This year, the U.S. stock market indexes have repeatedly hit new highs. The market capitalization-weighted indexes Nasdaq Index (IXIC.US) and S&P 500 Index (SPX.US) have cumulative gains of 11.11% and 9.84% respectively, reaching 21,455.55 points and 6,460.26 points, mainly due to the strong trend of the "Seven Sisters" Driven by the trend, Google (GOOG.US), Microsoft (MSFT.US), Meta (META.US), and NVIDIA (NVDA.US) all hit new highs in the second half of this year. Among them, NVIDIA has repeatedly set the highest market value in the history of global listed companies, but this does not hinder the pace of repurchases by giants. Is their aggressive repurchase activity a vote of confidence in themselves, or is it a helpless move due to lack of confidence in potential investments in the market?

NVIDIA buyback

As rational economic people, technology giants like Nvidia, which has the most professional financial analysis team, control every penny of the company very scientifically and accurately, which means that every penny of its use can bring it the greatest economic value.

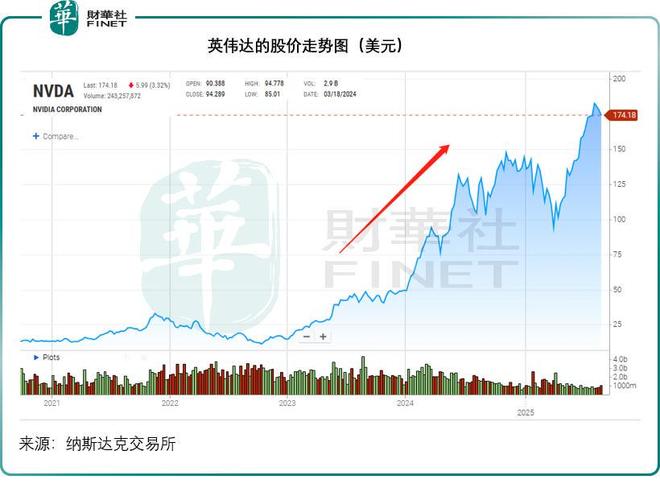

See the figure below. The AI wave will begin to break out at the end of 2022, and Nvidia's stock price will also start to soar at the end of 2022. According to our estimates, from the beginning of 2023 to the present, Nvidia's stock price has increased by a cumulative 10.93 times.

According to our estimates, NVIDIA's non-accounting net profit for the 12 months ending July 27, 2025 was US$87.753 billion, which is 6.94 times higher than the company's non-accounting net profit of US$11.058 billion for the 12 months ending July 31, 2022 before the AI boom.

Its current stock price trend far outperforms its profit growth. However, Nvidia still chooses to increase repurchases and increase dividends at this time. Nvidia paid a dividend of US$488 million in the first half of fiscal year 2026, a year-on-year increase of 41.86%.

As of the end of July 2025 this year, the company has returned US$24.3 billion to shareholders through repurchases and dividends. By the end of July, the company still has a repurchase authorization of US$14.7 billion, plus an additional US$60 billion of unlimited repurchase quota, which means that there is still US$74.7 billion of repurchase authorization that can be fulfilled.

Making buyback commitments and increasing dividends may, on the one hand, reflect Nvidia's confidence in its future prospects – buying its own shares at current prices is much more cost-effective than investing in other projects on the market, and it may also mean that the company's expected future earnings growth has not yet been reflected in its current stock price.

But on the other hand, it may also be to appease shareholders. Nvidia's management also mentioned at the July quarterly results meeting that the company will seize investment opportunities in AI solutions and sovereign AI in the future, which means it will increase investment. At the same time, it faces the possibility of missing out on China's major AI market and its current valuation is overvalued. The company may increase returns to shareholders to ease shareholders' concerns about returns on capital investment.

Capital spending ramps up with buybacks

While the "Seven Sisters" are increasing capital expenditures to consolidate their AI development advantages, they are also increasing repurchase amounts and increasing dividends to please shareholders.

Cash-neutral Apple (AAPL.US) has been a big spender on repurchases, with Wind data showing its repurchases amounted to $46 billion this year. However, Cook said at the June financial quarter results conference that Apple will invest US$500 billion in the United States over the next four years to promote innovation and create jobs in cutting-edge fields such as advanced processes, chip engineering, and AI. It is unknown whether this will affect its future repurchase capabilities.

