After deflation for so long, long-awaited inflation is coming?

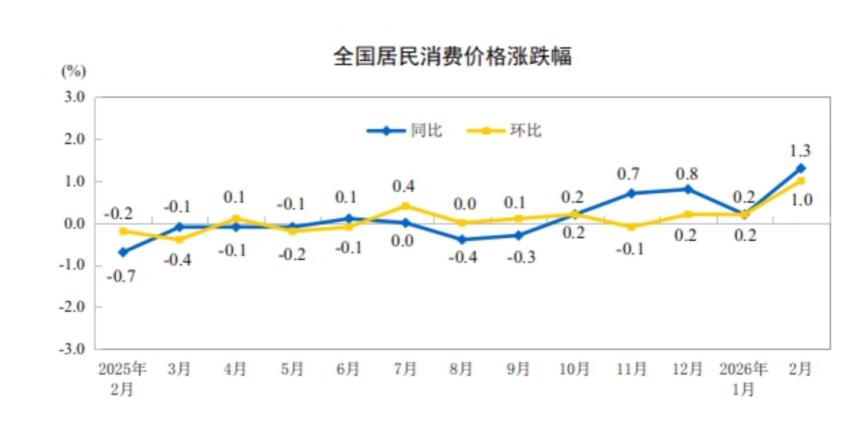

On March 9, the National Bureau of Statistics announced inflation in February 2026. The results showed that China's CPI increased by 1.3% year-on-year in February, a new high in the past three years.

This result far exceeded market expectations. Previously, Bloomberg’s survey of domestic and foreign institutions concluded that the CPI was expected to grow by 0.9% year-on-year.

You should know that the data for February does not include the impact of the US-Iran incident on oil prices. In other words, without high oil prices being transmitted to the country, CPI has begun to rise.

Even more staggering is the core CPI. According to calculations by Huatai Securities, after excluding the impact of food and energy prices, the core CPI in February rose sharply to 1.8% year-on-year.

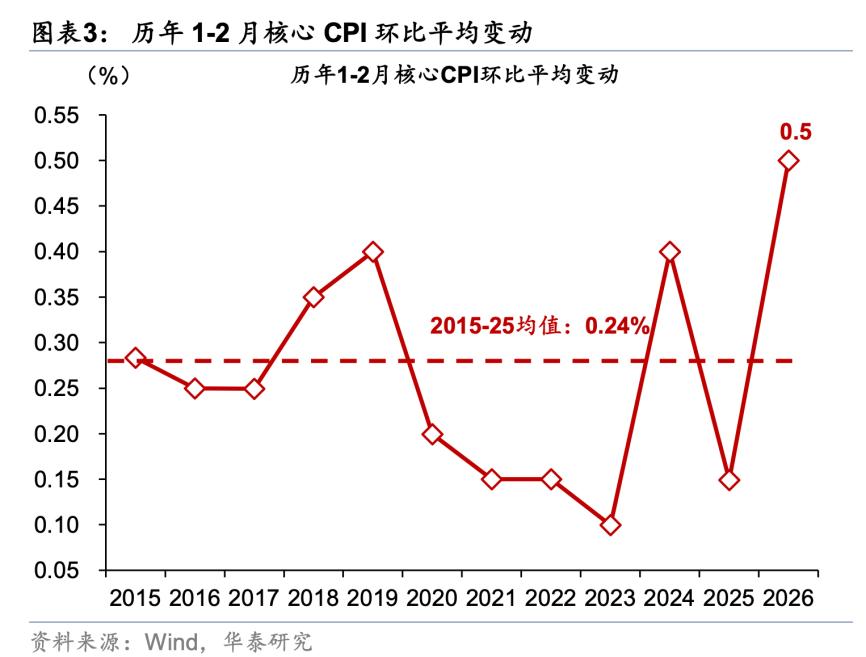

Combining the month-on-month growth rate in January and February, after excluding the Spring Festival effect, it hit the highest value since 2015.

What is the fundamental reason for the rise in CPI?

Deflation has been going on for such a long time, and I feel really uncomfortable seeing such changes in CPI. Why?

