Member of the 14th National Committee of the Chinese People's Political Consultative Conference, chairman of the China Development Research Foundation, and former deputy director of the Development Research Center of the State Council. Source of this article: China Real Estate News

Zhang Junkuo: Current economic situation, development trends and policy thinking

Hello everyone, I am very happy to participate in the "2026 China Real Estate Annual Trend Forum". According to the meeting arrangement, I combined my study of the spirit of the Central Economic Work Conference to communicate with you on the "current economic situation, development trends and policy thinking" to provide a macro background for everyone to think and discuss the high-quality development of real estate. It mainly talks about three aspects, one is about the basic characteristics of the current economic situation, the second is an introduction to this year's market demand environment and development trends, and the third is some thoughts on further releasing the potential of domestic demand and promoting a high-level dynamic balance of total supply and demand.

1. About the basic characteristics of my country’s current economic situation

Regarding the current economic situation, the Central Economic Work Conference summarized it in two sentences: first, "to move forward under pressure and develop in a new and optimal direction"; second, "there are still many old problems and new challenges in economic development." It should be said that these two sentences summarize the basic characteristics of the current economic situation more accurately and objectively.

“Moving forward under pressure” is mainly reflected in macroeconomic indicators. According to data from the National Bureau of Statistics, my country's GDP will grow by 5% in 2025. Among the world's major economies, my country is still the fastest growing economy. According to relevant statistical forecasts, the US GDP growth rate in 2025 is expected to be around 2.1%, the Eurozone is expected to be around 1.4%, and Japan is expected to be around 1.2%.

Judging from the main physical volume indicators, in 2025, the electricity consumption of the whole country will increase by 5.5% year-on-year, the highway freight volume will increase by 3.8%, and the railway freight volume will increase by 2.1%, which is basically consistent with the macro aggregate indicators.

"Developing towards newness and excellence" is mainly reflected in the continuous optimization of the economic structure and the continuous improvement of high-quality development.

For example, from an industrial perspective, the high-end, intelligent, and green manufacturing industry is accelerating, and new products, new industries, and new drivers continue to grow rapidly. In 2025, the added value of the equipment manufacturing industry will increase by 9.2%, and the added value of high-tech manufacturing will increase by 9.4%, with growth rates 3.3 and 3.5 percentage points faster than those of industries above designated size respectively.

For another example, from the perspective of consumer demand, service consumption is faster than commodity consumption. In 2025, service retail sales will increase by 5.5% over the previous year, which is 1.7 percentage points higher than the growth rate of commodity retail sales in the same period. The retail sales of services such as digital consumption, culture, sports and leisure, tourism rental, transportation, and communication information are growing rapidly.

For example, in terms of exports, exports of new products and new drivers continue to grow rapidly. According to customs statistics, in 2025, China's exports of high-tech products will increase by 8% year-on-year, of which integrated circuit exports will increase by 27.4% year-on-year. China's complete vehicle exports increased by 22% year-on-year.

Regarding the old problems and new challenges faced by current development, the following points are highlighted.

