re-screened. Inefficient stores were closed, resources were concentrated on core commercial entities, and store efficiency in core markets continued to improve. This process of "shrinking inefficiency and strengthening quality" has transformed the dealer network from a tool for scale expansion in the past to a higher-quality retail terminal.

Li Ning’s path: not to fight against DTC, but to “mix optimal solutions”

To understand Li Ning's channel selection, there is a key premise that needs to be clarified: Li Ning is not "rejecting DTC", but looking for a channel combination with the best marginal benefits for a specific market structure and brand development stage.

Compared with the complete DTC model, Li Ning's distribution ratio of nearly 47% has indeed sacrificed part of the gross profit margin ceiling. The existence of middlemen means that brands cannot exclusively enjoy all retail profits.

But what this "price" brings are three capabilities that are more valuable than gross profit in the counter-cyclical consumption: stronger anti-cyclical resilience, faster market response speed, and wider channel coverage.

Anti-cyclical resilience has been verified in 2025.

When direct sales channels are under pressure due to intensified promotion competition and deepening discounts, the dealer network provides a stable base for overall revenue with a positive growth of 6.3%, so that the brand-side profit and loss statement does not have to be directly exposed to the full impact of passenger flow fluctuations. This risk transfer mechanism significantly amplifies value in a cycle where consumption tends to be conservative.

Reaction speed is reflected in another dimension.

Distributors are rooted in the local area, are familiar with regional consumption rhythms, and have the flexibility to allocate goods immediately. This is exactly the capillary conduction capability that brands need most when creating hot-selling products and launching new products.

From first-tier business districts to county-level markets, the geographical coverage of thousands of distribution stores cannot be achieved at the same marginal cost by any DTC system that comes at the expense of property rent and manpower.

This channel logic is particularly amplified in the Olympic marketing cycle.

The core value of brand sponsorship of top events lies in the window period when traffic is concentrated. Every appearance of an athlete on the field is a highlight moment of brand exposure. However, whether this traffic can be converted into terminal sales depends on the brand's channel coverage and response speed during the window period.

During the 2026 Milan Winter Olympics, Li-Ning achieved "zero time difference" for the first time in simultaneously selling the same co-branded products for the Chinese sports delegation, opening up the conversion link of "highlights on the field – real-time planting – immediate purchase".

This link can be run smoothly only if offline terminals have the goods in place and dealers have completed collaborative stocking. A nationwide distribution network provides exactly this kind of infrastructure for "immediate landing of event traffic".

If Olympic marketing requires channel breadth, then multi-category operations and new groups of people require professional penetration depth of channels. The dealer network plays the role of "infrastructure" here.