Meta and Google are also the main players in repurchases. Although the stock prices of both companies have hit new highs this year and they have continued to significantly increase capital investment in the construction of data centers, they have not been stingy with repurchases.

Meta repurchased 36 million Class A ordinary shares for US$23.16 billion in the first half of this year. By the end of June 2025, the company still has a repurchase limit of US$28.23 billion. At the same time, Meta will increase its cash dividend by 5% from the first quarter of 2025. However, it should be noted that Meta's increase in capital expenditures is far greater than its return to shareholders. In 2024, its capital expenditure will be US$39.2 billion, and it recently raised its capital expenditure budget for 2025 from US$64-72 billion to US$66-72 billion, which means an increase of at least 68%. Management expects capital expenditures in 2026 to be similar to this year. It is not difficult to understand that Meta needs to give shareholders some small favors through buybacks and increased dividends to rationalize its expansion of AI capital investment.

In the first half of 2025, Google repurchased 164 million shares at a price of US$28.564 billion. In April this year, its board of directors increased its repurchase quota by another US$70 billion. As of the end of June 2025, Google still had a repurchase quota of US$86.3 billion. Similarly, Google, like Meta, increased its quarterly cash dividend by 5% in April this year. However, it should be noted that Google has further increased its capital expenditure, raising its capital expenditure guidance for 2025 from US$75 billion to US$85 billion, and stated that capital expenditure in 2026 will further increase.

The situation is similar at Microsoft.

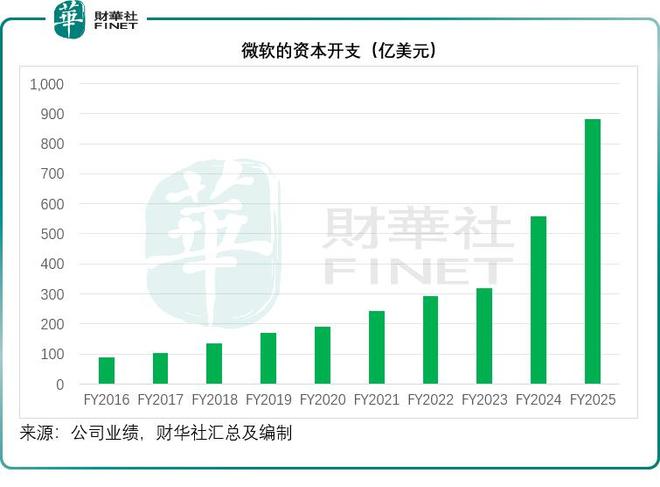

In fiscal year 2025, which ends in June 2025, Microsoft has repurchased 31 million shares for US$13 billion, and currently has an approved repurchase quota of US$57.3 billion. At the same time, Microsoft is also one of the companies with the highest capital expenditure budget among the "Seven Sisters", although it stated that its fiscal year 2026 resources will This expenditure will increase moderately year-on-year, but we checked the company's previous records and found that Microsoft's capital expenditures have increased exponentially in the past two years. Capital expenditures in fiscal year 2024 and fiscal year 2025 increased by 74.61% and 58.35% year-on-year, respectively, to US$55.7 billion and US$88.2 billion.

Conclusion

Therefore, technology giants represented by Nvidia are currently significantly increasing stock repurchases and cash dividends. Their deep strategic purpose is not simply shareholder returns, but to pave the way for larger-scale capital expenditures to consolidate and expand their lead in the fierce AI competition.

Through buybacks and dividends, these companies aim to:

Please and appease shareholders: When investing huge amounts of money in long-term, high-risk AI infrastructure (such as data centers, chip research and development), balance shareholders' concerns about profit dilution and long investment cycles through stable cash returns, maintaining market confidence and stock price stability.

Optimize the capital structure and support strategic investment: demonstrate its excellent cash flow management capabilities and prove to the market that the company has the strength to simultaneously "invest in the future" and "return in the present". The ample repurchase quota is more like a financial strategic reserve, ensuring that while fully betting on AI, it can still flexibly use financial tools to manage market value and offset the dilution effect.

In essence, generous repurchases are an extension of its rational economic man’s thinking: it is a necessary measure to exchange short-term profit distribution for shareholders’ long-term strategic support. The ultimate goal is to allocate capital more efficiently and without resistance in areas that can generate the greatest future value—that is, to win the dominance of AI development.