The trend of gold has been on a "roller coaster" recently.

On April 22, after crossing the $3,500/ounce mark and reaching a historic high, gold prices entered diving mode. From April 22 to May 4, the COMEX gold range retracement (maximum decline) was 8.56%.

The price of gold "jumps up and down", affecting the emotions of investors and consumers. From the beginning of 2024 to the present, gold has continued its rise and maintained a high level, and the gold market is also playing a wealth game. Under the illusion of "guaranteed profit without loss", some investors aggressively entered the market. Some people mortgaged their properties to speculate in gold, while others borrowed money to speculate in gold.

"The gold in my hand cost me six years of salary in one day. Now my head is cold and I sit in a daze all day." On April 23, COMEX gold fell by 3.45% in a single day. He Mi, a self-proclaimed "gold gambler," said he was stunned.

Born in a rural area, he now earns a monthly salary of about 3,000 yuan. At the beginning of this year, under the "bewitchment" of his friends, he took out credit cards, consumer loans, online loans and other loans, and scraped together 600,000 yuan to fill his gold position, and participated in gold futures trading. With a principal of 600,000 yuan, and magnified by 10 times leverage on gold futures, his position has reached 6 million yuan. "Ten times leverage means that if the price of gold drops by 10%, my account will directly return to zero." He Mi said.

1. Online loans to speculate in gold, "making money while lying down" is an illusion

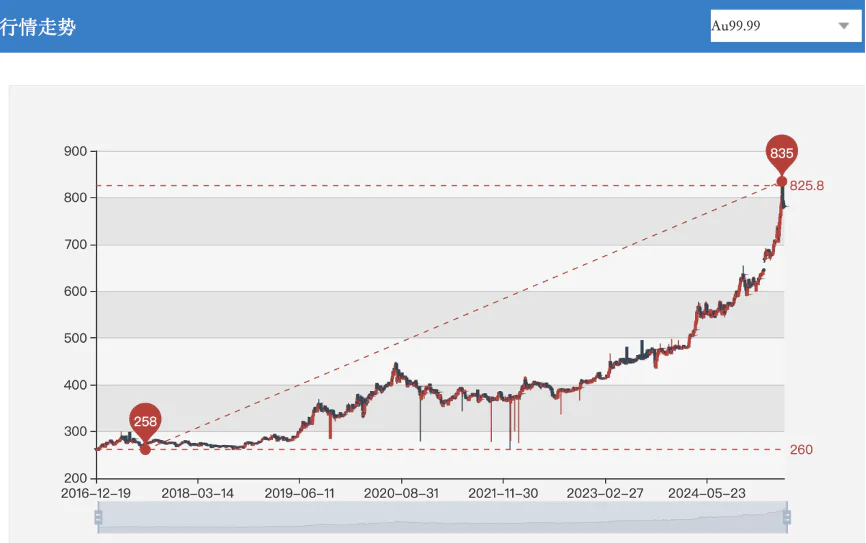

Year to date, gold has continued to hit new highs. According to Wind data, as of May 4, COMEX gold has increased by 22.96% during the year. If calculated from the beginning of 2024, the increase in COMEX gold will reach 56.74%.

Gold price trend since 2016; picture from Shanghai Gold Exchange

In the hot market, some investors began to take desperate risks under the illusion of "making money", hoping to make a lot of money through loan speculation. They are turning their attention to bank consumer loans, credit cards, and even online loans.

"I took out a loan of 700,000 yuan to buy gold, and it paid off!" Liu Hao, born in the 2000s, said that after graduating from college in 2023, he worked as an inspector in a factory, earning a monthly salary of 7,000 to 8,000 yuan. Unwilling to accept the status quo, he set his sights on financial management.

At the beginning of 2025, after Liu Hao had some savings, he invested some of his funds in the gold market. As the price of gold continued to rise, Liu Hao, who had tasted the benefits, came up with the idea of "buying gold with a loan."

"I took out a loan of 700,000 yuan to buy gold, and all the mainstream (online loan) APPs lent some money." Liu Hao made careful calculations. Most of the platforms he borrowed from were granted a one-month interest-free period, which greatly reduced the cost of funds. In mid-April, he bought gold reserves on JD Gold in batches at an average cost of 775 yuan/gram.

Due to the large fluctuations in gold prices, coupled with the transaction fees, loan interest and other costs of gold buying and selling, it is not easy to make money while lying down.

On April 22, gold prices reached a periodic high, with Au9999 spot gold on the Shanghai Gold Exchange reaching 835 yuan/gram. Liu Hao said that the book profit exceeded 50,000 yuan in just six days. But he didn't have time to be happy for long, and gold soon ushered in a correction. On April 27, the price of Au9999 gold fell back to 777 yuan/gram. Liu Hao said that day, "The current profit of more than 1,000 yuan in the book, after removing the handling fees, is only enough to eat Haidilao." He frankly regretted not selling gold at a high of more than 800 yuan.