Figures from the Bureau of Statistics show that in February, the CPI for urban residents increased by 1.4% year-on-year, significantly higher than the 0.9% for rural residents.

Friends who have been following Yetan Finance for a long time may still remember that according to our long-term tracking, the CPI in rural areas has been better than that in urban areas for a long time in the past.

The reasons are nothing more than two points:

First, due to a period of sluggish housing prices, urban residents' balance sheets have been more seriously damaged and their willingness to consume is not strong; second, people's livelihood and industrial policies are more tilted towards rural areas, and the channel of Internet + commercial real estate is sinking, which has stimulated the consumption desire of non-urban residents.

What happened in 2026 to cause such a big urban-rural reversal in CPI?

Excluding base effects, some signs may already be there.

We often take Shanghai as an example. Before the second quarter of 2025, Shanghai was still competing with Beijing to see whose consumption was worse. However, with the rise of the stock market, Shanghai's consumption began to pick up in the third quarter, and its performance in the fourth quarter even exceeded the national average.

As the impact of housing prices weakens and the impact of the stock market becomes stronger, I believe more and more cities will move closer to Shanghai.

In addition, the 2026 Spring Festival has a very distinctive feature – the reverse New Year, that is, the children do not return to their hometown, but bring their parents to the city for reunion. This will directly affect urban and rural consumption, causing one to wax and wane.

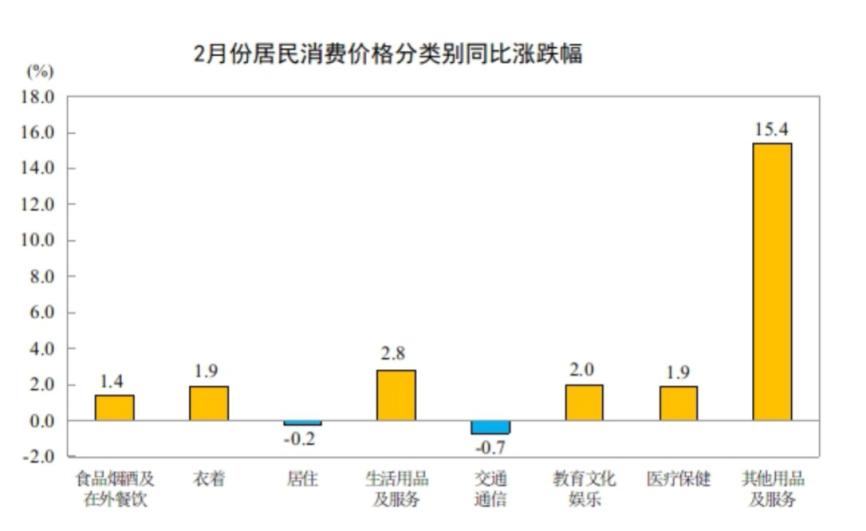

From the perspective of consumer goods and services, rising prices can be said to be global.

According to data from the Bureau of Statistics, in February, food prices increased by 1.7%, non-food prices increased by 1.3%; consumer goods prices increased by 1.1%, and service prices increased by 1.6%.

Among food, categories such as tobacco, alcohol, and catering have the greatest impact (heaviest weight) on CPI, driving up CPI by 0.41 percentage points with a year-on-year increase of 1.4%. The price of fresh vegetables increased by more than 10%, leading the CPI to rise by 0.19 percentage points.

Among the main food products in February, eggs, pork and other categories were still lagging behind, and the total dropped the CPI by nearly 0.3 percentage points.

In addition to food, the remaining six categories, 4 rising and 2 falling, and services related to tourism and jewelry consumption all performed outstandingly. Among them, other supplies and services including hotel accommodation, hairdressing and bathing surged 15.4%.

Other supplies and services are also categories that we have been tracking for a long time. We expected that the performance would be good, but we did not expect it to be so good, with a growth rate of 15.4%.

You know, in February 2025, other supplies and services were already at a high base, with a year-on-year growth rate of 6.5%. At the end of 2025, the year-on-year growth rate of this category soared to 17.4%.