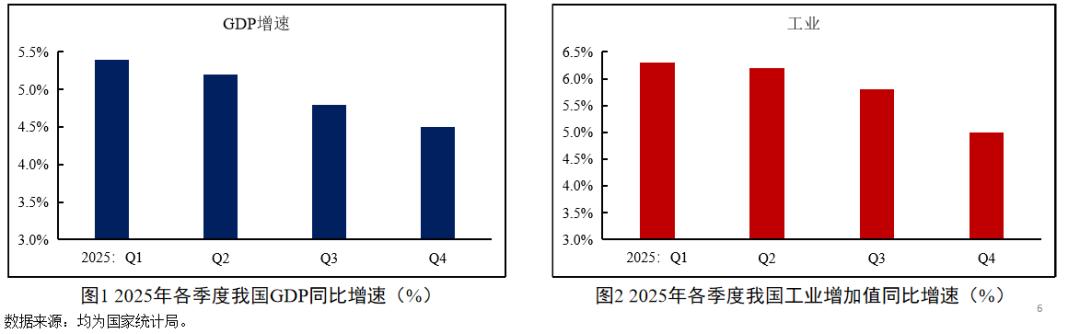

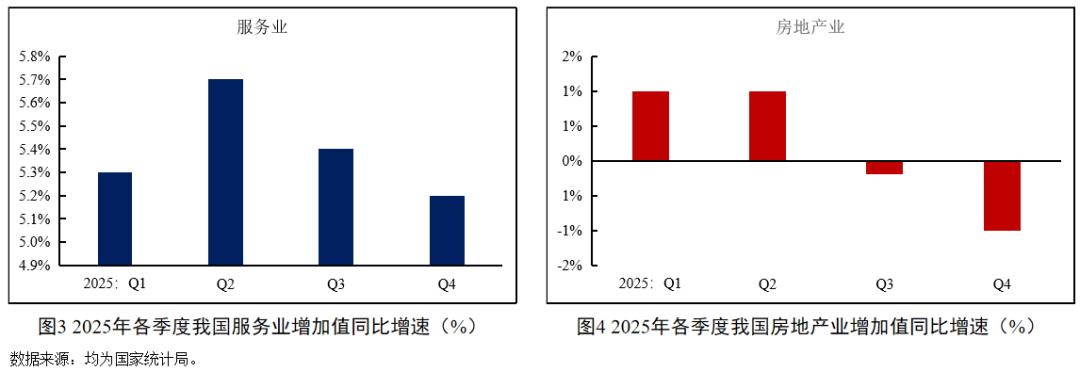

First, economic growth is slowing down quarter by quarter, and downward pressure is still considerable. Judging from the growth of major economic indicators in each quarter of last year, including GDP, industry, service industry, etc., the overall trend was high and then low, and continued to decline. Especially after entering the fourth quarter, the downward trend became more obvious.

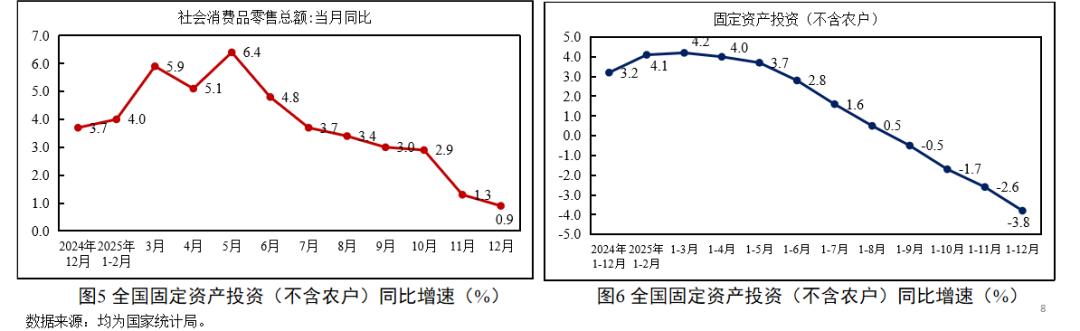

Secondly, the contradiction between strong economic supply and weak demand is still quite prominent, and market prices continue to be depressed. Since the second half of the year, the growth momentum of consumer demand has continued to weaken, with the GDP growth rate in December being only 0.9%, the lowest point in 35 months since the epidemic. Fixed asset investment fell by 3.8% throughout the year, a rare negative growth in more than 30 years since 1989. Among them, real estate investment fell by 17.2%. Prices are the most concentrated expression of supply and demand. On average for the whole year, consumer price CPI was the same as last year, well below the annual expected target of rising by about 2%, while producer price PPI fell by 2.6%.

Third, enterprises still face many difficulties in development, and the problem of unstable expectations is still prominent. Last year, the profits of industrial enterprises above designated size increased by 0.6% year-on-year, and the annual average operating income profit margin was 5.31%, a decrease of 0.03 percentage points from the previous year. In addition, the problem of corporate account arrears is still prominent. As of the end of December last year, the accumulated accounts receivable of industrial enterprises above designated size reached 27.4 trillion yuan, an increase of 4.7% over the same period last year, and the inventory of finished products reached 6.73 trillion yuan, an increase of 3.9% over the same period last year.

In terms of business expectations and confidence, according to data from the National Bureau of Statistics, from April to November last year, China's manufacturing sales managers index PMI was below the 50% boom-bust level for eight consecutive months, setting the longest contraction cycle since 2019. It improved at the end of the year, rising to 50.1% in December, an increase of 0.9 percentage points from the previous month. However, whether this trend can be sustained remains to be further observed.

Fourth, consumer confidence continues to be sluggish, and people are under pressure to increase their employment and income. These pictures respectively show the status of consumer confidence, employment confidence and income confidence in my country. It can be seen that in the short term, consumer confidence has improved to some extent, but in the medium and long term, both the consumer confidence index, the consumer employment confidence index, and the consumer income confidence index are all at historically low levels.