In the end, Liu Hao chose to take a gamble and continue to hold gold. He believes that gold will still see a wave of gains during the May Day holiday.

"Either wealth freedom, or nothing. There are only two results for me entering the gold market." The more bold and radical He Mi told Times Finance, "I am bullish on gold in the long term, but I am not sure whether the increase in gold can outperform the interest rates on online loans." This may be the reason why he chose to further increase leverage and invest in gold futures.

The wishful thinking of using online loans to speculate in gold is not easy to achieve.

Times Finance has noticed that the current annualized loan interest rates on mainstream online lending platforms range from 7% to 24%. According to a report released by Southwest Securities, taking the product information disclosed by a consumer finance company as an example, as of the end of 2023, the annualized interest rates of the company's credit products were mainly concentrated in the range of 7.20% to 23.76%, but the annualized interest rate levels of loans between 15% and 20% and 20% and above accounted for more than 80%.

A report released by the Shanghai Gold Exchange in 2017 showed that from 1970 to 2014, the annual return rate of gold was 8.1%, which is equivalent to the stock return rate in developed markets. In addition, the volatility ratio of gold returns in the past 20 years has been significantly higher than that of other commodities.

Social media witnessed this “gold rush”. Times Finance found on a social platform that there were more than a thousand shared posts about "loans to buy gold", and many financial bloggers even posted posts about selling houses/mortgaging real estate to buy gold.

2. Buying a gold quilt at a high position: I can’t bear to sell it, but I can’t bear it if I don’t sell it.

Since April 22, the gold market has taken a turn for the worse, and many investors who took out loans to buy gold have been "trapped at a high level and suffered heavy losses."

"I took a loan of 80,000 yuan and bought gold at a high price of 830 yuan/gram. I didn't expect to be trapped." He Li has been excited to watch the price of gold rising since 2025. After seeing posts about borrowing money to buy gold on social platforms, she followed the trend and performed similar operations.

After April 22, the price of gold began to correct. On April 24, He Li’s book loss exceeded 6,000 yuan. "I still have to pay off the credit card loan next month. I can't bear to sell it now, and I can't bear it if I don't sell it," she lamented.

People like He Li who took out loans to buy gold are not alone in being trapped in high positions. “I borrowed a credit card worth 100,000 yuan and bought gold for 830 yuan/gram. I was so hung up that I was about to cry.” “I’m chasing the high price. I bought gold at a high price of 810 yuan/gram and bought a bunch of money-losing goods. The one-month interest-free period for online loans is coming soon.”… Since April 22, as the international gold price has fluctuated lower, such discussions have emerged in investment communities and social platforms.

A gold futures analyst in South China told Times Finance that the rising gold price in consecutive years has induced some investors to have a cognitive bias that gold prices will rise unilaterally, which in turn has led to irrational investment behaviors such as high-leverage allocation of gold assets. It is worth noting that as a typical high-volatility investment target, the price of gold is significantly affected by multiple market factors, but most individual investors often ignore scientific assessment of market risk exposure during the participation process.

At present, relevant agencies have taken action to suppress loan speculation.

On April 23, the Shanghai Gold Exchange issued a notice on adjusting the margin levels and price limits of some gold futures contracts to increase the cost of adding "leverage". The notice stated that the margin level of some gold futures contracts will be adjusted from 15% to 16%, and the price limit will be adjusted from 14% to 15%.

In addition, many banks have issued intensive risk warnings stating that credit card funds are not allowed to be used for gold investment. Times Finance has noticed that since April, many banks, including Bank of China, China Guangfa Bank, and Industrial Bank, have clearly announced that if credit card funds are used for gold investment, violators will face reductions, transaction restrictions, or even card closures.

Industry insiders warn that "loan speculation" involves multiple risks.

Du Juan, a senior researcher at the Jiangsu Commercial Bank Research Institute, told Times Finance that the first is to invest in gold with leverage. If the investment suffers a loss, the amount of the loss will be magnified by the leverage. At that time, not only the principal will be lost, but also a large amount of debt may be incurred;

Second, gold, as a safe-haven asset, is more suitable for medium- and long-term holdings. The purpose of speculating in gold through short-term loan funds such as online loans and credit cards and using leverage is for short-term speculation. In the face of short-term fluctuations, it is more difficult for ordinary people to obtain profits;

Third, credit cards have usage restrictions and are usually used for consumption activities. If a bank finds that a borrower has misappropriated consumer loans to speculate in gold, the bank has the right to require the borrower to repay the loan in advance. At that time, the borrower is prone to the risk of funds being cut off, and the credit report performance will also be affected if the relevant behavior is uploaded to the credit report record;

Fourth, with the help of online loans and credit cards, some investors who do not meet the financial threshold and are not familiar with gold investment knowledge blindly invest in gold under the influence of external voices, increase their capital through loans, and purchase high-risk investment products that are not in line with their own tolerance. When the market fluctuates, it is more difficult to grasp the market and more likely to fall into losses.

(At the request of the interviewees, He Mi, Liu Hao and He Li in the article are pseudonyms.)