In February 2026, other supplies and services will still see double-digit price increases, which shows the popularity of consumer industries such as tourism and bathing.

To sum up, if domestic consumption does not decrease in 2026 and supply is controlled, CPI may indeed exceed expectations.

Compared with CPI, PPI is relatively weaker, but it is also in line with expectations, and there is no "normalized" weakness that is lower than expected.

According to data from the Bureau of Statistics, in February 2026, China's PPI fell by 0.9% year-on-year, and the decline continued to narrow by 0.5 percentage points, continuing the past recovery trend; month-on-month, PPI rose by 0.4% month-on-month in February, which was the same as the increase in January, and also maintained price inertia.

The PPI in February, whether year-on-year or month-on-month, was close to the forecasts of domestic and foreign institutions, which is a rare phenomenon in recent years.

PPI was in line with expectations, CPI far exceeded expectations, and the overall performance of China's price index was outstanding.

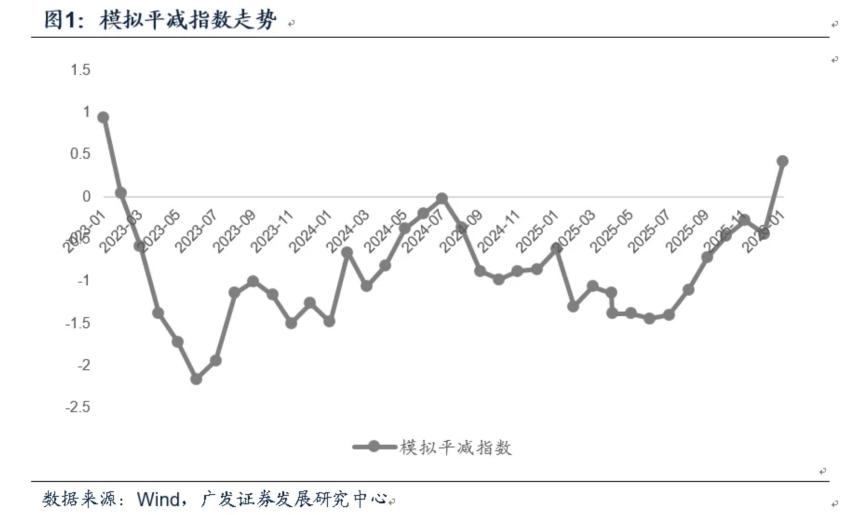

According to a March 9 report from GF Securities, the simulated (price) deflator with a CPI and PPI weight of 64 turned positive for the first time in 36 months. This is 3 months earlier than GF had expected.

Will oil prices really cause inflation to rise in China?

Regarding inflation, one unexpected factor that cannot be ignored is oil prices.

Because of Lao Chuan's recklessness, the crude oil market has experienced a huge shock since March. It only took one week to rise from 60+ US dollars to 120 US dollars, and it took less than two days to fall back from 120 US dollars to 80+ US dollars.

With oil prices so stimulating, investors are hedging on a large scale, taking advantage of the fire. For those engaged in economic analysis, such large fluctuations in oil prices are a time to challenge their professional abilities.

If you believe that the conflict will become long-term, oil prices will become the decisive factor in inflation, thus affecting all aspects such as monetary policy, consumption willingness, and market sentiment. If you believe that the conflict is short-term, everything will be bands and pulses, and will not form a long-term climate. Regardless of the economy or policy, it will eventually return to the established path.

How to deal with it? The bottom line principle may be a more appropriate way to respond.

The so-called bottom line is what will happen to inflation in the worst-case scenario.

Recently, many domestic and foreign institutions have made calculations on the correlation between oil prices and inflation, and the conclusions reached are not very different.

Huachuang Securities estimates that every 10% increase in oil prices will boost PPI by 0.3 to 0.4 percentage points and CPI by 0.14 percentage points.

The model of West China Securities shows that every 10% increase in domestic oil prices will directly boost PPI by about 0.6 percentage points month-on-month.