Finally, there are still many hidden risks. In addition to "the deepening impact of changes in the external environment," the central economic work mainly emphasizes real estate risks and local government debt risks, including operating debt risks of local government financing platforms. As we all know, when the Central Economic Work Conference at the end of 2024 deployed risk prevention and control work in 2025, it mainly emphasized the risks of real estate, small and medium-sized financial institutions and illegal financial activities, and did not place special emphasis on local debt risks. This issue has been raised again this year, which shows that real estate and local debt risks have become the two key areas to prevent and resolve risks in the next step.

The above are some of the main situations and basic characteristics of economic operations since last year. Generally speaking, it has both good and problematic aspects. It should be said that both aspects are relatively prominent. In particular, there is still a relatively obvious temperature difference between macro data and the micro-feelings of enterprises and consumers, and the foundation for economic recovery needs to be further consolidated.

2. Several analyzes on this year’s demand environment and development trends

When analyzing and predicting the macroeconomic situation and its trends, the medium and long term mainly focus on the supply side, while the short term mainly focuses on the demand side. This is especially true under the current economic background of our country. This is because, after years of development, our country has formed a strong manufacturing capability. Although this capability also has shortcomings and obstacles, overall, its scale and competitiveness are unparalleled in the world. Under this circumstance, the main contradiction in my country's economic operation, or the main aspect of the contradiction, has gradually shifted from the supply side to the demand side. Only when the demand problem is relatively well solved and the relationship between supply and demand is relatively relaxed can the economic cycle be relatively smooth and the economy as a whole achieve relatively stable and sustainable development. Only when the overall economic growth is relatively stable and sustainable can scientific and technological innovation, green transformation, common prosperity, improvement of people's livelihood, risk resolution, and the solution of other problems such as coping with external challenges have a stronger foundation and more favorable conditions.

An analysis of this year's total demand situation shows that there are many favorable factors as well as many risks and challenges. From a comprehensive judgment, overall, there will be improvement based on this year's basis.

(1) Regarding the external demand environment

Here are the predictions of the global economy and trade in 2026 by the five major international organizations: the IMF, World Bank, OECD, United Nations, and WTO. Taken together, there is a high probability that the global economic growth rate this year will be slightly lower than last year, while the growth rate of global trade, especially trade in goods, is likely to be significantly lower than last year.

Judging from my country's export situation, my country's exports have been able to maintain strong resilience in recent years, mainly due to the rapid growth of new products and new momentum, the continuous deepening of market diversification, and the continuous highlighting of the resilience advantages of the supply chain. These advantages and favorable conditions will continue to appear and work this year. Of course, there is also great uncertainty in the external environment. After two consecutive years of high growth, the base is already relatively high. Coupled with the appreciation of the exchange rate and the increased concerns about trade imbalance in some countries after last year's trade surplus exceeded 1 trillion US dollars. Based on comprehensive judgment, the market generally expects that my country's export growth this year will most likely fall significantly compared with last year, and is expected to be between 3-5%.

(2) Regarding consumer demand

Unsatisfactory growth in consumer demand has been a prominent problem in recent years. As shown in the figure, before the epidemic, the zero growth rate of my country's social economy was generally close to 10%. The epidemic has caused sharp fluctuations in the growth rate of consumer demand, but it has been sluggish since the epidemic. Although the growth rate last year has rebounded compared with the year before, the growth rate has been high and then low, and continues to decline, indicating a lack of stamina and a weak recovery.

This year, there are three main factors conducive to the growth of consumer demand:

First, stimulus policies will continue to be effective. The Central Economic Work Conference not only listed "adhering to domestic demand as the leading factor and building a strong domestic market" as the top priority for economic work this year, but also regarded expanding consumer demand as the top priority for expanding domestic demand. It emphasized the need to implement in-depth special actions to boost consumption, formulate and implement plans to increase the income of urban and rural residents, optimize the implementation of the "two new" policies, clean up unreasonable restrictive measures in the consumption field, and release the potential of service consumption.

The second is the basic stability of residents' employment and the restorative growth of income and confidence. The national average urban survey unemployment rate in 2025 is 5.2%, of which it was 5.1% in December. The growth of per capita disposable income of residents has basically kept pace with economic growth. Since last year, especially in November, the consumer confidence index, employment confidence index and income confidence index have all shown significant restorative improvements.

Third, the continuous expansion of consumption scenarios and fields is conducive to the release of consumer demand. The number of theme markets and immersive experience stores has increased, online and offline integration has become closer, and the product categories covered by instant retail have expanded from fresh food to digital, pharmaceutical, etc., making consumption more convenient. These factors will work together with policies to promote continued expansion of consumption.

