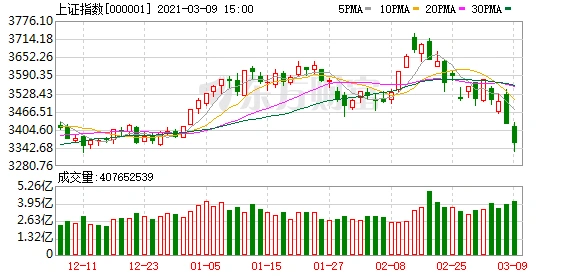

On March 9, A-shares went through a twists and turns trend: from a sharp drop, to a V-shaped reversal, and then to a sharp drop.

In early trading that day, under the pressure of panic selling, the three major indexes of the Shanghai and Shenzhen stock exchanges all fell sharply. The GEM index once plunged by more than 4%. However, as bottom-hunting funds entered the market, group stocks represented by Bailongma stocks took the lead in rebounding. Some Mao stocks, such as Kweichow Moutai, Hengrui Pharmaceuticals, China Duty Free, and WuXi AppTec, rebounded significantly, and the three major A-share indexes once turned red. However, the Baotuan stocks failed in the end, and Mao stocks made a comprehensive counterattack and ended dismally. At the close, all three major indexes fell sharply.

What was impressive throughout the day was that the Mao Index fell by more than 4% during the session, then turned red, and then fell by 2.65%.

For example, among the group stocks, Kweichow Moutai fell by 3% and once counterattacked to rise by 2%. At the close, it gave up all the gains and closed down by 1.17%.

In addition, many Mao stocks fell by more than 5% as of the close. For example, Zhifei Biotech -11.00%, Aviation Power -9.54%, Shanxi Fenjiu -7.79%, Sany Heavy Industry -7.10%, CICC -6.42%, LONGi -6.15%, Baofeng Energy -5.67%, Rongsheng Petrochemical -5.65%, Pien Tze Huang -5.58%.

The two cities generally fell throughout the day, with nearly 3,500 companies falling.

As of the close, the Shanghai Composite Index fell below 3,400 points and closed at 3,359.29, down 1.82%; the Shenzhen Composite Component Index fell by 2.80%; the ChiNext Index fell by 3.50%.

On the same day, among the first-level industries of Shenwan, defense industry, electronics, and mechanical equipment led the decline, with declines of 5.11%, 4.07%, and 3.44% respectively. Only three of the 28 first-level industries increased, namely leisure services, steel, and transportation, which increased by 1.62%, 1.56%, and 0.30% respectively.

What is the cause of this market crash? How will the market outlook go? Can you still invest in group stocks? Institutional figures vary in their views.

Essence Strategy Chen Guo issued a market commentary saying that the adjustment of A-shares from yesterday to this morning will most likely no longer be driven by concerns about U.S. bond interest rates, but will become dominated by absolute profit stop-loss operations and concerns about negative feedback. This constitutes the bottom of the first stage of the adjustment period. Under the influence of various factors, the acute pressure concentrated on the trading level has been relieved. Although recurrences are not ruled out, we think it can basically be judged that the first stage of the adjustment period has ended.

Ma Cheng, chairman of Juze Investment, believes that this wave of decline is mainly due to the bubble digestion of last year's high valuation of white horse stocks when the ten-year U.S. bond yield rose. However, the decline is faster than expected. This is related to the fund's decline – redemption – fall – redemption. In fact, from the continuous stampede decline of white horse stocks and the recent large inflow of money funds, we can see that a redemption wave of equity funds is taking place.

"In the next stage, we will mainly invest in two main lines: one is the non-ferrous metals, steel, and chemical industries that are affected by the economic cycle; the other is the insurance, banking, real estate, and construction sectors with absolutely low valuations." Ma Cheng said.

Wang Xuan, chairman of Chengen Capital, said that there were some risks in A-shares before this round of adjustment. For example, the influx of funds into A-shares from all walks of life has made sentiment overheated. In addition, the high valuations of early-stage group stocks also accumulated downside risks amid expectations of tighter liquidity. In addition, my country's post-epidemic recovery growth has entered an advanced stage, and subsequent policies are easy to tighten but difficult to loosen, so increased market volatility is also expected.