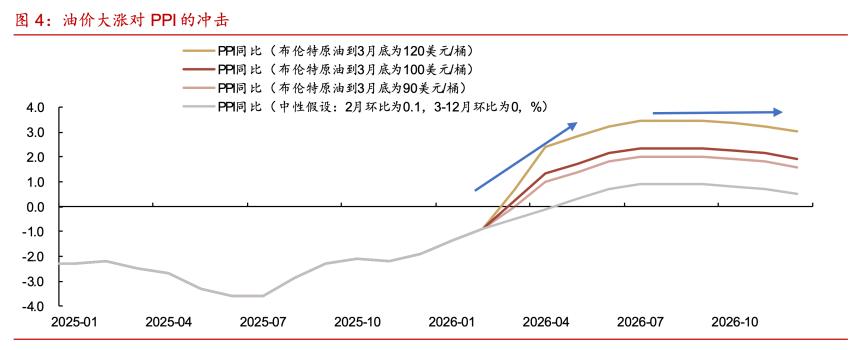

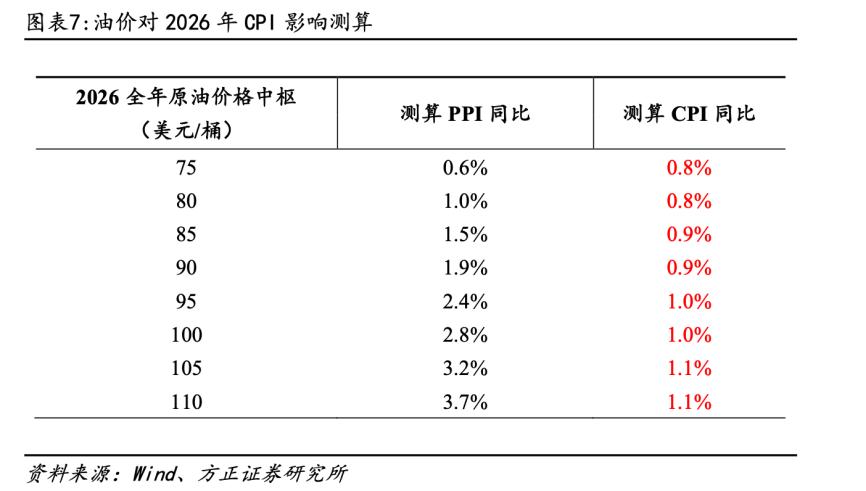

At the end of March, if the oil price reaches US$120, the PPI will reach 3% in 2026; if the oil price falls to US$100, the PPI will be around 2%; if the oil price is US$90, the PPI will be between 1.5% and 2%.

Founder Securities said that in 2026, even if the central price of oil prices is US$110, China's CPI will be pulled to 1.1%. Of course, the PPI will be higher, close to 4%.

It is not difficult to see that domestic institutions generally believe that even under the most exaggerated circumstances of oil prices, CPI will not reach the ideal level of 2%. The stimulation of oil prices will help China's inflation return to normal to a certain extent.

Foreign institutions have a more straightforward view.

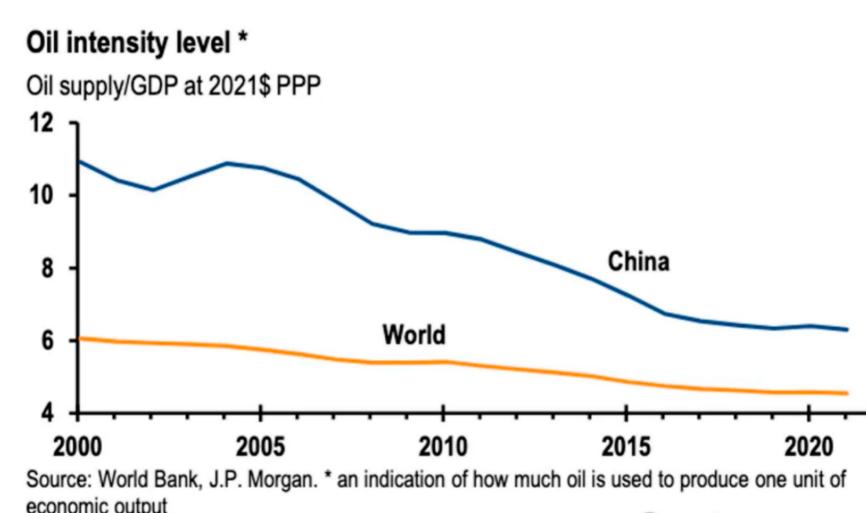

JP Morgan believes that as the status of new energy continues to improve, the oil consumption of the Chinese economy has dropped significantly in recent years. It is estimated that the transmission coefficient of oil prices to China’s consumer price index is only 0.1.