The main disadvantage is that the stable growth of consumer demand most fundamentally depends on the enhancement of consumption power and the improvement of consumer confidence. This depends not only on the significant improvement of residents' employment status, significant increase in income and optimization of income structure, but also on the stable improvement of residents' asset status and the continued enhancement of wealth effects. These are subject to the overall improvement of the macro economy, so it is difficult to achieve overnight and requires a process of mutual promotion and gradual accumulation.

Based on comprehensive judgment, market institutions generally expect that consumer demand will rebound further this year on the basis of last year's recovery, and the growth rate will be higher than last year's 3.7%, but it will not be much higher. Market institutions predict that most of them are between 4% and 5%.

(3) Regarding investment needs

As mentioned above, fixed asset investment last year experienced a rare negative growth that had not been seen in many years, becoming the biggest shortcoming in expanding domestic demand.

This year, there are two main factors conducive to investment growth:

First, this year is the first year of the "15th Five-Year Plan". Many major projects in the "15th Five-Year Plan", including major science and technology power projects, major infrastructure projects, major green transformation projects, major livelihood projects and major regional coordinated development projects, will be concentrated in this year in accordance with the central government's requirements of "early planning and early start", forming a physical workload and playing an important supporting role in the recovery of investment.

Second, from a macro policy perspective, promoting effective investment is still a focus this year, and the policy environment is relatively favorable. The Central Economic Work Conference clearly stated that in 2026, it is necessary to "promote investment to stop falling and stabilize". To this end, it is necessary to appropriately increase the scale of investment within the central budget, optimize the implementation of "double" projects, optimize the management of local government special bonds, continue to play the role of new policy financial instruments, effectively stimulate the vitality of private investment, and at the same time, promote urban renewal with high quality. Officials from the Ministry of Finance have also repeatedly stated that the central government's overall fiscal support this year will "only increase but not decrease", and the protection of key areas will "only be strong but not weak". In 2026, ultra-long-term special treasury bonds will continue to be used for "double" and "two new" tasks. In this context, macroeconomic policy support will only become stronger, not weaker.

Looking at the three major investment areas of manufacturing, infrastructure and real estate, manufacturing investment increased by 0.6% last year, the lowest point in many years. This year, the vigorous development of new technologies, new industries, and new driving forces will undoubtedly be conducive to the growth of manufacturing investment. However, for traditional manufacturing industries with large volumes and wide areas, the key still depends on market demand, corporate profitability, and entrepreneurs' confidence in development prospects. Taking into account various factors such as policy support and changes in market demand, market institutions generally predict that the growth rate of manufacturing investment this year will improve compared with last year, reaching 3% to 5%. Infrastructure investment fell by 2.2% last year, the first time in more than 30 years. Infrastructure investment may benefit the most from the favorable macro policy environment in the above two points. Market institutions generally predict that the growth rate of infrastructure investment this year may increase significantly compared with last year, reaching about 4% to 5%, becoming the most important force supporting the stabilization of investment this year. In terms of real estate investment, it fell by 17.2% last year, the largest decline in many years. The Central Economic Work Conference continued to emphasize that this year we must "focus on stabilizing the real estate market, implement city-specific policies to control increment, destock, optimize supply, and encourage the acquisition of existing commercial housing to focus on affordable housing." We must "promote the construction of "good houses" in an orderly manner, and accelerate the construction of a new model of real estate development." In addition to increased policy support and a more positive policy environment, urban renewal has been further intensified and the confidence of home buyers in some cities has improved, which is also conducive to the restorative growth of real estate investment. Taking into account various factors, market institutions generally predict that although it is still difficult for real estate investment to get rid of the negative growth pattern this year, compared with last year, the negative growth rate is expected to narrow significantly.

Based on comprehensive judgment, there is a high probability that investment growth this year will be better than last year, and it is expected to stabilize and achieve positive growth of 2% to 3%.

The above are some basic conditions and analysis and predictions of market institutions about this year's total demand trend. The market situation changes rapidly, and there are many unstable and unpredictable factors, especially the international environment, so the situations introduced are for reference only.