"As for the market outlook, we believe that although high-valued stocks have corrected somewhat, the overall market valuation is not low, and the fund positions on the market are not low. Considering that the short-term fund redemption pressure has not been fully released, there is still a risk of high volatility in the subsequent market. We believe that in investment layout, targets with confirmed performance growth and lower valuations are preferred," Wang Xuan said.

Mao Junyue, investment director of Xinpu Assets, also believes that group stocks have loosened up after the Spring Festival, and the market performance is significantly weaker than that of the external market. Therefore, this adjustment belongs to the adjustment needs of the A-shares themselves, not the influence of the external market. Today's market inherited the weakness of yesterday's market opening high and moving low, with a deep sell-off in early trading. Although it has emerged from a deep V trend, it does not mean that the market adjustment has been completed. Baotuan stocks are high-quality stocks in the market. The adjustment is a reasonable correction to last year's group stocks. Compared with group stocks, small-cap stocks have no valuation advantage, so small-cap stocks will also adjust.

Mao Junyue warned, "There has not yet been a wave of fund redemptions, and the real decline may be yet to come. It is best for investors to control their positions and not blindly buy the bottom."

Xia Fengguang, manager of Future Star Fund of Private Equity Pai Pai Network, pointed out that from an internal perspective, the leading sector of the decline this time was the group stocks that the fund held heavily. These stocks have experienced several times of rise, their valuations are at historically high levels, and their holdings have made huge profits. Some funds chose to leave the market when there were signs of changes in the market environment. From the perspective of external factors, after experiencing the rise of inflation, the market quickly turned to expectations of tightening monetary policy. The main driving force behind the market's rise last year was liquidity. If liquidity tightens significantly, the damage to the market will be very great. At present, the short term is mainly driven by emotions. Monetary policy will not run ahead of economic recovery, but emotions usually have the habit of jumping ahead of the economic recovery.

"There is no need to worry too much about the future mid-term trend. The future market is likely to interpret a different logic from last year's market, that is, there will be a trend of index decline but individual stocks stabilizing. Among them, small and medium-sized market capitalization stocks with clear growth rates may also achieve better returns." Xia Fengguang said.

Lang Chengcheng, director of the Research Department of Furong Fund, judged that the fundamentals of leading companies are still very stable in the long term. Although factors such as excessive short-term valuations, tight liquidity, and lack of profitability have caused the stock price to fall sharply, the company's value has gradually returned to the fundamentals, and the subsequent improvement in the operating performance of leading companies will also digest part of the valuation. In addition, we still need to be wary of some companies whose fundamentals are not that good. When market sentiment is high, such companies also enjoy high valuations, but their fundamental support is weak and it takes longer to adjust.

"Looking forward to 2021, due to the impact of a low base in the first quarter, the performance of leading companies is likely to show a sharp increase year-on-year. The market also has certain expectations for this. Therefore, paying attention to subsequent changes in the company's operating conditions will become the key to guiding investment strategies. In the current valuation return environment, we should pay more attention to leading stocks with relatively low valuations and rising operating performance, or we should be rational and optimistic about the long-term growth performance of leading companies." Lang Chengcheng said.

Hao Xinming, manager of Fangxin Wealth Investment Fund, believes that "the market is currently in a negative cycle of mass group stocks, which is exactly the opposite of the previous group rally. It can be seen that the main driving force behind the post-holiday decline is the previous group white horse stocks. On the contrary, small-cap stocks have stopped falling and stabilized or even rebounded. The current bull market that started in early 2019 has always been a structural market, with obvious sector differentiation and obvious style differentiation."

"The market has come to the present. After a short-term rapid decline, the valuations of previously overvalued group stocks have returned to a certain extent, and some have returned to a reasonable range. However, market sentiment is often either greed or fear. The release of this emotion must be released before the market bottoms out. This requires paying attention to changes in market trading volume. The number of group stocks can gradually shrink. After investors calm down, the market is expected to bottom out. Don't try to catch the flying knife during the current decline. Wait until the flying knife hits the ground and stops moving before entering the market." Hao Xinming said.