Deutsche Bank even believes that a sharp rise in oil prices will be a reward for the Chinese economy.

According to Deutsche Bank's estimates, if oil prices rise by 50%, China's PPI can change from a long-term negative number to a healthy range of 3% in one fell swoop, allowing China's industrial sector to quickly achieve reflation and get out of the haze of losses.

The problem of overcapacity can also be solved, because global demand for green energy will surge again.

To sum up, this round of rising oil prices will make the Chinese economy better, rather than making it worse.

The "bottom line" is this, what else is unacceptable?

Of course, there is always a gap between reality and expectations, especially in the time and space where Lao Chuan lives, expectations have long become empty assumptions.

Before March 9, domestic and foreign media seemed to believe that the conflict would become protracted. But on March 10, Lao Chuan suddenly jumped sideways, indicating that everything might end soon. Subsequently, Al Jazeera reported that Tehran's first condition for a ceasefire is that "there will be no further acts of aggression."

As soon as the two pieces of news came out, international oil prices began to plummet.

Almost at the same time, Saudi Arabia, the United Arab Emirates, Iraq and Kuwait announced cuts in oil production, with a total reduction of up to 6.7 million barrels per day. The Group of Seven countries, which had previously been preparing to release oil reserves, also announced that they would not release strategic oil reserves for the time being.

It seems crude oil is no longer an issue.

Too fast.

But, this is Lao Chuan, isn’t it?

Looking at oil prices from Lao Chuan's perspective, everything is logical. In the past, as long as the U.S. stock market was in turmoil, Lao Chuan would change his tune. As long as core voters began to complain and structural support began to loosen, Lao Chuan would stop.

Veteran actors are used to old scripts and can't get out of their comfort zone.

On March 9, before Laochuan jumped, the U.S. stock market hit a key point. Taking Nasdaq as an example, since September 2025, as long as it falls to 22,000 points, Lao Chuan will "rescue the market", and it has worked repeatedly.

On March 9, it reached 22,000 again, and Lao Chuan couldn’t sit still.

In addition, on the trading day before March 9 (March 6), the U.S. Bureau of Labor Statistics released a very dismal employment data, which may accelerate Lao Chuan's change in attitude.

According to data from the U.S. Bureau of Labor Statistics, U.S. non-farm employment fell by 92,000 in February, significantly lower than market expectations for a growth of 59,000.

AI's impact on employment is becoming increasingly severe, with medical care, information, transportation, and manufacturing being the areas hardest hit by unemployment. The employment situation has deteriorated. If oil prices rise sharply, it is easy to imagine the electoral success of Lao Chuan and the Republican Party.

In fact, the conflict between the United States and Iran that Lao Chuan advocated failed to produce the "gathering of flags" effect he expected.

According to an article in The Economist on March 8, the Gulf War in 1991 caused George Bush's approval rating to soar from 64% to 82%; during the "War on Terror" in 2001, Bush's approval rating soared from 51% to 90%.

Where is Lao Chuan? Since the outbreak of the war, it has been only 38%. The median voter, who can most influence the outcome of the election, has only 25% support.

This result may be beyond Laochuan's expectation and is also the core factor in his inability to fight for a long time.

Of course, Lao Chuan won, after all, victory can be defined by oneself.

The right to call a stop is indeed in Lao Chuan's hands. If the United States doesn't fight, and other countries fight, does it still make sense?

Therefore, it is neither ethical nor realistic to expect long-term rises in oil prices to help China emerge from deflation. Domestic problems must be solved by the country itself.