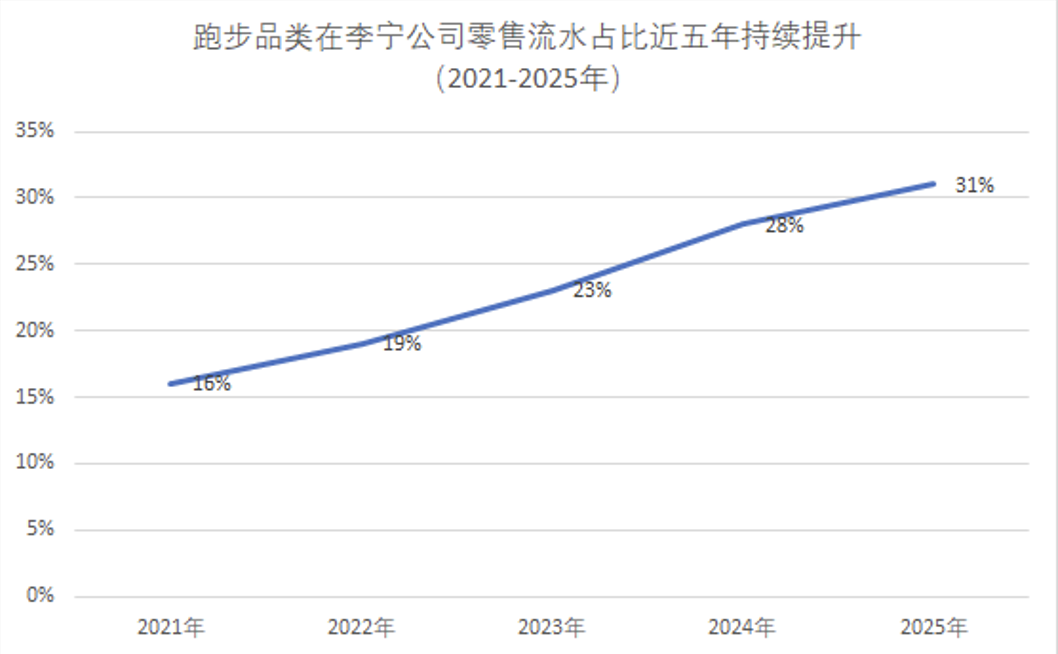

Running and badminton are Li Ning’s two most eye-catching category business cards in 2025. The proportion of running revenue increased to 31%, becoming the largest category; badminton revenue increased by 30%, and the growth rate led the industry.

But these two types of movements are essentially not consumption scenes that only exist in first-tier cities. Running is penetrating into a wider range of people, and badminton is a typical national sport, and its demand distribution itself is highly dispersed.

Under such a category structure, if there is a lack of broad enough terminal coverage, it will be difficult to translate product power into real sales scale.

Running is a classic example. With Feidian's help, the "Breaking Three" runners ranked first in wear rate, and Li-Ning has established a clear professional endorsement on the elite side. But the value of elite runners lies in conveying trust to mass runners.

For this "ripple effect" to be truly realized, it depends on the real-life scenarios where running consumption occurs: not flagship direct stores in first-tier cities, but secondary cities where runners gather, community business districts, and temporary consumption grounds around marathon events.

The value of the distribution network is to transfer the brand trust established by elites to every terminal touch point where mass runners actually consume.

The logic of badminton is more straightforward.

The bottom layer of this round of growth is the rapid increase in demand on the demand side. The national badminton craze has stimulated a large amount of new consumption in a short period of time. Whether it can be realized in time during the craze, production capacity is a variable, and the channel response speed is also critical.

Li Ning has been deeply involved in the badminton track since 2009. The dealer network accumulated in this category just provides the distributed distribution capabilities that are most needed when demand explodes: instead of waiting for consumers to find the brand, the brand has been deployed in advance where consumers will go.

There is a counter-intuitive point worth pointing out here: professional categories often give people the impression that "you should go through boutique channels", such as high-end flagship stores, limited sales, and DTC controlled price systems.

However, professional sports consumption has its own geographical distribution rules. Runners do not only run in Sanlitun, Beijing, and badminton enthusiasts do not only play in Xintiandi, Shanghai. Breadth of coverage is precisely the necessary condition for professional categories to move from niche to mass, rather than the cost of diluting the brand.

Li Ning's "mixed channel model" has begun to show an advantage that is different from the pure DTC path: Compared with complete DTC, this model has sacrificed the ceiling of gross profit margin; but the anti-cyclical ability, market response speed and coverage depth it has gained have demonstrated its actual value time and time again in the instant conversion of Olympic marketing, the large-scale penetration of the running category, and the rapid realization of the explosive demand for badminton.

Behind this is actually a more essential judgment. In a highly stratified and continuously volatile market, it is difficult for a single model to cover all variables. Rather than pursuing the "purity" of a certain model, it is better to build a system that can dynamically adjust between different cycles and different regions.

The nearly 20 billion net cash on hand gives Li Ning sufficient capital reserves to seize opportunities, and there is no need to bet on the radical transformation of a single channel in an uncertain market environment.

Qian Wei, executive director and co-CEO of Li Ning Group, said at the media communication meeting for the performance release, "We are still the same this year. We hope that the company will maintain a medium-to-challenge posture rather than a risky posture. Laying a solid foundation is still Li Ning's top priority. At the same time, we will use a more positive attitude and actions to look at the business and opportunities of different categories in different subdivisions. This time it has become the main idea of Li Ning Group's operations. "

Channels are never isolated operational variables, but physical extensions of brand strategy.

The "hybrid optimal solution" chosen by Li Ning may not be the sexiest answer in the textbook, but it is the one that can best withstand the test of cycles in China's highly stratified market.