3. Combining long-term and short-term measures to treat both symptoms and root causes to continuously and effectively release the potential of domestic demand

As mentioned just now, at this stage, whether it is to boost confidence and stabilize growth in the short term, or to promote sustained and high-quality economic development in the medium and long term, expanding domestic demand plays a very critical and even decisive role. In fact, everyone has seen that expanding domestic demand has always been a focus of the party and the government's economic work in recent years. Especially in the past two years, the scope and intensity of policies to expand domestic demand are unprecedented. Judging from the actual operating conditions of the economy, various policy measures to expand domestic demand have also achieved positive results and played an important role in ensuring the realization of expected development goals. Despite this, the problems of insufficient market demand, strong supply and weak demand, and weak prices are still prominent. So what exactly is the problem? How should the policy of expanding domestic demand be further focused?

Due to time constraints, it is impossible for me to go into detail. Here I will briefly talk about the basic understanding and suggestions from the two aspects of consumption and investment.

(1) To continuously and effectively release the potential of consumer demand, more emphasis must be placed on structural countermeasures

In recent years, everyone has become more and more aware that the reasons for my country's current insufficient consumer demand include, in addition to the impact of short-term market volatility factors, medium- and long-term phased and deep structural constraints. The so-called staged reasons mainly refer to the fact that due to the improvement of my country's development level and changes in population structure, my country's residents' overall consumption has shifted from mainly commodity consumption to both commodity consumption and service consumption. The so-called structural reasons are mainly due to the long-term low consumption rate of Chinese residents. According to the analysis of different scholars, the degree of low is roughly 10% to 20%. Short-term factors and medium- and long-term factors are not only superimposed and intertwined in time and space, but also interact and reinforce each other, forming a negative cycle of shrinking demand, increasing employment pressure, slowing income growth, weakening wealth benefits, and further declining consumption capacity and consumer confidence. Therefore, the response must be to use short-term and powerful stimulus policies to interrupt the negative cycle, while at the same time focusing on solving the underlying problems and continuously laying a solid foundation for sustained and stable growth.

On the one hand, the counter-cyclical consumption stimulus policy must continue to optimize the scope and structure of support for commodity consumption without reducing the total amount and continuing to exert force, and support service consumption with greater intensity. In particular, in accordance with the requirements of investing in people, it must target urgent and difficult issues such as education, medical care, pensions, and childbirth that the masses are anxious about, and increase subsidies to boost consumption willingness and enhance consumption ability. On the other hand, we must effectively implement the residents' income growth plan, and make greater efforts to improve the level of social security and public services for low-income groups, effectively enhancing the safety expectations and consumer confidence of our residents.

(2) The space for investment demand is still not small, and it also needs to be supported through institutional and policy innovation.

At the current stage, although consumer demand needs to play a greater role in driving economic growth and the proportion of consumer demand in total demand needs to be significantly increased, this does not mean that investment is unimportant, nor does it mean that efforts to expand effective investment can be relaxed. Fully unleashing consumption potential and focusing on expanding effective investment should be paid equal attention to achieve positive interaction.

There are two key focuses to further release and expand the potential of investment demand. One is to accelerate the formation of a new model of urban and rural construction and real estate development that is suitable for the new stage, and the other is to vigorously boost private investment and foreign investment.

With the changes in development stages, although the past era of large-scale or even extensive urban and rural construction and real estate investment expansion characterized by solving housing shortages has ended, investment and consumer demand focused on improving the urban and rural environment and housing quality are still huge. Taking cities as an example, it includes urban renewal and environmental optimization, as well as residents’ demand for higher-quality housing. The problem is that although the investment needs in these areas are not small, they are difficult to achieve through the simple real estate development model of the past, let alone the incentive mechanism of land finance. To fully unleash these investment potentials, it is necessary to accelerate the exploration and formation of new models of urban and rural construction and real estate development that are suitable for the new stage. The key is to coordinate and balance the interests of all relevant parties, clarify the responsibilities and rights of different subjects, and give full play to the role and enthusiasm of the government, enterprises, owners, society and other parties.

To further promote private investment and foreign investment, in addition to continuing to respond through policies to expand domestic demand, it is also very important to further improve the business environment and stabilize and enhance business expectations and confidence by deepening reforms and expanding opening up.

Finally, it needs to be pointed out that the Party Central Committee has repeatedly emphasized that our country’s economic foundation is stable, has many advantages, is strong in resilience, and has great potential. The supporting conditions and basic trends for long-term improvement have not changed. Indeed, from a global perspective, the advantages or favorable conditions for my country's development are not only huge, but also unique and even unique. As long as we follow the requirements of the Central Economic Work Conference, adhere to both policy support and reform and innovation, combine long-term and short-term measures, and address both the symptoms and root causes, we will surely be able to promote further economic recovery and lay a solid foundation for medium- and long-term high-quality development.